As we fail to pay our balances in full each month, we fall deeper into debt, and credit card companies make massive profits.

This is why credit card companies hope you only pay the minimum owed on your balance each month. When you carry a balance, they make a ton of money.

If that doesn’t sit well with you, don’t complain about unfair the game is. When you sign up for a credit card, you agree to play by certain rules.

Instead of wasting your time and energy griping about high interest rates, figure out a plan to pay off your debt. Stop giving the credit card companies any more of your money.

What can you do to stop making money for the credit card companies?

Start by understanding exactly how credit card companies make money off of you. This is what we’re going to focus on today.

If nothing else, always remember that banks are “for profit” businesses, and they’re very good at making profits.

Then, you can implement these 10 tips to pay off debt as quickly and painlessly as possible.

Let’s get to it.

Understand how credit card interest works so you don’t end up paying it.

If you’re going to use credit cards as part of your everyday life, you should understand the basics on how interest is charged.

Unfortunately, failing to understand how credit card interest works is an all too common mistake.

Here’s what you need to know.

Credit card interest is typically expressed as an annual percentage rate, or APR.

If you carry a balance on your card, the credit card company charges interest by multiplying your average daily balance by your daily interest rate. You will be charged this interest until your balance is paid off in full.

Credit card interest rates are typically variable, meaning they can change over time.

In the abstract, it can be difficult to fully appreciate how penalizing credit card interest is on our finances.

Let’s look at an example to better understand the consequences of carrying a balance.

Let’s say you just moved to a new apartment and purchased a $1,400 TV using a credit card.

You don’t have enough money saved up for the full purchase, so you decide to pay off $100 each month. Your credit card charges 23% interest.

At that interest rate, it will take you 17 months to pay for that TV. You will end up paying a total of $1,645, which includes $245 in interest.

The $245 in interest equals 15% of the original price of the TV. That means you paid 15% more than the TV actually cost.

If that doesn’t catch your attention, don’t forget this is just the interest on one purchase after moving to a new apartment.

What if you want to buy a new sofa to go with your TV? How about a coffee table and a rug? Floor lamp? End table?

You can see how a 15% penalty on each of these purchases can start to add up quickly.

Think about this added cost the next time you make a purchase expecting to just pay it off slowly over time.

Never miss a credit card payment unless you like making banks richer.

Write this rule down in stone: never miss a credit card payment.

If you don’t remember any of the other credit card tips, remember this one.

It may seem unfair, but even a single missed payment can severely impact your credit history and credit score.

Because the consequences of a missed payment are so severe, it’s a good idea to set up your account for automatic payments.

You have options when setting up automatic payments. Ideally, you can pay your full balance automatically each month.

If that won’t work for your situation, you can set up automatic payments for the minimum required amount to stay in compliance with your account terms.

By paying at least the minimum amount required on-time each month, you will not be penalized with a missed payment.

What is the minimum required payment?

Credit card companies typically only require customers to make a minimum payment towards their balance each month.

By the way, the banks want you to only make the minimum payment each month. When you do that, they make a lot of money off of you.

They get richer while you fall deeper into debt.

The minimum payment is generally 2% to 4% of your balance, or a predetermined minimum fee of around $35.

It may sound enticing to only pay the minimum. However, you will be charged interest on that remaining balance. That interest compounds and will be a major drag on your finances.

Let’s look at another example to see what happens when you only make the minimum required payment.

Let’s say you have a credit card balance of $2,000. Your minimum required payment will likely be between $40 and $80 to stay in compliance with your account terms.

In this example, assume the minimum required payment is $40. If you make the minimum payment of $40 out of your total balance of $2,000, that means your remaining balance is $1,960.

On the next billing cycle, you will be charged interest on that remaining balance of $1,960. At 23% interest, you will be charged $37.39, which gets added to your total balance.

So, on the next billing cycle, your total balance will be $1,997.39.

Let that sink in.

Even though you paid $40 last month, your balance only decreased by $2.61. Ouch!

Note: this example is for illustration purposes only and may not be precisely how your credit card company calculates interest.

Know the fees associated with your account.

