I try to bring my lunch most days. It’s partly trying to eat healthier. The other part is that I have a hard time justifying the cost and have decided that lunch is really not something I care about.

Even so, there are days when I run out of time in the morning to get a lunch packed before I’m out the door. On those days, I’m usually looking for something relatively quick and healthy.

I’ve noticed that no matter where I go near my office, it seems like the cost of a fast-casual lunch is between $15-$20. That’s true whether it’s a sandwich or a salad or a burrito.

$20 for a lunch that is not even the least bit exciting! That’s hard for me to swallow (sorry, couldn’t help myself…)

Am I yelling at the clouds alone here?

Why does it matter that everything is getting more expensive?

There’s no single explanation for why things are getting more expensive. For example, restaurants are facing higher costs for ingredients, labor, and even online reservation sites.

Setting aside isolated explanations, the reality is that all things tend to get more expensive over time.

The word for that reality is “inflation.”

Specifically, inflation is defined as “ongoing increases in the overall level of prices.”

If you were accustomed to paying $10 for lunch, and now that same lunch costs $20, that’s what inflation looks like.

Terry took no risk and kept his money in a savings account. Terry did not play offense.

Sally took on reasonable risk and invested in the S&P 500. Sally played offense.

What happened after 40 years in our hypothetical scenario?

Terry, at a 3% interest rate from his savings account, had a total of $234,358.87.

Sally, at 10% annual returns from the S&P 500, had a total of $1,440,925.81.

As a result, Sally will have $1,200,000 more than Terry to do fun things with in retirement.

Sally clearly played offense. Terry clearly did not.

Investing to counteract inflation is playing defense.

You may be thinking that at least Terry’s “safe” approach meant that he played good defense.

Nope.

Terry’s approach was bad defense just like it was bad offense.

All because of inflation.

Investing to counteract inflation is playing defense. It’s protecting your hard-earned purchasing power.

Over the long term, it’s critical to invest your money and earn a return that exceeds the rate of inflation.

Otherwise, you risk not being able to afford the same items you’re accustomed to buying today because those items will be more expensive.

In our earlier examples of eggs and workday lunches, we’ve seen how things feel like they’re getting more expensive over time.

It’s not just eggs and lunches that get more expensive. Everything does.

Let’s plug some numbers into US Inflation Calculator to illustrate how things really are getting more expensive.

Let’s say you bought something in 2000 for $100. Based on the actual inflation rates between 2000 and 2025, that same $100 item would could $185.71 today.

That’s an increase of 85.7%!

So, by keeping his money in a savings account earning 3% interest, Terry may have thought he was doing the right thing because his balance was getting bigger.

The problem is that while his bank balance was increasing, so was the cost of everything he might want to buy. So, he had more money, but he could buy less things with that money.

That’s what inflation does.

The only way to get ahead of inflation is by investing and earning a higher rate of return.

So to return to our question: was Terry really playing good defense by keeping his money in savings?

No, because his actual purchasing power diminished even though his balance grew.

Investing is about playing offense and playing defense.

By now, you should hopefully be motivated to invest as a way to play offense and play defense.

It’s fun to think about what you can do with your money when it grows with very little effort on your part.

It’s just as important to think about investing as a way to protect your ability to buy the very same things in the future that you buy today.

Instead of being the man who yells at the clouds, you can be the one buying as many eggs and lunches as you want.

That’s cool. It’s never a bad idea to pay a little extra attention to your finances.

Of course, Think and Talk Money readers don’t wait until April to be reminded of all the things we should be doing with our money.

With more than 50 posts already at our disposal, Think and Talk Money readers pay attention to our money year round.

We know how important money is to reaching our ultimate goals in life. That’s why we like to think and talk money just a little bit every week.

Think and Talk Money readers know that personal finance starts with getting our money mindset in the right place. That’s why we create our personal version of Tiara Goals for Financial Freedom.

Is it just me, or are you also noticing more and more businesses charging fees to use credit cards?

I wrote about my disdain for credit card fees recently.

In just the past couple of weeks, I’ve chosen to pay with cash instead of credit card on multiple occasions:

At the butcher shop, which charges a 3% fee, and is kind of smug about it.

At the local ice cream shop, which charges a 4% fee and misleadingly labels it a 4% discount for customers paying in cash.

For the garage door repair guy, who creatively indicates the fee in terms of cash instead of a percentage. In this instance, $11 instead of 3% of the total bill.

At the tree nursery, which also charges a 3% fee for credit cards. This one hurt the most. Trees are expensive! I really would have liked those points.

By paying cash, I avoided hundreds of dollars in fees. Don’t get me wrong, I love credit cards points as much as anyone. But, I just can’t stomach paying these fees to earn the points.

I even ran the numbers recently and determined that the points don’t make up for the added penalty of using a card.

I know many business owners disagree, but in my opinion, these fees are bad for business.

Fees act as a deterrent for me to spend money. I imagine they are a deterrent for others, as well. If I do shop at one of these establishments, I end up being more selective and spending less money than I otherwise would have.

At the butcher shop, I didn’t buy the side items to go with my skirt steaks.

At the ice cream shop, I bought ice cream for my kids but not for myself. Luckily (or unluckily?), my son gave me his leftover, melty Superman ice cream with rainbow sprinkles.

I had no choice with the garage door guy- the garage was broken and needed fixing. You win, garage door guy!

At the tree nursery, I bought half as many trees and plants as I intended.

The way I see it, both the customer and the business lose out because of these fees.

For example, at the nursery, I didn’t get all the plants I wanted. That made me kind of sad.

At the same time, the nursery lost out on more than $1,000 in plant sales. I don’t know how that made the business feel. Obviously, it’s not that sad since it continues to charge the fee.

Taking a broader viewpoint, maybe these credit card fees are actually good for us consumers.

In our consumer-driven society, we all spend too much money when we go out to eat or go shopping. Studies have consistently proven that we spend less money when forced to use cash.

In that sense, a deterrent to spending, which is exactly what these fees are, is probably a good thing for us consumers.

I can’t imagine it’s good for business, though.

What do you think?

It’s OK that tracking your net worth is less fun during a market dip.

I track my net worth once per month using a simple spreadsheet. Today was the first day I updated the spreadsheet since “Liberation Day” and markets dipped.

Like so many others, my net worth took a hit this past month.

That’s not fun.

But, I’m not losing my mind over it.

I’m not saying it feels good. I would much rather see my net worth steadily improving.

I’m just saying I’m not freaking out about it. Time is on my side.

I expect dips like this will occur multiple times throughout my investing timeline.

One thing I’ve found is that it helps to talk about money when things aren’t going well. You realize that you’re not alone. Your friends and family are probably having the same feelings that you’re having.

You don’t have to share how much money you have or how much you lost. You can still benefit emotionally by acknowledging to your loved ones that you’re thinking about the markets a little bit more these days.

People are going bananas for The Bananas.

A reader sent in a great story about a couple who went $1.8 million into debt to start The Savannah Bananas.

If you haven’t heard of The Bananas, they might just be the best story in sports right now.

The Savannah Bananas are the best story in sports.

Owner Jesse Cole and his wife Emily went $1.8 million in debt to start the team, but they now have a broadcast deal with ESPN and will sell two million tickets this year.

Despite countless opportunities to cash in by taking on investors, the owners still own 100% of the team. They continue to do things their way, even if that means foregoing massive profits.

I love stories like this. These owners bet on themselves and found success. Instead of cashing in at the first chance, they’re staying true to themselves.

At the end of the day, they’re making money and seem to enjoy what they’re doing.

Two young coworkers, Terry and Sally, start the same job at the same time making the same amount of money.

While still many years away, Terry and Sally both know that they should invest early and often for retirement.

They each decide to fund a retirement account with an initial contribution of $2,500. They are also dedicated to making contributions of $250 every month until they retire.

Both plan to retire in 40 years while they’re in their 60s.

There’s one major difference between Terry and Sally.

Terry doesn’t like risk. He wants to be able to sleep at night knowing that his hard-earned money is safe and sound in the bank. He can’t stand the idea of potentially losing money from one month to the next.

When Terry wakes up in the morning, he likes to check his bank accounts while he drinks his coffee. He gets a jolt out of opening up his mobile banking app and seeing exactly how much money he has.

In fact, at any given moment, Terry can tell you within a few hundred dollars what his net worth is.

Because Terry doesn’t want to take any chances, he decides to stash all of his retirement savings in a savings account that earns an average annual return of 3%.

Sally is more comfortable with reasonable risk. Upon starting her career, Sally was aware that she had never learned basic personal finance skills. She was determined to put in a little bit of effort early on to set herself up for a prosperous future.

