If I have one critique about the financial independence community, it’s that certain segments can be awfully judgy.

This is especially true when it comes to how people choose to spend their money.

If you choose to spend money on a big house, a fast car, or heaven forbid… a latte… watch out for the Financial Independence Police.

They will tell you you’re doing it all wrong, and you’ll never reach financial freedom spending like that.

I disagree.

More to the point, I don’t find judgments like that productive, especially when I teach personal finance to lawyers.

Instead, I do my best to encourage my students to spend their money based on their own values, not anyone else’s. Yes, there always tradeoffs. But, those tradeoffs are yours alone to make.

In today’s post, I wanted to explore this concept as it relates to my own spending decisions.

Spoiler alert! The FI Police won’t like how much I spend on housing.

Let’s dive in, starting with how the average American spends his money.

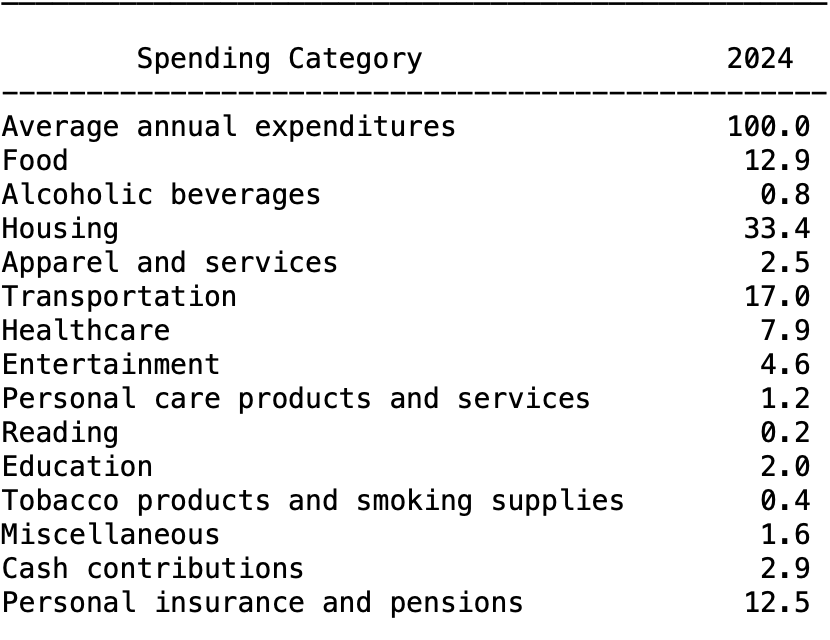

The average American spends the most in three categories: housing, transportation and food.

According to the U.S. Bureau of Labor Statistics, Americans tend to spend the most money each month on housing (33.4%), transportation (17%), and food (12.9%).

Those three categories equate to nearly 63% of the typical American’s budget. This is not to say that you should base your spending on these averages. Everyone is different.

But, conventional wisdom goes that by focusing on just those three categories, most people can make major strides towards financial independence.

Scott Trench from BiggerPockets Money has been championing this idea for years. Check out his book Set for Life to read more about the impact you can make on your finances by targeting just these three areas.

Personally, I spend way more on housing than the typical American.

Look out! Here comes the FI Police!

Before they lock me up and throw away the key, hear me out. There are some intentional reasons why my wife and I spend more on our house, some financial and some emotional.

And, I’ve never been closer to financial independence.

More on that below.

First, let’s remind ourselves about that intersection between money and emotions and why it’s so important to make individual decisions when it comes to our money.

There are no hard and fast rules on how you should spend your money.

In The Art of Spending Money, bestselling author Morgan Housel explores the relationship between spending money and happiness.

Housel’s primary thesis is that there are no hard and fast rules on how you should spend your money. What you may value is different from what I may value.

For that reason, we should all make individual spending choices based on what matters the most to us. To go along with that, we should not spend money to impress other people. When we do that, we will never find happiness.

In Housel’s estimation, seeking external validation based on material possessions is a one-way ticket to a miserable life.

It’s hard to disagree with that.

Here’s a passage about spending habits that resonated with me:

The people I know who’ve used money best have inconsistent spending habits. They spend a lot of money on this, and very little on that. They value this, and couldn’t care less about that. They’re independent thinkers, forcing their money to work for them, not the other way around.

This was such a brilliant observation that it inspired me to write about how I spend my money. That’s the focus of today’s post.

What you can learn from other people’s spending habits.

As you read about my spending habits, remember Housel’s advice:

We all value different things and experiences. That means we naturally should be spending money on different things and experiences.

Of course, you may appreciate some of my spending decisions. On the flip side, you may think other spending decisions are foolish.

That’s OK. No FI Police to worry about here.

The point is not for me to tell you, “Spend money like me if you want to be wealthy.”

The idea is that by hearing my perspective, you might be inspired to evaluate your own spending habits and think about whether you want to make any adjustments.

And, that right there is the whole key to budgeting.