Beyond interest and hoping you only make the minimum payment, credit card companies profit by charging fees, such as late fees and balance transfer fees.

Let’s focus on just one of the many fees: the annual fees tied to rewards credit cards.

These fees can cost hundreds of dollars annually and cancel out the value of any points you earn.

For example, if you have a credit card that charges an annual fee of $500, and you only earn $400 worth of points each year, that’s a losing proposition.

You’d likely be better off using a credit card that does not charge an annual fee, even if that means losing out on some points.

For that reason, it’s important to do your homework before applying for a new card.

Be strategic about what, and how many, credit cards you have.

There was a time in my life when I had ten different credit cards because I wanted to maximize the points I earned on every purchase.

I had airline branded cards, hotel branded cards, and general travel rewards cards. I had credit cards with Chase, American Express, and CitiBank.

My wallet was so thick it was embarrassing.

I did earn a lot of points. But, it was so stressful.

Keeping track of what card to use for every single purchase was complicated. Making sure I paid off each card every month was even harder. In the end, it wasn’t worth it.

I now keep things simple with just two credit cards and recommend you do the same.

There’s no reason to overcomplicate it. I use the Sapphire Reserve for travel and dining and the Freedom Unlimited for everything else.

My wife and I still earn plenty of points and our finances are much simpler.

One other suggestion: if you’re in a relationship and share finances, I suggest you align your credit card strategies. Most major credit card companies allow you to combine points with a household member.

You can more quickly accumulate points by focusing on a single rewards program, instead of spreading out those points among various programs.

Unless you want the banks to get richer, don’t spend money just to earn points.

When you have rewards credit cards, the temptation exists to spend money you otherwise wouldn’t because you want to earn more points.

It’s possible to become so obsessed with collecting points that you forget about the strong personal finance habits you’ve worked so hard to establish.

It can be easier to justify careless spending when we trick ourselves into thinking that spending will eventually lead to a vacation.

For example, if you have a credit card that offers bonus points at restaurants, you may be tempted to spend more money when you eat out.

Or, you may be tempted to pick up the tab for your friends even though that spending doesn’t align with your budget.

The temptation to earn points can overwhelm your plans to stay on budget. This logic applies to any type of spending, not just dining out and bar tabs.

Use your credit cards to spend within your Budget After Thinking, not as an excuse to justify blowing your budget.

Otherwise, all you’re doing is helping the banks get richer.

Help yourself get rich, not the banks.

If anyone is going to get rich off of my efforts, I want it to be me, not the banks.

By understanding how credit card companies make money, I can plan my actions in a way where I benefit instead of them.

It starts with not overspending. From there, I need to make sure I pay my balance in full each and every month. Finally, I need to make sure I’m not spending just to earn more points.

Have you ever asked yourself what you would do with financial freedom?

I asked myself that powerful question on a beach years ago and came up with my Tiara Goals.

Debt is a major obstacle on the way to financial freedom. To help you stay motivated to eliminate debt, write down your version of Tiara Goals.

By reminding yourself what you’re actually striving for, you’re more likely to stay on track.

Whenever we talk about good money habits, it always starts with establishing strong motivations. This is especially true when it comes to debt. There are too many temptations that can push us off track.

When you’re faced with these inevitable temptations, take a look at your Tiara Goals. I keep my Tiara Goals in my notes section on my phone. I also have a picture on my phone of the original sheet of notebook paper I scribbled on.

All it takes is a quick glance at my most important life values to overcome whatever temptation is in front of me.

Getting out of debt is not easy. Make it easier by regularly reminding yourself what you would do with financial freedom.

If you’re currently in debt, it’s crucial that you stop that debt from getting larger.

Think about it. If you’re paying off $1,000 of credit card debt each month, but you’re still spending $1,200 more than you earn, your efforts will be for nothing.

Your debt is growing faster than you’re paying it off. You’re not getting any closer to being debt-free.

Once you’ve stopped the disappearing dollars and learned where your money is going each month, you can make thoughtful decisions to pay off debt on a budget.

Then, you can be confident that any money you allocate to debt will actually lower your debt balance.