Through the process of educating herself about personal finance, Sally started thinking about what she really wanted out of life. Since she was young and had just started her career, it wasn’t easy to come up with a good answer.

Still, Sally knew that whatever she wanted to do in life, investing was an important part of her financial journey. If she wanted to create more time for herself down the road, she would need passive income from investments to sustain her.

So, after doing her homework, Sally decided to invest her money in a low cost S&P 500 index fund.

While she appreciated that there are no guarantees when it comes to investing, Sally knew that the S&P 500 has historically earned an average annual return of 10%.

Unlike Terry, Sally only checked her accounts once per month when she tracked her net worth and savings rate. Sally slept fine at night because she knew time was on her side.

Let’s see how Terry and Sally turned out 40 years later.

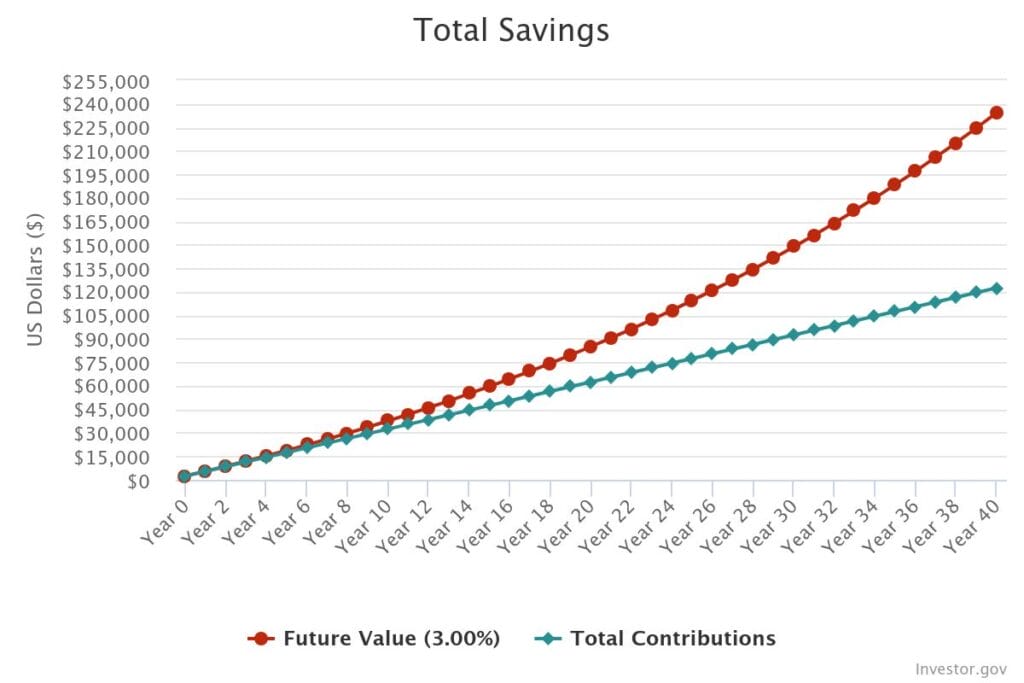

Using a simple online calculator like the one at investor.gov, let’s see how much money Terry and Sally will have in their retirement accounts after 40 years.

After 40 years, Terry will have contributed a total of $122,500.00 to his retirement savings account.

At a 3% interest rate, Terry will have a total of $234,358.87 after 40 years.

In other words, Terry has just about doubled the value of his total contributions in his account.

Not bad, Terry.

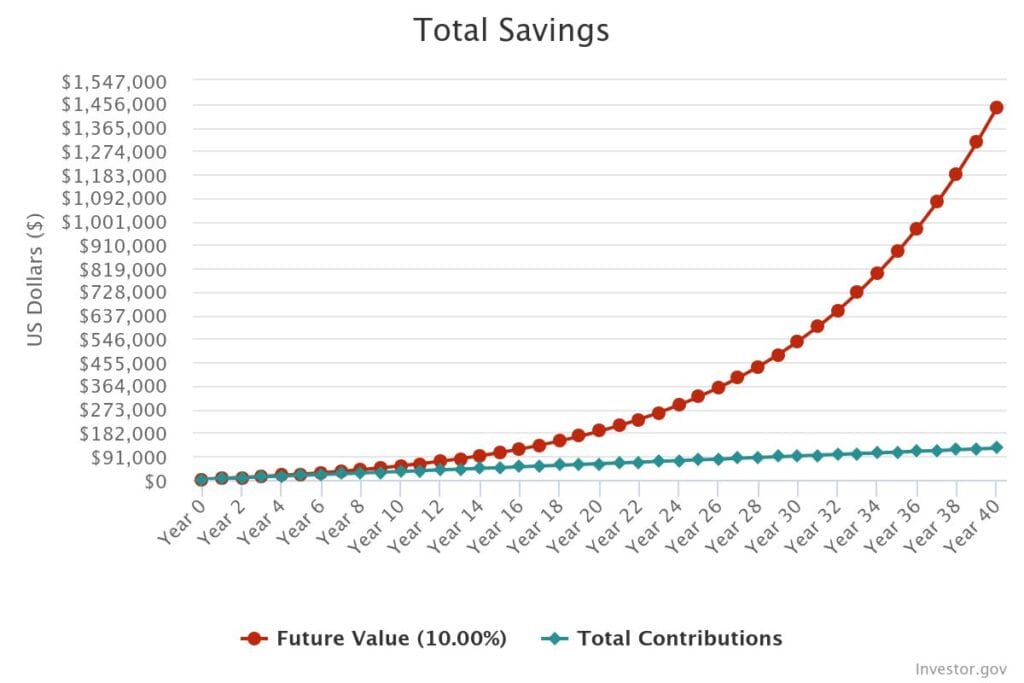

Now, let’s check out Sally’s account.

Sally’s retirement savings total $1,440,925.81.

Sally likewise contributed $122,500.00. After 40 years, at a 10% interest rate, Sally’s retirement account will have a total of $1,440,925.81.

Wow, Sally!

Sally’s retirement account is worth 10 times more than what she personally contributed. Terry failed to even double his account.

Recall in our little hypothetical, Sally did the exact same things as Terry, with one key difference. Sally was more comfortable taking on reasonable risk.

Because Sally was comfortable taking on some risk, her retirement savings were worth more than six times as much as Terry’s savings. She has over a million dollars more than what Terry has!

Look at compound interest in action.

One last thing: take a look at the pictures of Terry and Sally’s investments over time. Notice the gaps between each of their red and blue lines.

While they each benefited from compound interest, Sally benefited exponentially more.

Look at how Terry’s red line stayed much closer to his blue line. Because he wasn’t earning as much overall interest, he didn’t have as much money to multiply from compound interest.

Sally’s red line mirrored her blue line closely for the first 12-15 years. Then, the gap widened before the red line skyrocketed over the final decade or so.

The point of this hypothetical is to introduce the concept of risk when it comes to investing.

We’ve all heard the saying, “You don’t get something for nothing.”

That motto applies to investing as much as anything else. There is always risk involved in investing.

The question is how do you react to that risk.

Some people are so fearful of that risk that they don’t invest at all, like our friend, Terry.

Other people are so desperate to get rich quickly that they take wild risks.

The people that tend to reach and sustain financial independence are the ones who educate themselves and become comfortable with taking on reasonable risk. This is what Sally did.

In future posts, we’ll dive into the various ways you can reduce investment risk.

At this point, knowing why you’re investing and taking on risk is a powerful first step. I was recently reminded of my Money Why when my baby girl was born.

Think of risk as the cost to invest.

If you want to reach true financial independence or any other financial goal, it’s going to cost you something.

Think of risk as the cost to invest.

Sure, there may be some people out there who are able to reach financial independence on a massive salary.

For the rest of us, we’re going to have to get comfortable with investing.

There’s a reason we spend so much time talking about our ultimate life goals. It’s important to embrace the reasons why you’re investing and why you’re opening yourself up to risk.

It never hurts to remind yourself what you are hoping to achieve in the future.

When you know what that thing is, it’s much easier to pay the cost of risk.

When you look at Sally and Terry’s future outlook, who would you rather be?

It’s not really a hard question, right?

It’s not that Sally has a bigger bank account. What matters is that she has created options for herself.

Sally should be in position to do whatever she wants.

Terry probably can’t.

Are you naturally more inclined to act like Terry or Sally?

If you’re more like Terry, have you thought about what outcome in life would be worth taking on some reasonable risk?

There’s an infamous slogan in Chicago politics, “Vote early and often.” My professional advice: don’t do that. Instead, I prefer: “Invest early and often.”

