Being good with money starts with the little stuff.

What I’ve learned teaching personal finance is that too many of us want to race right to the finish line. We want to skip ahead to mile 26 without completing the rest of the marathon.

Money doesn’t work that way. There’s no magic switch to skip over the hard part. The little stuff matters.

Picture the young lawyer who graduates with $100,000 in student loan debt. Absent some unlikely windfall, it’s going to take years of consistent payments to eliminate that debt.

No matter how badly the young lawyer wants that debt to go away, he’s going to carry it for a while. There’s simply no fast way to eliminate hundreds of thousands of dollars of debt.

But, there are faster ways.

I’ll show you exactly what I mean below using the Think and Talk Money Student Loan Calculator.

What you’ll notice is that every $20… $30… $50… decision can make a big impact on your overall financial picture.

This isn’t to say that you shouldn’t spend your money on stuff that makes you happy today. What it means is that you should spend that money knowing how meaningful it could be down the road if used for your financial goals.

Of course, this is easier said than done. When you’re staring down six-figures of debt, focusing on the little stuff may not seem that exciting. But, if you can make these types of small adjustments now, you can buy back years of your life.

Focusing on the little stuff is how you get ahead.

This discussion is not just for lawyers paying off student loans. The same idea applies if you’re trying to pay off credit card debt, save up to buy a home, or invest for your kid’s college.

There are no fast ways to accomplish these goals.

But, there are faster ways.

In my opinion, too many of us don’t want to do the little stuff that will accelerate our financial journeys. We don’t take advantage of these faster ways.

Instead of making intentional money decisions on a consistent basis, we spend mindlessly and hope to get bailed out with a huge bonus later on.

That’s too risky. What if that bonus never comes? You’ve formed bad habits and set yourself up for trouble.

If this sounds like you, you’re not alone. Too many Americans behave this way when it comes to spending instead of saving.

Would it surprise anyone to learn that most Americans are not satisfied with the amount they have saved?

According to a recent survey from Yahoo Finance/Marist Poll:

- Only 10% of households are completely satisfied with the amount of money they have saved.

- Only 20% reported saving more in 2024 than in 2023.

To me, these numbers prove that we aren’t doing the little stuff when it comes to our money.

Unfortunately, these results aren’t surprising at all. They closely mirror the stats I first showed my students in my financial wellness class back in 2021.

What happens when we don’t do the little stuff?

Let’s look at another stat that illustrates what happens when we don’t do the little stuff:

- About 33% of households would not be able to pay their bills or expenses for one month, if faced with a sudden loss of income.

- This number rises to 38% of Gen Z and 41% of Millennials who report they could not pay their bills for even a month.

What do these numbers really mean?

1 in 3 people currently reading this post, in the comfort of their homes they have worked so hard for, would not be able to afford those homes for even one month if they suddenly lost their jobs. It’s worse for Gen Z and Millennials.

Put another way, maybe you’re on the train commuting to work while reading this. How many people are in the train car with you? 30 or so?

Pick out 10 passengers, really look at their faces.

They’re just like you, typically responsible people, working a job to provide for themselves and their families. If these 10 people suddenly lost their jobs, they wouldn’t be able to pay their bills next month.

That’s scary.

Count me in the group of people not completely satisfied with their savings.

If you read these stats and are honestly not worried about your savings, you are in the minority and are doing a tremendous job managing your personal finances.

Keep up the good work and please let us know in the comments below what strategies are working for you.

On the other hand, if you’re being honest with yourself, you’re most likely in the 90% of people that are not completely satisfied with their savings.

Count me in this group.

From 2017 to 2024, my wife and I prioritized using all of our available money to acquire real estate. The downside was that left us limited funds for savings.

We now have work to do to build our savings back up. Instead of presently shopping for investment properties, we are now focused on paying down mortgage debt and increasing our savings.

Most people attribute their low savings to rising cost of living.

What is the most common explanation given by people that have so little saved? The rising cost of living across the nation:

- Nearly 66% of Americans believe that the cost of living for the average family is not affordable in their area.

Millennials and Gen X are the most worried about the cost of living, with more than 70% of each group feeling unprepared. 64% of Gen Z and 59% of Baby Boomers likewise feel unprepared.

Cost of living includes necessary expenses like housing, food, transportation, and healthcare. In other words, Now Money.

There are any number of reasons we can point to that are combining to drive up the cost of living, like limited housing inventory, higher interest rates, and more expensive groceries.