3. Prioritize Later Money funds to pay off debt.

The art of budgeting is to generate fuel for your Later Money goals. The more fuel you can generate each month, the faster you will achieve your personal finance goals.

There are lots of options on what to do with your Later Money. For example, you can invest in real estate or the stock market.

When you’re in debt, I recommend you prioritize using your Later Money to eliminate that debt. This is especially true if you have Bad Debt, like credit card debt. Your number one money focus needs to be to eliminate that debt.

This is the key to learning how to pay off debt on a budget.

There’s a good reason to focus on paying off your Bad Debt.

The interest rate on Bad Debt is generally very high. The amount you pay in interest each month will be significantly greater than what you may reasonably expect to earn through investments.

If you only have Good Debt, like student loan debt, you have some more flexibility in whether to focus on that debt or your other investment goals.

This is because Good Debt generally carries lower interest rates, so your investment returns may match or even exceed what you’re paying in interest.

In this scenario, I suggest that you consider splitting your Later Money between debt pay down, savings, and investments. This is what my wife and I are currently doing in 2025.

Seeing your savings and investments grow while focusing on how to pay off debt on a budget can provide an emotional lift.

Establishing good savings and investment habits now will also have longterm benefits that should survive your debt phase.

Our Top 10 Strategies for staying on budget will help you generate more money to allocate to debt. These tips are crucial if you’re trying to learn how to pay off debt on a budget.

For example, when you see something that you might want to buy, make a note in your phone instead of buying it right away. After a couple weeks, you probably won’t even want that thing anymore. Take that money you didn’t spend and put it towards your debt.

As another example, how about playing The $500 Challenge Game? When you come in under budget that month, use the excess funds to pay down debt.

You’ll see for yourself that the emotional high of paying down debt is better than the feeling you’d get from spending that money on things you don’t care about. It’s important not to ignore these emotional wins when learning how to pay off debt on a budget.

5. Talk to your people about how to pay off debt on a budget.

Talking money is not taboo. That includes talking about our current money goals and money challenges. Of course, it includes talking about how to pay off debt on a budget.

What are your current money priorities? If you don’t want to share with us, are you sharing with your friends or family?

I struggled with debt when I began my career as a lawyer. For years, I kept that to myself. I wish I had been more open. I’ve recently learned that many of my friends were struggling in the same way.

The problem was that none of us talked about it.

I think about how much stress we could have saved each other if we were just willing to talk about money like we talked about everything else. Instead, we hid our truths from each other.

Even worse, we likely enabled each other’s poor spending habits.

I now know that it didn’t have to be that way. I would have been better off if I was open about it.

This part still bothers me today: I also might have helped my friends facing the same challenges just by starting the conversation.