We’ll call it the new Chicago way.

When you invest early and often, you can take advantage of the power of compound interest.

There’s very little we can control when it comes to investing. One of the main things we can control is how early we prioritize investing.

In today’s post, we’ll learn what compound interest is and why it’s so powerful in generating long-term wealth.

Invest early and often to benefit from the magic of compound interest.

Fortunately, the idea of compound interest makes a lot more sense with a simple example.

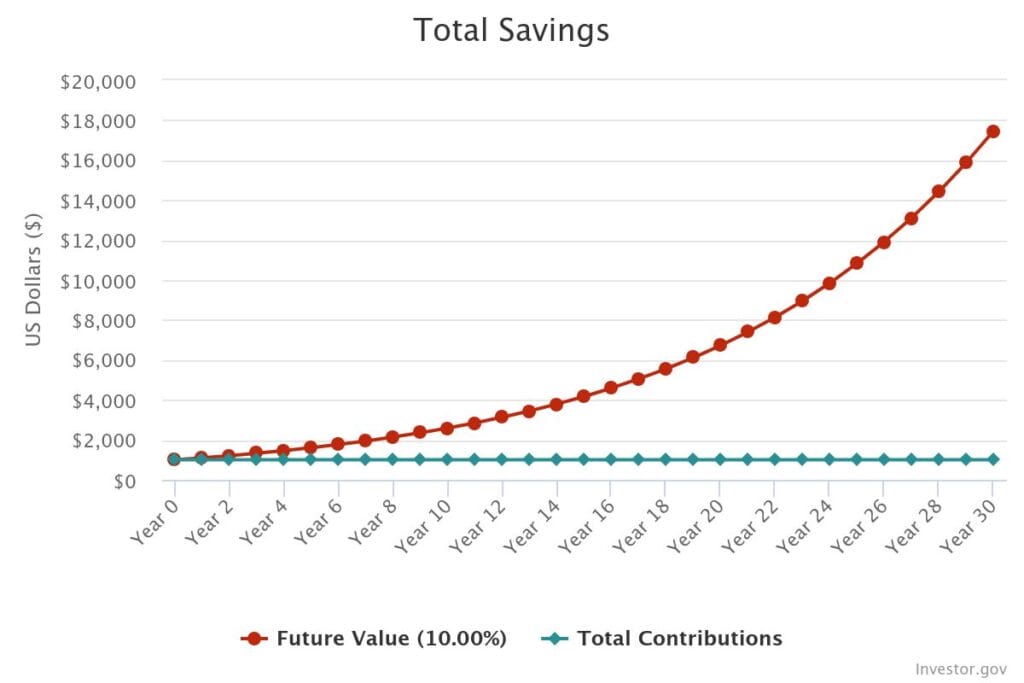

Let’s say you make an initial investment contribution of $1,000. Let’s assume that you earn 10% interest each year on that investment. We will also assume that you re-invest your investment gains.

After the first year, your initial contribution of $1,000 earns $100 in interest (10% of $1,000). That means after one year, you have $1,100 in your investment account.

Because we are re-investing our gains, that means that at the start of year two, yo have $1,100 to invest: $1,000 from your initial contribution plus the $100 earned in interest.

If you earn the same 10% interest on that $1,100 investment, you will have $1,210 at the end of year two.

Notice that in year two, you earned $110 in interest, whereas in year one you earned $100 in interest. That’s because in year 2, you earned interest on the interest your previously earned.

This is the key point about compound interest: you earned more money in year two, even though the interest rate remained the same and you did not contribute any additional money.

That’s how compound interest works. Compound interest is earning interest on interest you’ve previously earned.

So, why is compound interest so powerful?

Earning an additional $10 in interest year two may not seem like a lot.

Over the long run, those additional earnings add up.

Let’s look at an illustration from investor.gov of what happens to that initial $1,000 contribution over a 30-year period:

In 30 years, you will have a total of $17,449.40. That’s a pretty good result from total contributions of only $1,000.

However, for this example, that total is not the important part. The important part is to visualize how compound interest worked its magic to get that result.

Look closely as the two lines on the graph. The blue line that doesn’t change represents your initial $1,000 contribution.

The red line represents the amount of money you have over time.

Notice how in the first 10 years or so, the red line and blue line mirror each other pretty closely. Around year 12, you start to see some separation between the two lines.

While the blue line stays flat, the red line begins to arc upwards. That’s because all that interest you earned during the previous decade has been earning interest. Your investment begins to accelerate upwards without any additional contributions from you.

By the end of year 30, look at how steep the red line is jetting upwards.

We can look at the specific amount of money you’d earn each year in this hypothetical to really drive this point home.

As we mentioned earlier, you earned $100 in interest during year 1. Then, you earned $110 in interest during year 2. That’s a good, but modest, increase.

During year 12, you earned $285.31 in interest. That’s significantly more than you earned in the early years, all without any additional contributions on your part.

During year 30, you earned $1,586.31 in interest!

The more time that you stay invested, the more money you’ll earn as compound interest works its magic.

That’s the power of compound interest.

Invest early and often to be a millionaire with very little effort on your part.

Compound interest is so powerful that it can make you a millionaire with very little effort on your part. All it takes is time and consistency.

In other words, invest early and often.

Let’s look at another example to see how you can easily become a millionaire if you invest early and often.

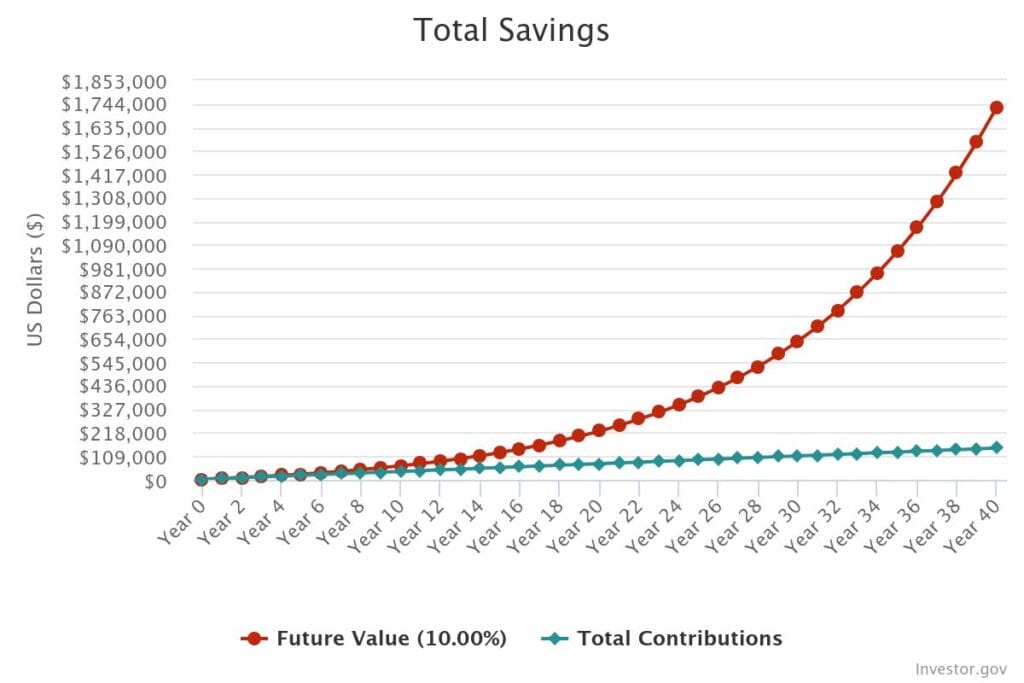

Let’s say you begin your career after going to law school or grad school at age 25. During your first year working, you saved up $3,000 and decided to invest in a low cost index fund.

You also make a plan to contribute an additional $300 per month to your investment account for the next 40 years, setting yourself up to retire at age 65.

We’ll also assume you earn the same 10% interest from our prior example, and you don’t make any withdrawals from your account.

By the time you reach retirement age, you’ll have $1,729,110.97 in your retirement account!

That’s after contributing only $3,000 initially and $300 per month after that.

Put another way, your total contributions of only $147,000 turns into $1,729.110.97 by the end of your career.

Let’s look at the graph corresponding with these figures to once again visualize compound interest at work.

You’ll notice this graph looks almost identical to our prior example, even with the additional contributions that you make over time.

You can once again see that the blue and red lines mirror each other closely for the first 10-15 years.

Then, the blue line stays relatively flat while the red line gradually arcs up before skyrocketing towards the end.

Your personal investment picture should look similar in the long run.