Our goal should be to focus on what we can control. That means the little stuff.

Let’s explore one way to pay more attention to the little stuff.

So, what exactly can we do to focus on the little stuff?

When it comes to establishing good money habits, don’t overcomplicate it. There’s nothing wrong with starting small.

A good place to start is with how much money you’re spending on food, whether that means restaurants or groceries.

Why start with food?

There are endless options when it comes to spending money on food. We can choose to spend a lot, or a little, or somewhere in between.

Curious how much the average American spends on dining out?

According to a recent survey from CNET:

The average adult spends $59.19 per week, which adds up to $236.76 per month and a whopping $2,832 a year. Some age groups spend even more.

Of all generations surveyed, millennials (born roughly between 1981 and 1996) spend the most on restaurants and takeout. The average millennial spends $86.55 per week on takeout, which comes out to $346.20 per month and $4,154.40 a year.

Dining out is not the only area to target when it comes to how much you spend on food. CNET also found that we waste a lot of groceries that we end up throwing out:

The average US adult wastes a significant amount of money on food from the grocery store that never gets used. An average of $31.25 weekly is spent on groceries that aren’t cooked or eaten, amounting to $125 per month and $1,500 a year.

For today’s example, let’s focus on this one area of consumption to see how the little stuff can make a big impact on our finances.

How the little stuff can take years off your loan payments.

Let’s focus just on that $125 per month on wasted food from the grocery store. It may not seem like a lot of money to waste, but it adds up.

Let’s revisit our recent law school graduate with $100,000 in student loan debt. Let’s assume he has a 7.5% interest rate and currently pays $1,200 per month.

Using the Think and Talk Money Student Loan Calculator, we can see that with no additional payments, it will take him 9 years and 11 months (119 months) to pay off his loans. He will pay a total of $141,696.

Now, what if he can make an additional payment of $125 per month just by paying more attention to what he’s buying at the grocery store?

With an extra monthly payment of $125, he could eliminate his loans 16 months faster and save $5,999 in total payments.

Think about that.

That’s more than a year of his life back without having to worry about loan payments. All he had to do was pay attention to the little stuff at the grocery store.

What if you make a series of little decisions like this with your money?

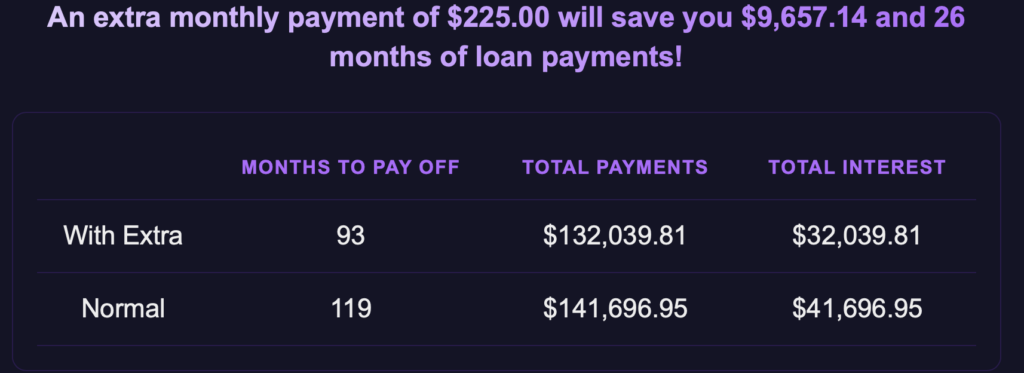

Let’s take it one step further. Let’s say our recent law grad also decides to spend $100 less on dining out each month. That’s only $25 per week, which is about what one lunch and one coffee cost these days.

By adding that $100 per month on top of the $125 he saved at the grocery store, he can shave off more than two years of loan payments and save $9,657.

This example illustrates how consistently paying attention to the little stuff can pay massive dividends down the road.

In this case, small adjustments with food can lead to thousands in savings and accelerate your journey to financial freedom.

Pay attention to the little stuff to accomplish your financial goals.

The big takeaway here is that achieving your financial goals starts with the little stuff. There’s no secret weapon or magic wand. You can’t finish mile 26 without completing miles 1-25.

Just like with our recent law grad with six-figure debt, start small and reap the benefits down the road.

Like we said earlier: there’s no fast way to achieve your money goals. But, there are faster ways.

Paying attention to the little stuff may not be exciting, but it works.

If you know a better way, I’d love to hear about it in the comments below.

Leave a Reply