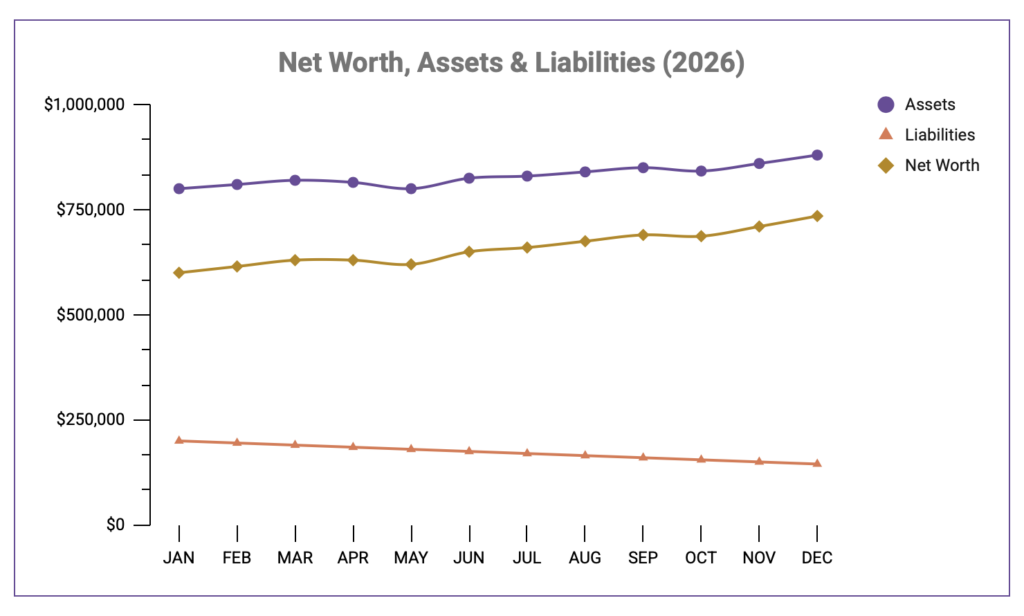

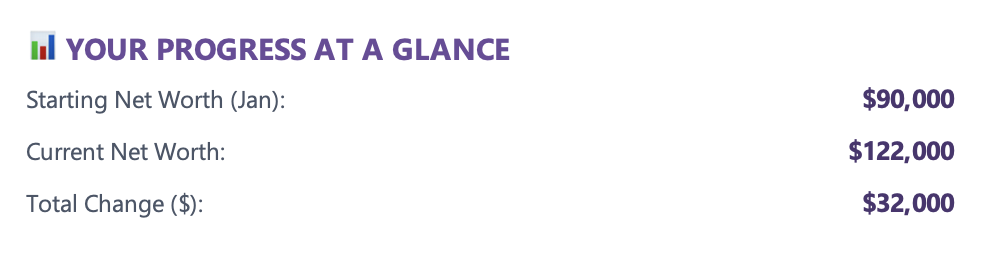

6. Track your net worth and savings rate for small wins.

Remember that your net worth grows when you reduce your liabilities, meaning debt.

When we think of net worth, it’s common to focus on growing our assets. Don’t forget that reducing your debts has the same impact on your balance sheet.

For example, when tracking your net worth, eliminating $1,000 in debt is the same as an investment that grows by $1,000.

Even when you’re focused on how to pay off debt on a budget, tracking your net worth can be very motivating. Every payment you make to reduce that debt improves your net worth.

This is especially helpful if you are focused on paying off student loans or paying down a mortgage. You may not have many appreciating assets, but you can still make a positive impact on your net worth by reducing your debt.

The same logic applies to tracking your saving rate. Measure and feel good about each additional amount you dedicate to eliminating debt.

The goal is to stay motivated while you pay off debt on a budget.

There are two common strategies to consider when you hope to pay off debt on a budget. These strategies are referred to as “Debt Snowball” and “Debt Avalanche.”

Debt Snowball means paying down your smallest debt balance first, regardless of interest rate. When you’ve paid off that loan completely, you then move to the next smallest balance, again regardless of interest rate.

Debt Snowball is ideal for people that are motivated by the emotional wins that come with eliminating a loan completely, even if it costs more money in interest in the long run.

Debt Avalanche means you pay down the debt that has the highest interest rate first, regardless of the balance. Once that debt is gone, you move to the loan with the next highest interest rate.

Debt Avalanche is for people who would prefer to pay less overall interest, even if it will take longer to pay off a single loan and receive the emotional win.

I discussed the pros and cons of each strategy here. Some people will prefer the emotional wins of the Debt Snowball method, while others will prefer the mathematical advantage of the Debt Avalanche method.

I’ve experienced firsthand that our money choices have more to do with emotions than they do math. If you prefer to play it strictly by the numbers, I completely understand.

The key is that whichever strategy you pick, stick with it. You’ll save yourself a lot of unnecessary mental gymnastics by choosing one approach and then moving on.

One word of caution: whichever method you choose, be sure to always pay the minimum on all of your loans. Otherwise, you’ll be in violation of your loan terms and face devastating penalties.

The idea with either of these methods is to allocate whatever funds remain to the single loan you have prioritized after paying the minimum on all loans first.

8. Think about loan consolidation or balance transfers.

Whether you have credit card debt, student loan debt, or even mortgage debt, you may have the option to consolidate each type of loan into a single loan.