Now, there’s no way to predict exactly when you’ll start to notice the magic of compound interest. There are too many variables at play.

The point is that given enough time, your personal investment trajectory should look similar because of compound interest.

You can play with the numbers in an investment calculator like the one available at investor.gov to match your personal situation.

If you’ve created a Budget After Thinking, you may be able to invest much more than $300 per month.

No matter what initial contribution you make and what interest rate you assume, you should notice a similar investment picture over the long run.

When I say investing is the easy part, this is what I mean.

I just showed you how an early contribution of $3,000 and regular contributions of $300 can turn into more than $1.7 million.

You don’t have to understand the math behind compound interest.

You just have to trust that it works.

Then, invest early and often.

Given enough time, assuming normal, historical market conditions, your investments will gradually increase before shooting up in the later years.

Read that sentence again. “Given enough time” is the key phrase.

The magic behind compound interest is time.

The earlier you can start investing, the better off you will be.

Since we can’t control investment returns, I prefer to focus on what we can control when it comes to investing.

We can control when we start investing and how long we invest for.

By making regular contributions over a long period of time, compound interest ensures that your wealth will grow.

Invest early and often.

$3,000,000 today or a penny that doubles each day for the next 30 days?

Let’s look at one more fun example to demonstrate the power of compound interest.

At the start of each personal finance class I teach, I ask my students this question:

“Would you rather have $3,000,000 today or one penny that doubles each day for the next 30 days?”

Maybe the fact that I’m asking the question in the first place gives away the answer. Still, some students refuse to believe that the penny could grow to more than $3,000,000 in 30 days.

The real lesson in asking this question is not that the penny ends up being worth more. The lesson is that it’s not until the very end of the time period that the penny takes the lead.

If you chose the penny, for the first 20 days, you’d be feeling pretty foolish. Even after 29 days, the penny still hasn’t outpaced the guaranteed $3,000,000.

Then, by day 30, you realize the full power of compound interest. The penny ends up being worth $5,368,709.12!

Just like we saw with our prior examples, it takes time for the magic of compound interest to do its thing.

When it comes to investing, time is the most important factor that we can control. The more time you spend in the markets, the better chance you have of significantly increasing your wealth.

People smarter than you and me preach the power of compound interest.

Warren Buffett, the world’s greatest investor, fully appreciates the power of compound interest. He’s famous for saying that his favorite holding period for an asset is “forever”.

Buffet’s not literally saying that there’s never a time or reason to sell an asset, like a a stock. He’s simply making the point that compound interest benefits people who stay invested over the long term.

If the world’s greatest investor isn’t impressive enough for you, how about the world’s greatest thinker?

Albert Einstein is often credited with this famous quote about compound interest:

Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.

You don’t have to be as smart as Buffet or Einstein to benefit from compound interest.

You just have to invest early and often.

The Chicago Way: Invest early and often.

Let’s recap:

Voting early and often = bad idea.

Investing early and often = good idea.

Whether you are new to investing or have been investing for some time, never underestimate the power of compound interest.

It will take time before you see results. But, the only way you’re going to get those results is by staying patient and staying invested.

When you’re tempted to pull out of the market, remind yourself that investing is a long-term game.

Picture the graphs that show how your money can skyrocket with enough time. Remember the question about the penny doubling for 30 days. Don’t ignore the words of Buffett and Einstein.

Investing is a major part of leading a healthy financial life.

It also should be the easiest part.

Despite all the attention, news, and marketing, investing doesn’t have to be complicated.

Investing simply means committing money now to earn a financial return later. This is why I refer to money I invest as Later Money.

To be honest, the most difficult part of investing is continuously generating money to invest in the first place.

The actual investing part is pretty easy.

That’s because when you invest the right way, your money should earn more money without much additional effort from you.

This is the best part about investing. Your money can (and should) grow over time without your active participation. This is why investment gains are often referred to as “passive income.”

If you are on a journey towards financial independence, you know how important passive income is. The best way to get your time back is to earn money passively through investments while you’re off doing something else.

We’ll soon learn why investing does not have to be complicated. If you can drown out the noise, all you’ll really need to do is regularly fund your investment accounts and watch your net worth slowly grow.

This is when personal finance starts to get really fun.

Investing is when personal finance starts getting really fun.

When you’ve invested the right way, your wealth will slowly multiply. You won’t notice it at first. Trust me, give it time.

You’ll soon see that all the effort you put into educating yourself about money was more than worth it.

No, you won’t be immune from market swings like the one we’re in right now.

But, you’ll be educated enough to not panic. You’ll know that time is on your side.

Have you noticed that we’re now 50 posts in and have hardly talked about investing?

There’s a reason we’ve hardly talked about investing in the first 50 posts of Think and Talk Money.

In order to get the benefits of investing, you need to have the right money mindset. That means knowing why you’re investing in the first place. Without the right motivation, you will struggle to consistently fund your accounts.

After all, when you invest, you are sacrificing money you could spend right now for the opportunity to spend even more later on. Without the right motivation, too many people put off, or give up on, investing altogether.

When they do that, they have a little more money to spend today. But, years from now, they will wonder why they’re still working so hard and don’t see an end it sight.

Your goal may be to pay for your kids’ college. One way to do that is to take advantage of 529 college savings plans.

You may not know exactly what you want down the road. That’s OK, too. Whatever it is, investing now will make it easier to pursue whatever that thing ends up being.

Once your mindset is in the right place, you’ll be more determined to craft a budget that consistently creates money to invest.

Think about it: would you rather be someone who invests $1,000 one time or someone who invests $1,000 every month?

If you practice solid personal finance fundamentals, you can be the person consistently investing to accomplish your ultimate life goals.

Too many people think personal finance is only about investing.

Too many people skip over the part where we learn strong personal finance habits. These people think that personal finance is only about investing.

Let’s play a game. Walk down the hall at your office and ask the first person you see what they know about personal finance.

I’m guessing you’re going to get a response like:

“Personal finance? Oh, yes. I need to learn that. I don’t know anything about the stock market.”

If I’m right, leave a comment below. This should be fun.

By the way, people that assume personal finance is only about investing are not bad people. They just haven’t been properly educated. Just like me when I set $93,000 on fire.

By now, you know that personal finance is about so much more than investing. You know that you need to develop strong habits so you constantly have money to invest in the first place.

And, you’ll soon learn that investing is really the easy part.

When you learn basic investing principles, like minimizing fees and playing the long game, your money can slowly grow over time.

As that happens, you move closer and closer to financial independence without much effort at all.

It’s actually pretty easy.

We’ll cover these basic principles in upcoming posts.

One thing we won’t discuss at Think and Talk Money is the latest hot stock tip.

If you want to study P/E ratios and company balance sheets in a quest for the best individual stocks, I won’t stop you.

I just won’t be joining you.

That’s because it’s very hard to pick winning stocks. Even the “experts” have a very hard time doing it consistently.

You don’t believe me, do you?

What if I told you that the vast majority of investment pros underperform the S&P 500?

Making matters worse is that the professionals, who the average investor might turn to for guidance, have poor track records. In the past decade, an alarming 85% of U.S.-based active fund managers underperformed the broader S&P 500. Those who invest in these funds are essentially paying for unsatisfactory results.

If the “pros” can’t beat typical market returns that are available on the cheap for all of us… why even play that game?

Why overcomplicate things?

Sure, maybe you’ll get lucky and your investment pro is one of the few who can beat the market. Odds are that if your pro beat the market one year, he probably won’t the next year.

If that’s your game, I wish you nothing but good fortune.

Personally, I’d rather do things the easy way. I’d rather focus on what I can control, like how much money I’m contributing to my investment accounts each month.

And, that brings us to an interesting point.

Even if you are working with a professional, you are not excused from participating in your investment journey. You still need to understand the basics.

Plus, while you may not be watching your portfolio closely, your job is always to make sure there is consistent money to be invested.

My guess (or is it hope?) is that your advisor has told you as much.

Investing is a major component of financial independence.

Whether you are striving for financial independence, or hoping to maintain it, investing is a major component.

To be a successful investor, you first need to practice strong financial habits.

Don’t worry. If your mind is in the right place, the investing part is actually pretty easy.

Back in 2008, I was a third-year law student. My entire life savings at that point was about $10,000. A lot of this money came from savings bonds gifted to me by my grandma for my birthday since the year I was born.

I mentioned the year was 2008, otherwise known as the beginning of The Great Recession. As detailed in Forbes Advisor:

The Great Recession of 2008 to 2009 was the worst economic downturn in the U.S. since the Great Depression. Domestic product declined 4.3%, the unemployment rate doubled to more than 10%, home prices fell roughly 30% and at its worst point, the S&P 500 was down 57% from its highs.