Why a Budget After Thinking works for young lawyers when other budgeting systems fail.

It’s not for me or anyone else to tell you what to do with your money. Housel knows a thing or two about money and just wrote an entire book premised upon that message.

That’s why I don’t tell you to save 20% of your income or only spend 50% on fixed expenses.

In my experience teaching personal finance, that advice just doesn’t work for young lawyers with entry-level salaries and massive student loan debt.

The truth is fixed spending rules sound good until you actually try to implement them.

In reality, when you base your entire budgeting strategy on arbitrary rules like “save 20%,” you’re likely to realize that target is out of reach.

You would have to cut so much from other areas that your budget would be oppressively restrictive. The result is you’ll get frustrated and quit your budget.

I have a different approach. One that actually works for young lawyers.

With a Budget After Thinking, the central purpose is to evaluate your current spending habits, no matter your starting point. Once you understand where your money is going, you can implement thoughtful adjustments that match your lifestyle and financial goals.

No hard and fast rules.

Just individual thought and discretion.

And, that leads us to my self-evaluation on how I spend money.

Note: for budgeting purposes, I do not include bonuses in my income. Any bonus money I earn goes straight to investments. Call it the “Jay Leno Rule.” More on that in a future post.

Housing takes up about 40% of my budget.

Similar to most Americans, housing is my biggest monthly expense.

Where I’m different is that I spend more of my monthly budget on housing than most.

The funny thing is my answer would have been the exact opposite if I wrote this post in 2024.

From 2018-2024, I had zero housing costs. We lived in apartments within buildings that we owned. The rent we collected covered all of our housing expenses. That allowed us to save a lot of money, most of which we invested in more rental properties.

In 2024, we moved into our “forever home” just outside Chicago. For the first time in our married life, we had housing expenses to pay on our own.

Housing now takes up about 40% of my monthly budget.

Here are some reasons why we choose to spend more on housing.

My wife and I are comfortable spending a decent amount on housing at this stage of our lives. We made that decision intentionally and haven’t regretted it for a second.

Here are some of the financial reasons why we choose to spend more on housing:

- We lived in small apartments for free until I was almost 40-years-old. If you average out our housing costs including that time period, we’re well below the American average.

- We have already reached Coast FIRE. That means we’ve already saved enough for a comfortable retirement, opening up more money to spend today. To see if you’re in the same boat, you can use the TATM Coast FIRE calculator.

- Additionally, we have enough saved to cover college for 2 of our 3 kids. Again, more money to spend elsewhere. You can see if you’re on track with the TATM 529 College Savings Calculator.

- Finally, refer back to the Jay Leno Rule mentioned above. We don’t spend our bonuses, just our regular paycheck. If we included bonuses, that 40% figure would drop significantly.

In terms of emotional reasons, here’s why we choose to spend more on housing:

- Our family is growing. We now have three young kids. The neighborhood is full of families, and the schools are great. This is the exact time in life to prioritize a home for my family.

- We can walk to parks, shops, and restaurants. It’s also an easy commute downtown for me.

- We simply like spending time at home. Call me a homebody. As a family of five, we spend a lot of time amusing ourselves at home.

- On top of that, just about every weekend, we host friends or family at our house, something we prefer to going out.

The point is: we spend more than average on our home, but it’s more than worth it to us.

The tradeoff is that because housing eats up a big chunk of our budget, we intentionally don’t spend as much in other areas. That ensures we stay on track to financial independence.

Let’s explore that further.

Transportation takes up only 3% of my monthly budget.

Spending decisions always have ripple effects. In my case, that plays out when you look at my housing expenses in relation to other areas, like transportation expenses.

Here’s what I mean:

We spend a decent amount on our house, but because of the house we chose, we don’t spent a lot on transportation.

I walk to the train station for my commute downtown. We walk our kids to school. For date night, my wife and I walk into town for dinner.

Most of our weekly driving is to the grocery store (2 miles away) or to kids’ activities (all close by). On the weekends, we tend to visit grandparents (25 miles away or less), which also means free entertainment.

In total, we just don’t drive very much. When we do drive, we don’t go very far.

All told, we spend about 3% of our monthly budget on transportation.

That includes car insurance, gas, maintenance, and train passes.

We do not have a car payment. One of our cars is now 10-years-old and the other we bought two years ago. We don’t plan on replacing either vehicle anytime soon.

Food eats up about 7% of my monthly budget.

Do you see what I did there?

As a family of five, our grocery bills keep getting bigger. Kids gotta eat, right?

Most of our food budget is used at the grocery store. We shop at Costco, Mariano’s and Trader Joes.

We eat most of our meals at home. I bring my lunch to work every day. Same for coffee.

So, most of our food budget is for groceries rather than dining out.

As for dining out, this just isn’t a big part of our lives or budget. I owe a lot of that to having young kids who sort of take all the fun out of restaurants, but also that we like eating at home (see above).