If you do your homework, you should end up with a lower overall interest rate and have only one loan payment to make each month.

If you choose to go this route, make sure you fully understand the fine print involved.

For example, if you’re thinking about consolidating your student loans, you’ll end up sacrificing certain loan forgiveness provisions that accompany federal loans.

The same caveat applies when considering a credit card balance transfer.

A balance transfer is when you move the balance from one credit card to a different credit card with a lower interest rate. Most major credit cards accept balance transfers from other banks’ credit cards.

The main reason to consider a balance transfer is if the card you are transferring into carries a significantly lower interest rate than your current card.

In some instances, you may even qualify for a promotional rate with no interest charged for a limited period of time.

I used balance transfers when I was focused on eliminating credit card debt at the beginning of my career. I did my homework and found a card that was advertising 0% interest for 12 months with no balance transfer fees.

That meant that for an entire year, I paid no interest. Every payment I made went directly to lowering my overall debt.

If you’re considering a balance transfer, be mindful that there are usually upfront fees involved, usually around 3%. That fee may end up cancelling out any benefit from doing the transfer in the first place.

9. Get a side hustle to help pay off debt on a budget.

You’re not too busy or too important for a side hustle.

At the end of the day, there are really only two ways to more quickly pay off debt on a budget: spend less money and/or make more money.

We already talked about creating a Budget After Thinking to help on the spending side.

If you still believe that your income is the reason you have debt, there are always ways to improve your income.

Of course, if you really want to get rid of your debt faster, earning more money and the same time you’re spending less money is a dominate combination.

If you take on a side hustle, you can use every dollar you earn to pay off debt. Since this is new money you’re earning, you shouldn’t need it to fund your Now Money or Life Money.

Avoid the temptation of using that money on things you don’t really want anyways. Think about how much faster that debt will disappear if you’re able to throw additional money at it each month.

If you’re not ready for a side hustle, the same logic applies anytime you earn a bonus or commission at your primary job. Put that money to good use by paying down your debt.

10. Don’t let yourself fall backwards while you pay off debt on a budget.

When you do succeed in eliminating a debt, don’t let yourself fall back into bad habits. It’s hard to pay off a debt. It takes time. It takes patience and discipline.

Don’t let it all be for nothing.

When you pay off a loan, celebrate that accomplishment!

Be proud of yourself and let that good feeling motivate you to continue on your journey towards financial freedom.

Before you know it, debt will be part of your past life. You can shift all your attention to the opportunities that comes next for you and your family.

Top 10 Tips to Pay Off Debt for Lawyers and Professionals

To recap, here are my top 10 tips for lawyers and professionals to pay off debt:

If you have credit card debt, your immediate financial goal should be to pay off that debt as quickly and efficiently as possible. To get you started, I’ll show you exactly how to make a budget to pay off debt.

On your journey to financial freedom, getting rid of credit debt is crucial.

It is nearly impossible to get ahead financially if you are paying 20% interest or more on credit card debt. That type of drag on your money is just too strong.

Think about it: the stock market has historically averaged a 10% annual rate of return.

Does it make any sense to prioritize investing in the stock market to earn 10% per year if, at the same time, you are paying 20% in interest on your credit card debt?

Each year you follow this pattern, you are losing more and more money.

So, the first thing you should do is come up with a plan to pay off your credit card debt. Once the debt is gone, use that money for investments.

Today, we’ll look at how to make a budget to pay off debt so you can begin fueling your investments.

If you can follow these three steps, you’ll have a budgeting framework in place that will serve you well, long after you’re out of debt.

Paying off debt is the hard part. If you can do it, you’ll soon realize that it is a lot more fun to see your money grow each month instead of only seeing your debt shrink.

Let’s dive in.

Making a budget to pay off debt is about having a plan ahead of time.

The art of budgeting is to know what you want to do with your money before it hits your checking account.

Otherwise, it’s too late. Those dollars will disappear.

How do you come up with a plan, or budget, to pay off debt?

I teach my students that to create a budget to pay off debt, you need to first study your own personal situation to figure out where your dollars are currently going.