Suffice it to say, 2008 was not a great time to be graduating or looking for jobs.

Those of my friends fortunate enough to have secured a job offer soon learned that their offers were being rescinded. Such were the times.

But, I digress.

Back to how I set $93,000 on fire.

As I mentioned, my life savings at the time totaled about $10,000. I had previously decided to use a financial advisor to invest my money for me.

I had been working with this financial advisor for a few years prior to The Great Recession.

All these years later, I couldn’t tell you what she had me invested in prior to the markets imploding. I’m assuming that she took into account my age and risk tolerance and designed a suitable portfolio for me.

What I can tell you is that my portfolio suffered the same fate as just about everyone else towards the end of 2008. My $10,000 balance was shrinking.

At that point, my advisor took me out of the markets and stashed the remainder of my money in a savings account earning close to 0% interest.

I didn’t notice this maneuver right away. In fact, it wasn’t until 2010 that I noticed that my money was sitting in a savings account.

When I finally caught on that my account balance had not changed for a couple years, I called my advisor. She explained that she had pulled me out of my investments when things weren’t looking too good.

She didn’t have a good explanation for why I was still in the savings account in 2010. To be honest, it seemed like maybe she forgot about me.

By that point, the markets were improving. I had already missed all of the upswing from 2009. Since I had felt neglected, I withdrew my money and closed my account.

I wish I could tell you that I started investing on my own at that point.

Nope, that’s not how you set $93,000 on fire.

Instead of investing, I let the money sit in my checking account until it just kind of disappeared. I had no plan for the money. All these years later, I have no clue what I spent it on. I just know that it disappeared.

But Matt, you said you only invested $10,000. How did you end up setting $93,000 on fire?

I’m glad you asked.

If I had known then what I know now, I would have invested that $10,000 in a low-cost S&P 500 index fund.

I also would not have taken my money out of that S&P 500 index fund when the markets dropped.

Time was on my side. The smart thing would have been to do nothing at all.

Between the start of 2009 and the end of 2024, the S&P 500 earned an average annual return of 14.98%.

That means my $10,000 invested in a low-cost S&P 500 index fund at the start of 2009 would have been worth $93,265.90 by the end of 2024.

That, my friends, is how I set $93,000 on fire.

And, I have nobody to blame but myself.

Let me make one point perfectly clear:

It’s nobody’s fault but my own that I missed out on those earnings.

It was my fault for not taking a more interested, and educated, approach to my personal finances.

In a way, I’m glad I learned that lesson with only $10,000 at stake instead of later in life when I had more to lose.

It’s not my financial adviser’s fault. She did what she thought was best. For some people, her strategy was probably successful.

My problem was I blindly trusted my adviser without educating myself first. I didn’t know the right questions to ask. I didn’t understand the plan.Worst of all, I didn’t pay attention when my account statements arrived in the mail each month.

In my mind, once I transferred my money over to my advisor, I was excused from taking any responsibility for my future.

That was a mistake I’ll never make it again. When things didn’t go well, I had no one to blame but myself.

We all need to understand the basics of investing.

Whether you choose to work with an advisor or not, it’s up to each of us take accountability for our own future.

We need to educate ourselves enough to be part of the planning process. We need to know why we’re taking certain steps and be savvy enough to ask the right questions.

You may be more comfortable working with a financial advisor. That’s perfectly fine. You still need to understand the basics of investing.

My problem in 2008 and 2009 was that I hadn’t educated myself. I like to share this little story to illustrate how important it is to pay attention to our finances.

These days, I manage my own investments. I’ve determined that paying fees for someone else to manage my money is not worth it to me.

By the way, we’re going to spend a lot of time talking about fees so you can decide for yourself if you want to pay them.

Whether you manage your own investments or you use an adviser, it’s critical to understand the basics about investing in the stock market. The good news is the basic principles of investing are relatively straightforward.

Always remember: there are some things we can control and a lot of things we can’t control.

We’re going to focus on what we can control.

That means focusing on how much fuel you’re generating each month to invest in the first place.

Then, it means minimizing fees and maximizing your time in the market.

If you can successfully implement just those ideas, you will wake up years from now with major gains to your net worth due to the power of compound interest.

There are other strategies we’ll cover, as well. You’ve likely heard fancy terms like “diversification” and “asset allocation.” We’ll talk about what those phrases mean with the goal of convincing you that investing does not have to be complicated.

That’s right. Investing does not have to be complicated.

You don’t have to read the Wall Street Journal. You don’t have to study financial statements. Even people who do that for a living struggle to predict what’s going to happen next.

So, let’s not waste our time. We’ve got better things to do on our way to financial independence than studying corporate balance sheets.

With even just a little bit of knowledge, you can feel comfortable and confident investing in the stock market. Then, all you’ll need to stay on track is the occasional reminder to think and talk about money with your loved ones.

I’m further away from financial independence today than I was five years ago.

You know what’s funny?

I couldn’t be happier about where I am today.

Let me explain.

In 2020, my wife and I had very minimal expenses.

At the start of 2020, my wife and I were both working as lawyers in Chicago. We lived in an apartment in a 4-flat that we had purchased in 2018. We had no kids at the start of the year, but were about to welcome our first.

This was a good apartment in a popular part of town. It had 3 bedrooms and 2.5 bathrooms. That was plenty of space for my wife and I, and eventually the two babies we brought home there.

We purchased this 4-flat from a real estate investor who had done a decent job on the renovation. It had in-unit washer/dryer, modern finishes, and plenty of storage.

We had a small outdoor patio with enough room for a grill and little table. We also had a garage parking space but ended up parking our 20-year-old car on the street most days.

When we purchased the building, it was the most expensive 4-flat that had ever been sold in that part of town. It was a bit of a risk to set the high-water mark in the area.

Even though the building was expensive for the area, this was not a fancy apartment. This part of town was still up-and-coming. Some people probably thought it was not a nice part of town.

I doubt many people came over and thought, “Wow, look at this amazing apartment!”

The more likely reaction was probably something like, “What the heck are they doing?”

To be fair, I asked myself that question plenty of times.

So, what were we doing?

We were paying ourselves to live there.

Say that again?

My wife and I paid ourselves to live in that apartment.

We lived for free. And made a profit at the same time.

See, the rental income from the other three units covered the entire mortgage plus all expenses for the property.

But, that’s not all. On top of covering all the expenses, the rental units generated a profit of $1,000 per month on average.

So, not only did we spend zero dollars each month on housing, we profited $1,000 per month.

Looking back, getting paid to live in a decent apartment was maybe the best decision we ever made.

What happens to your finances when you live for free?

Let’s take a look at how living for free can be a major advantage on your way to financial freedom.

The common wisdom is for people to spend no more than 30% of their gross income on housing. Regardless of how much you make, that usually means thousands of dollars.

Because our tenants were paying our living expenses for us, we did not have that expense for the five years we lived in that apartment.

In other words, we didn’t have to worry about budgeting for housing.

We also drove a nearly 20-year-old car and could walk to the “L” (Chicago’s subway). We lived in a neighborhood with plenty of nearby restaurants and shops. That meant our transportation costs were next to nothing.

Because we weren’t paying for housing and had very minimal transportation costs, we could supercharge our savings.

How much were we able to save?

Let’s take a look.

Between 2018 and 2023, my wife and I acquired three buildings and ten apartments in that same neighborhood. We’re very familiar with market rents in the area.

We rent our apartments for anywhere from $2,300 to $3,600 per month. Our usual tenants are professionals like engineers, lawyers, doctors, consultants, and pilots.

The unit we were living in from 2018 to 2022 was one of our larger units. At the time, it would have rented for $3,500 per month on average. That equals $42,000 per year to rent that apartment.

Keep in mind, if someone was paying rent to live there, that would be $42,000 of after-tax money.

Since we owned the building, we lived there for free. We could save that $42,000 we would have otherwise paid in rent. Instead of spending that savings on things we didn’t need, we were able to save that money for our next real estate investment.

Plus, we earned $1,000 on average per month while we lived there. That’s an additional $12,000 per year in profit.

We lived in that unit for almost five years.

Add it all up and we saved $270,000 by living in that apartment for five years.

$42,000 saved rent x 5 years =$210,000.

$12,000 profits x 5 years = $60,000.

Total savings = $270,000

We used that $270,000 for a downpayment on a rental condo in Colorado ski country.

It took five years of living in a decent, but not-awesome, apartment to have a ski condo that will hopefully be in our family for decades.