When we do dine out, we tend to keep it casual. We do pizza night weekly at a neighborhood Italian restaurant. Maybe carryout a couple times per month.

My wife and I are hoping to incorporate more date nights this year. Not always the easiest thing with three kids under six at home.

If you add up date nights and socializing with friends, we dine out maybe 2-3 times per month.

Add it all up and food eats up about 7% of our monthly budget.

In total, 50% of my monthly budget goes to housing, transportation, and food.

In total, we spend 50% of our budget on housing, transportation, and food. That’s less than the typical American (63%).

However, compared to the typical American (33%), we spend more on housing (40%). We make up for it by spending less on transportation and food.

What would the FI Police have to say about that?

In my opinion, there’s no right way or wrong way to do it. We try to be intentional about each choice we make, understanding the ripple effects on the rest of our budget.

The end result is that by keeping our spending in check in these three major categories, even with spending more on housing, we have more funds available for fun and for financial goals.

What else do I spend money on?

The remaining 50% of our budget goes mainly towards discretionary spending and financial goals.

I’ve previously outlined my current financial goals. Click here to read more.

Today, I’ll give an overview of how I spend the rest of my money.

I am a “Buy Once, Cry Once” consumer.

I am definitely a “Buy Once, Cry Once” person. That means I’m happy paying more upfront for a quality item that will last to avoid the repeated costs and frustration of replacing cheaper items.

That applies to clothing, furniture, recreational items, gadgets, and everything else. For example, I’d rather spend more on a single nice sport coat that will last me decades instead of three cheaper ones that will need to be replaced.

As another example, we’ve been in our house for less than two years and are taking our time getting furniture to fill it up. I’d rather buy one new dresser that will last until the kids are off to college instead of three new dressers that I’ll need to replace.

The tradeoff is that certain rooms look emptier for longer. I laughed when we hosted a party and some guests made fun of the smallish TV we have in the family room.

My wife and I are fine with that. We don’t like clutter. We don’t like shopping. This spending philosophy matches our personalities perfectly.

We spend money on travel and the kids.

As a family, we like to take trips to our two favorite places, Colorado and Florida. While traveling with a family of five can be expensive, we use points to keep our costs as low as possible.

To that end, we primarily use the Chase Sapphire Reserve to earn points and pay for travel.

Besides traveling, we spend a good amount on kids’ activities: ski lessons, piano lessons, swimming lessons, soccer, dance, Girl Scouts… and that’s just what comes to mind for my oldest daughter.

Yikes.

As a side note, if you ever needed a reason to learn strong personal finance fundamentals when you’re young, re-read that previous sentence. It’s important to take ownership of your money decisions right now. It only gets more complicated as you progress through life.

I don’t mind spending on the kids so they can try new experiences. It’s fun to watch them have fun, socialize and learn new skills.

My love language is gift giving.

Have you ever looked up your “love language?”

I think mine is gift giving. I like buying gifts for my wife and kids, more than I like getting things for myself.

That means plenty of opportunities to spend money with four birthdays and seemingly unlimited holidays throughout the year.

I particularly enjoy when I think of a gift idea months ahead of time and visualize the moment when I give it to the person.

These gifts don’t have to cost a lot of money, by the way. Ask my father-in-law about the garbage bags I gifted him. I planned that one for months. I think I enjoyed it more than he did…

We spend intentionally on everything else without tracking every penny.

Besides these expenses, we spend intentionally on things and experiences as they present themselves throughout the year.

To stay on budget, we track just two simple numbers using the TATM Budget After Thinking Template™️.

We’ve learned enough about our spending habits that we no longer need to track every penny. When we want to buy something, we buy it and focus on just those two simple numbers.

For example, I got really into planting trees in the backyard last spring.

Trees can be expensive, but I enjoyed putting them in the ground and watching them grow throughout the season. Plus, when I would buy a couple trees, I’d make sure to hold off on other big purchases that month.

As another example, the kids are really into Halloween and Christmas decorations for the house. Each year, I tell my kids they can pick out one new decoration. This year, it was a giant skeleton. It brought them so much joy.

Holiday decorations like that are another seasonal expenditure that we’re happy to take on with a little advanced planning.

So, how do you spend your money?

This was a fun and valuable post to write.

It forced me to self-evaluate my spending decisions, and I’m generally happy with where I’m at.

That hasn’t always been the case.

When I started on my financial independence journey, my spending was a mess. It took some time and discipline to get on the right track.

What I learned is that once you make those thoughtful adjustments, the results can be life changing.

I encourage you to take a look at your owning spending habits.

If you’ve never thought about budgeting before, you can learn all about my Budget After Thinking philosophy here. You’ll find a custom-built budgeting template and links to a number of posts to help you get started.

When you evaluate your habits, you may be in a similar boat as me or a completely different boat.

Either way, let me know in the comments below or reach out if you have any questions.

That’s what makes thinking and talking money fun.

Leave a Reply