Choosing to live in our 4-flat to save $270,000 over five years was one of the best financial decisions we’ve ever made.

I highly recommend you consider house hacking if you’d like to start investing in real estate.

Many of you are familiar with the strategy of living in a building (or home) you own while tenants (or roommates) pay for it. Brandon Turner, of BiggerPockets fame, popularized the concept he dubbed “House Hacking”.

You can read all about house hacking on BiggerPockets here.

Without a doubt, there is no better strategy for entry level real estate investors than house hacking. I gave you a glimpse of the financial upside earlier in this post.

Besides the financial upside, it’s like landlording with training wheels. Since you live on site, you can more easily learn how to manage a rental property, including responding to tenants and handling routine maintenance.

The naysayers will say something like, “I don’t want to live with my tenants. They’re going to stress me out. I don’t want to be bothered at 2 a.m.”

Ignore them.

My wife and I lived with our tenants for five years at this property and two more years at a subsequent property. We did this while working full-time jobs as lawyers and raising two kids.

Because we didn’t listen to the naysayers, we now have four income-generating properties and our “forever home” just outside Chicago.

Even though we’re no longer living for free, the income from our rental properties is enough to cover the expenses of our home.

So, why am I further away from financial independence today?

I’m further away from financial independence today because my expenses have gone up since 2020. I’ve already alluded to those increased expenses throughout the post.

In 2020, we had our first child. Now, we have three children.

Also, after seven years of house hacking, we decided it was time to purchase a long-term home for our growing family just outside the city in a terrific area.

We also finally traded in our 21-year-old car for our first new car ever.

How’s this for easy math:

Three Children + Nice House + New Car = Further Away from Financial Independence

While that combination means I’m further away from reaching financial independence, I now have everything that I could possibly ever want.

That’s why I couldn’t be happier with where I’m at today.

My end game is finally in sight. Five years ago, I didn’t know where I’d be living or what car I’d be driving or what my family situation might be.

Now, the picture is clear.

I can calculate with reasonable certainty how much money I need to be truly financially independent. I can use that number as a target and make every financial decision with that target in mind.

That’s why in 2025, I’m focused on paying down HELOC debt. Each time I make a debt payment, I move closer to financial independence.

I have no intentions of retiring any time soon. Retiring early is not, and has never been, my goal.

My goal is to become financially independent to create as many options as possible to protect myself and my family. I want to be financially independent so I can pivot no matter what life throws at me.

If my goal was to retire early, I may have skipped the single family home in a great neighborhood. I could have continued house hacking, minimized my expenses, and lived off of the rest of the rental income.

But, I want more for me and my family. I don’t want to just survive.

Have you delayed financial independence to craft the life you really want?

My life has certainly changed in the past five years, but all that change has been for the better.

That meant house hacking at first to keep expenses as low as possible. Now it means enjoying the wealth I created by making those earlier sacrifices.

In order to have the life I want, I needed to temporarily move further away from financial independence.

Still, I’m confident that I’ve taken the right steps to not just reach financial independence, but to reach it while living the life I want.

The tradeoff is that it will take me longer to be truly financially independent. I’m perfectly happy with that.

Financial independence has never been more clearly in sight. It’s just delayed a little bit.

Is your goal to reach FIPE and pivot as quickly as possible?

Or, are you OK with delaying FIPE temporarily for the life you truly want?

We focus a lot on financial independence here at Think and Talk Money. That’s because achieving financial independence is the ultimate goal for most of us.

To me, financial independence does not mean retiring.

That’s why I don’t like the popular acronym, FIRE: Financial Independence, Retire Early.

Instead, I I like to view my financial freedom journey as FIPE: Financial Independence, Pivot Early.

Let me explain why I believe in FIPE not FIRE.

FIPE = Financial Independence, Pivot Early

Whatever it is that you truly want to do in life, financial independence makes it possible.

When you have financial independence, you have options. You can make decisions based on your core values instead of making decisions based on money. You can pivot, if necessary.

Financial independence is for people who want to be empowered to take more control of what they do with their working hours.

It’s not about quitting work. It’s about the freedom to pivot to other work, if you want. I’m convinced that humans are meant to be productive. We are social creatures who at our core want to be contributing.

That doesn’t mean we have to be or want to be employees. But, it does mean that we want to do something meaningful with our working hours every week.

That’s why I believe in the power of pivoting, not retiring.

Why I don’t like the name FIRE.

Part of the misconception about financial independence may stem from the name of the popular personal finance concept known as FIRE: Financial Independence, Retire Early.

It’s not uncommon for people to hear financial independence and immediately think that’s only for people who want to quit their jobs and retire. That’s how widespread FIRE has become in the personal finance space.

I agree with so many of the principles of FIRE. I just don’t agree with the name.

Financial independence is about much more than retiring early.

FIRE emphasizes saving more and spending less until you reach the point where your passive investments generate enough income to allow you to quit your job.

I love this part of FIRE: the idea of creating enough income streams so that you have the freedom to do what you want with your time. I share the primary goal of saving more money and spending less to achieve more life freedom.

I call this Parachute Money. I like to view each income stream as a separate parachute string. The more parachute strings you have, the safer it is to make a big change in life.

The problem for me is that the FIRE end game is suggested right there in the name: become financially independent so you can retire.

I don’t like that part. I don’t like what the word “retire” implies.

If you look it up, you’ll see that the word “retire“means to withdraw, to retreat, to recede.

None of those things sound appealing to me at all.

Each word implies moving backwards. I’m not working so hard to achieve financial freedom so I can move backwards in life.

I prefer to think of financial independence in terms of creating options. I prefer to think of financial independence as a way to move forward in life.

I think “pivot” better reflects that mission.

Pivot means to adapt or improve through modifications and adjustments.

That sounds so much more appealing to me.

With FIPE, financial independence is still the primary goal. But, the endgame is not to withdraw or retreat. The endgame is to adapt and improve how you spend your working hours.

FIPE = Financial Independence, Pivot Early.

Granted, the name “FIPE” is not as catchy as FIRE.

But, I think it actually better encapsulates the entire purpose of financial independence in the first place.

To explain, let’s look back at the modern day origin of FIRE for a minute.

Vicki Robin and Joe Dominguez are often credited for laying the groundwork for the modern day FIRE movement. Robin and Dominguez wrote an incredible book called Your Money or Your Life.

It’s one of my favorite personal finance books. You should definitely read it if financial independence is important to you.

In their book, Robin and Dominguez have a lot to say about the relationship between money, work, and time.

Guess what?

Most of us are doing it all wrong.

Most of us make the mistake of chasing money at the cost of our precious time. When you read Your Money or Your Life, you will start to value your time for what it’s really worth.

By making good choices about how to earn money- and as importantly what to do with that money- you can get the most out of your money and your life.

That’s what FIRE is really all about. It’s about choosing to use your working hours in a way that is more meaningful to you than clocking in-and-out as an employee each day.

It’s not about retiring from meaningful work. It’s about pivoting to work that is more meaningful to you.

FIRE proponents would likely agree that the goal is not to withdraw or retreat.

I think proponents of FIRE would actually agree with me that the end game is really not about withdrawing or retreating. The mission is always about moving forward, not backwards.

My belief is that people who are disciplined and skilled enough to reach financial independence in the first place are the type of people who don’t retreat or withdraw.

They may opt for periods of temporary retirement, as they should. But, I don’t think financially independent people are truly wired for full-time retirement.

That’s why you see so many people who have obtained financial independence continue to pursue income streams.

That might mean managing real estate investments, teaching others, or even starting a financial freedom blog.

So, technically speaking, most people who have obtained financial independence have not actually retired. They haven’t withdrawn or retreated. Instead, they have pivoted.

They are now spending their working hours doing other things. They may not be working full-time for an employer, but they’re still working.

They’ve achieved financial independence and have earned the right to pivot.

Financial Independence, Pivot Early.

Even FIRE leaders would likely agree that the end game is not to completely retire.

FIRE is not about retiring or quitting. It’s about pivoting to more meaningful life pursuits.

I don’t want to speak for Robin, but I think this is what she was getting at.

I just think the name FIRE doesn’t accurately portray the mission. Pivoting early seems more appropriate to me than retiring early.

We all have the same goals in mind: financial independence. And, I believe we have the same end game in mind: pivoting to more meaningful work.

That’s why I like FIPE instead of FIRE.

Are you looking to retire early or simply to pivot?

What is it that you’re aiming for by getting your personal finances in order? If you want to retire early, there’s nothing at all wrong with that. You may be at the point in your career and life where that makes sense.

Personally, I’m not looking to retire early. That’s why I like to view financial independence as a chance to pivot.

Pivoting doesn’t mean you have to switch jobs or change things up just for the sake of change. It just means that you have that option if you want it or need it.

By the way, I’m not alone in viewing financial independence as a chance to pivot instead of retire.

I’m in complete alignment with Trench. I like almost everything about FIRE, just not what the name implies.

With FIPE, the goal is not to retire. The goal is to give yourself the freedom to choose what to do next.

Whether you want to retire early or just pivot to a new chapter in your life, being good with money is key.

Do you like the name FIRE or FIPE?

At the end of the day, whether you like to view it as FIRE or FIPE, the mission is the same. We are all looking for the freedom to choose what to do next.

When striving for financial independence, the goal is to create options. Those options likely include pivoting to more meaningful work, rather than withdrawing or retreating.

Personally, I think the name FIPE better encapsulates that mission.

Do you agree?

What name resonates more with you on your financial freedom journey?

Are you interested in retiring early or pivoting early?

Financial freedom doesn’t happen overnight. I’ve been on my journey to financial freedom for more than a decade.

I’m not there yet.

Here’s a look at how my journey to financial freedom has progressed since I graduated law school in 2009.

My journey to financial freedom began in my late-20s and was focused on eliminating debt.

In my 20s, I needed to pay off credit card debt and student loan debt. All I knew about the journey to financial freedom back then was that it seemed very far away.

I started budgeting, which meant reigning in my spending on things I didn’t really care about.

I began to establish good money habits. It wasn’t easy, and I was far from perfect. That’s OK. The 80/20 rule reminds us that we don’t need to aim for perfection.

By the way, my life didn’t all of a sudden become boring and miserable when I became more money conscious. Quite the opposite, actually.

I became more confident in myself because I had a plan. I no longer felt like I was sliding backwards. With each paycheck, I moved one step closer to erasing my debt. That was a powerful feeling.

In my early-30s, my journey to financial freedom was about fueling my savings.

By the time I turned 30, I had paid off my credit card debt and my student loan debt. I’ll never forget the day I made my last student loan payment as my family and I were heading out to Colorado. A huge weight had been lifted from my shoulders.

I felt free. My journey to financial freedom was still in the early stages, but I was on my way. Most importantly, I still had good habits and a plan.

The money I had been allocating to student loan and credit card debt could now be put towards more fun goals and experiences.

Instead of aimlessly spending the thousands of dollars each month that had been going towards debt, I rolled that money directly into savings. Highest on my list was saving for an engagement ring.

Within a year, I had enough saved to purchase the ring. I thought being free from debt was strong motivation. Turns out that motivation was nothing compared to the desire to buy a ring for the woman you love.

As your career progresses and you earn more money, you will benefit from strong personal finance habits.

As my career progressed, like many of you, I started earning more money. When I earned more, I did my best to use that additional income as fuel for my goals.

I’m grateful I had previously learned strong personal finance habits on my journey to financial freedom when I earned relatively little.

For most of us, our usual career progression is the exact opposite of the typical lottery winner. Who hasn’t heard the stories about the lottery winners that hit it big and then quickly go broke?

These stories are unfortunately all too common. What starts out with so much elation usually ends in tragedy.

The normal downfall involves unrestrained spending on things like houses, cars, and extravagant nights out. It also involves the pressure to give money away to family, friends, and charities.

The challenge is the same for lottery winners and professional athletes. They come into a lot of money suddenly without any prior personal finance education. When this happens, that money disappears quickly.

What can we learn from lottery winners and professional athletes?

I think it’s safe to say that none of us are going to win the lottery or earn millions as a professional athlete. I hope I’m wrong about that!

But, we can still fall victim to the same set of challenges on the journey to financial freedom. It may not be a sudden rise and then an equally sudden drop-off. Our financial growth presents itself more slowly.

Over time, we may earn referrals/commissions, raises, and bonuses. These earnings certainly add up and can make a huge difference in our lives, if we have a plan. That’s a big “if” for most of us.

I didn’t have the full plan figured out in my 20s. Our goals change as life changes. There’s nothing wrong with that.

That said, because of the steps I took in my 20s to learn about personal finance, I was better prepared for the opportunities and challenges that arose in my 30s. I learned that when you create a solid foundation for yourself, you have options.

To me, life is all about giving yourself options. Nobody likes feeling stuck, including me.

In my mid-30s, my journey to financial freedom was about building wealth through real estate.

Besides saving for an engagement ring and a wedding, I was able to save up for a downpayment on a home. At the time I started saving up for a home, I had no idea that I could use my savings to invest in real estate.

It wasn’t until I went to a Cubs game with a good friend of mine, The Professor, that I learned about real estate investing.

This is when my journey to financial freedom really accelerated.

See, The Professor had a beautiful condo with an incredible rooftop deck near Wrigley Field. During the game, he told me he was selling the condo and moving into a 4-flat with his fiancee in an up-and-coming part of town.

Huh?

Why on earth would you give up your amazing condo?And move to a random neighborhood I’d maybe been to one time in my life?

I thought The Professor had lost his mind. Back then, I had no idea what a 4-flat even was. I couldn’t even point to his new neighborhood on a map of Chicago.

The Professor set me straight.

He walked me through the numbers. He explained that he was going from paying $3,000 per month for his condo to receiving $700 per month on top of living for free in the 4-flat. That’s a $3,700 difference per month!

The Professor also introduced me to BiggerPockets. That was huge for me because I believe in the motto, “Trust but verify.”

Over the next week, I read everything I could and listened to podcasts every day. It didn’t take long before I was convinced that I wanted a 4-flat of my own.

Eight years later, I own three buildings and 10 apartments in that same Chicago neighborhood. I have a ski rental condo in Colorado.

Without that great talk with The Professor, I don’t think I would be where I am today on my journey to financial freedom.

We all need to position ourselves to benefit when luck comes our way.

I was fortunate to have learned from The Professor’s experience. We all need some luck on the journey to financial freedom. I’m convinced that we’ll all catch a break here or there. The question is what we do with that luck when it comes our way.

If I hadn’t taken the time to learn about personal finance in my 20s, I wouldn’t have been positioned to benefit from that conversation with The Professor.

That’s why I say the journey to financial freedom doesn’t happen over night. It’s about one building block at a time.

For any aspiring real estate investors out there, please take that message to heart. Before you can successfully invest in real estate, you have to invest in your own financial literacy.

I’ve learned firsthand that the same principles that apply to personal finances apply to managing a real estate portfolio. Each pursuit takes a plan that only works with discipline and patience.

In my late-30s, my journey to financial freedom was about paying off debt.

In my late-30s, my journey to financial freedom pivoted from acquiring properties to optimizing my portfolio. My wife and I decided we were ready to transition from growing our real estate portfolio to paying off our debt.

In a way, I’ve come full circle on my journey to financial freedom.

Reading Small and Mighty Real Estate Investorhelped us conclude that at this point in our lives, we have enough. Our portfolio generates enough income to help fuel our current goals. If we were to continue expanding, the headaches could end up outweighing the financial benefits.

In the short term, that mortgage debt pulls me further away from financial freedom.

If my plan works, that same debt will push me more rapidly to financial freedom.

Financial freedom through real estate has existed for decades, if not centuries.

By the way, I didn’t invent the plan of achieving financial freedom through real estate. That idea has existed for decades, if not centuries. I’d avoid anyone who tells you they pioneered this concept.

Years ago, I remember sharing my newfound passion for real estate with mom. She had this smile on her face as I excitedly shared this “new” phenomenon of investing in real estate to achieve financial freedom.

The next time I saw her, I realized her smile was actually more of a smirk.

It’s natural to want to jump to the finish line. I’m guilty of that, too. I think about achieving financial freedom every day and need to remind myself to take it one step at a time.

Even with all I’ve learned about personal finance, it can sometimes feel like I’m heading in the wrong direction.

Wherever you currently are on your journey to financial freedom, remember that it doesn’t happen over night. I need to constantly remind myself to stay the course.

Keep coming back to Think and Talk Money for daily reminders that financial freedom is within all of our grasps.

I had the happiest occasion to think about that question this past week.

My wife and I welcomed our third child, a little baby girl.

We were very fortunate and had a smooth delivery process.

Even so, when you’re in the delivery room, your mind runs wild. You just want everything to go well. It’s completely out of your hands by that point.

Things get really interesting when you’ve been at the hospital for a while and haven’t slept. There’s no telling where your mind will go.

No matter how much you tell yourself not to do it, you can’t help but think of all that can go wrong.

During these moments, I can assure you that one thing you’re not thinking about is money. If anything, you’re thinking that you would trade all the money you have for a healthy baby and a healthy mom.

When you finally hold your new baby, nothing else in the world matters. Everything around you goes quiet. The sense of relief is overwhelming and you cry.

It’s a beautiful thing.

In those first few moments, I told my baby girl that I love her. I promised that I will always protect her. Whatever she needs, I will be there.

If I want to keep that promise, I need to be good with money.

To be good with money, I need a powerful Money Why.

I wrote down that goal before I was even married or had kids.

Years later, my Money Why hasn’t changed. The only thing that’s changed is my Money Why has gotten stronger and stronger since then.

In 2017, my Money Why got stronger when I got married.

Then in 2020, my Money Why got stronger when my daughter was born.

Again in 2022, my Money Why got stronger when my son was born.

This week, my Money Why got stronger when my baby girl was born.

My Money Why has never been more clear. It doesn’t even matter if my brain is functioning at half speed right now on limited sleep.

My Money Why is my baby girl, my son, and my daughter. My Money Why is my wife.

Of course, I want to provide for my family financially.

But my Money Why is more than that.

I don’t want to just provide money, I want to provide time. And, I want to be present and share experiences.

Most of all, I want to be with them.

My overall goal in life is to spend as much time as possible with the people who are meaningful to me. To accomplish that goal, I need to be good with money.

If I’m good with my money, I can achieve financial freedom.

With financial freedom, I can choose how to spend my time. That means I can choose who to spend my time with.

My Money Why is not about being rich.

Saying that I want to be good with money is not the same thing as saying that I want to be rich. Funny enough, people that are good with money oftentimes feel rich regardless of what their net worth is.

But I’ve noticed on my path to financial freedom there were several times when I felt incredibly rich and money wasn’t the dominant reason.

I couldn’t agree more with Dogen. There’s no richer feeling than having just come home from the hospital with a healthy baby girl. That feeling has nothing to do with money.

Check out more from Dogen at his website financialsamurai.com. There’s a reason why he is one of the leading voices in the personal finance space.

Simply making a lot of money will not make you feel rich.

On the flip side, people that make a lot of money but are not good with money often feel like they’re struggling to get by. As CNBC explained after talking with financial psychologists:

Whether you’re aiming to save more cash or boost your overall earnings, it’s important to ask yourself what you hope to achieve by obtaining more money, Chaffin says. Otherwise, if you don’t change your internal money beliefs, you may still feel anxious about money even if you hit millionaire status.

The takeaway is that it is pointless to make money without stopping to think why you want that money and what you’re going to do with it.

Money is nothing but a tool that you can manipulate to get what you truly want out of life. The thing is, you have to actually think about what you want if you are going to use that tool effectively.

Don’t wait for a major life event to start thinking about money.

You don’t have to wait until you have a baby to start thinking about what money can do for you. In fact, if you wait for a major life event like that, it’s going to be a lot harder than if you start thinking now.

Ask yourself:

“What is my Money Why?”

Whatever comes to mind, write it down.

Maybe you want to retire early. Maybe you’re just looking for a life pivot, as Scott Trench, CEO and President of BiggerPockets wrote about recently and has regularly discussed on the BiggerPockets Money podcast.

I personally agree with Trench, and I like almost everything about FIRE, which stands for Financially Independent Retire Early. It’s just that I know that retiring early is not for me.

I prefer to think of it as FIPE:

Financially Independent Pivot Early

With FIPE, the goal is not to retire. The goal is to give yourself the freedom to choose what to do next.

Whether you want to retire early or just pivot to a new chapter in your life, being good with money is key.

Besides, I’ve never seen the point in working endless hours to make money, while spending hardly any time seriously thinking about how to keep that money.

What’s your Money Why?

My Money Why gets clearer by the day. It has never been more clear than it is right now after bringing home a little baby girl.

What is your Money Why?

Has your Money Why changed over time?

How does your Money Why impact your relationship with money?

They’re a weight that we carry around long before we even make the first repayment. Sometimes that weight feels so heavy, it’s hard to imagine it ever going away.

And as much as we wish we could, we can’t ignore our student loans.

One way or the other, we have to get rid of them.

And when we do get rid of them for good, there might not be a better personal finance feeling in the world. Personally, I’ll never forget the day I made my last payment and shared the news with my future wife and family.

To help you have that same feeling of accomplishment, here are my top 10 student loan tips for lawyers and professionals.

Top 10 Student Loan Tips for Lawyers and Professionals

Locate all your loans.

Sign up for automatic payments.

Do not miss a payment.

Consider using Debt Snowball or Debt Avalanche.

Make an extra monthly payment.

Create a BAT that generates fuel for your student loans.

Make more money and use that money for your loans.

Take a tax deduction and use your tax refund for your loans.

Consider a loan consolidation.

Look for ongoing scholarship opportunities.

1. Locate all your loans.

As a first step, be sure that you are aware of all of your loans. Most people end up needing both federal loans and private loans, which are not tracked by the same loan servicers.

Additionally, you may have taken out different types of loans at different stages of your education. It’s not uncommon to forget about some of those loans.

Before you can implement a thoughtful strategy to pay back your loans, you need to ensure that all of your loans are accounted for.

The best place to locate all of your loans is on your credit report. The next best option is to ask your school’s financial aid office.

A credit report is a document that tracks your history of repayment and the current status of any loans you’ve taken out.

You are entitled to receive a free copy of your credit report from each of the three main credit reporting agencies every year. To do so, simply visit annualcreditreport.com.

For federal loans, you can also check online at studentaid.gov. But, your private loans won’t be tracked by the federal government at studentaid.gov.

Besides checking your credit report, you can access all your private loan information from your loan servicer.

Once you’ve identified all your loans, you can implement a strategy to pay them off efficiently.

2. Sign up for automatic payments.

By signing up for auto pay, you can save .25% interest on your federal loans. Many private loan companies also offer a .25% discount for using auto pay.

Over time, those savings will add up. And, there’s really no downside to you.

In fact, you should be using automatic payments even if your loan servicer does not offer a discount.

When it comes to paying back loans or achieving any other financial goal, automating your money is a very good idea. In The Automatic Millionaire, David Bach thoughtfully explains how the single step of automating your finances can help you achieve all of your financial goals.

You can learn more about Bach’s philosophy on his website.

I personally implement many of Bach’s strategies in my own life. I used to automate my student loans payments. Now, I automate my mortgage payments.

You know that expression, “Act now, apologize later”?

That absolutely does NOT apply to loan payments.

No matter how responsible or well-intentioned you are, sometimes life happens. Whether it’s technically your fault or not, a missed loan payment is a big problem.

It may seem unfair, but even a single missed payment can severely impact your credit history and credit score.

Because the consequences of a missed payment are so severe, this is another reason why setting up auto payments is such a good idea.

If you know ahead of time that you won’t be able to make a payment, it is imperative that you notify your loan servicer ahead of time. Your loan servicer may be able to work with you and figure out a solution before major consequences set in.

4. Consider using Debt Snowball or Debt Avalanche to pay off your student loans.

When you apply the Debt Snowball strategy, the idea is to focus on the loan with the smallest balance first, regardless of interest rate.

Once you have paid off the first loan in full, you move to the loan with the next smallest balance, again regardless of interest rate. The money you had been paying to the first loan can now be rolled into the second loan.

When you apply the Debt Avalanche strategy, the idea is to prioritize the loan with the highest interest rate, regardless of the balance.

Once you’ve paid off the loan with the highest interest rate, you move to the loan with the next highest interest rate. Just as before, the money you had been paying to the first loan can now be applied to the second loan.

Either approach works perfectly for paying off multiple student loan balances. Regardless of which method you choose, always pay the minimum required amount on all loans every month.

5. Make an extra monthly payment for massive savings.

You may be surprised how big of an impact even a small additional payment each month can have on your loans.

Let’s look at an example.

Let’s say you owe $100,000 in student loans and currently pay back $1,250 per month with an 8% interest rate.

Using calculator.net, you learn that at this pace, it will take you 9 years and 7 months to pay off your loans. You’ll pay back a total of $143,377.94.

Now, let’s imagine you are able to pay back an additional $100 per month.

Look what happens:

You can eliminate your loans an entire year sooner and save $5,040.13 in interest payments. Just with an extra $100 per month!

What about if you are able to pay back an extra $250 per month?

This is when I start to get excited.

Check this out:

For just $250 per month, you can knock off 2 years and 2 months of loan repayments and save $10,684.35 in interest!

Think about how good it will feel to get 2 years and 2 months of your life back without loan payments.

How are you supposed to come up with an extra $100, $250, or more per month?