Then, you can figure out a plan for how to use your next dollar before you earn it. This applies not just to bonuses or other unexpected dollars, it applies to every dollar you earn.

When you put the time in to study your own habits, you can then create a realistic budget. When you have a realistic budget, you will have confidence that your dollars are working for you.

Some dollars will be used to pay your ordinary life expenses, some dollars will be used for all the things in life you love, and some dollars will go to your financial goals, like paying off debt.

That’s all there is to it.

If you don’t currently maintain a budget, here are three steps to follow to get you started.

Step 1: Track your spending for at least 3 months.

I recommend everyone, regardless of where you are in life, start with this first step of tracking your spending for at least three months.

Without knowing where your money is currently going, you won’t be able to make adjustments so you can pay off debt faster.

In other words, before you can reduce your debt, you have to make sure your debt is not growing each month.

That means not spending more than you can afford to pay off each month.

That’s a problem if you’re hoping to make a budget to pay off debt.

To address that problem, you need to track every penny for at least three months. Then, you’ll know exactly how much you’re spending and can begin to think about areas of improvement.

So, before you go any further in the budgeting process, you need to commit yourself to tracking every penny for three months and only charging what you can afford to pay off.

Fair warning, you probably won’t enjoy this part of the budgeting process.

Tracking your spending is important even if it’s not enjoyable.

I won’t lie to you.

This step can be hard and you probably won’t like it. This is the step that makes people think budgeting is a nasty word.

I get it and don’t blame you for having that reaction.

Still, there’s no getting around this first step. You don’t have to budget forever, just long enough to learn your own behaviors towards money.

Please know that many of us struggle with this first step. You might not like what you learn by tracking your spending.

When I first started budgeting, I learned that I was $20,000.00 in debt and was spending way more than I earned.

That wasn’t fun, but I’m happy that I put in the effort to find my blindspots and make adjustments.

I often think to myself, “Where would I be today if I didn’t go through this process 15 years ago? How much further into debt would I have fallen?”

The good news is, tracking your spending is easier today than it’s ever been. I’ve used apps, spreadsheets, and even the notes function on my phone.

Regardless of how you track your spending, be honest with yourself. If you intentionally or mistakenly leave out certain expenditures, you won’t learn where your money is actually going.

A budget, which is just a plan, is only as good as the data it’s built off of. Be honest about your data.

Last note: Budgets are usually done monthly, so you’ll want to create a separate accounting for each month you tracked.

The reason we track three months of spending is so you’ll be able to identify any patterns or inconsistencies in your spending from month-to-month.

This helps ensure you’re making decisions based off the best data possible.

Step 2: Separate your spending into three three main categories.

Great work completing the first step! That wasn’t easy, but you did it.

Now that you have tracked your spending for three months, you can assign each expense into separate categories.

Most personal finance experts agree, though we have different names for each category, that you should divide your money into three main buckets.

I refer to these buckets as:

Now Money

Life Money

Later Money

1. Now Money

Now Money is what you need to pay for basic life expenses.

These expenses include housing, transportation, groceries, utilities (like internet and electricity), household goods (like toilet paper), and insurance.

These are expenses that you can’t avoid and should be relatively fixed each month.

If you’re making a budget to pay off debt, it’s going to be hard to cut from this category, unless you are willing to make major changes. That means moving to a less expensive home or giving up your car, which are not always feasible.

That said, if you are in the position to make these kinds of big changes resulting in serious savings, you can accelerate your path towards being debt-free.

2. Life Money

Life Money is what you are going to spend every month on things and experiences in life that you love.

This bucket includes dining out, concerts, vacations, subscriptions, gifts, and anything else that brings you joy.

We can’t be afraid to spend this money. This bucket is usually what makes life fun and exciting.

The key is to think and talk so you are spending this money consistently on things that matter to you.

If you are truly dedicated to paying off debt, this is the major category to focus on. If it costs $100 to go out to eat, and $10 to eat dinner at home, that’s $90 that could potentially go towards paying off debt.

When you repeat that decision over and over, you can aggressively attack your debt.

3. Later Money

Later Money is what you are saving, investing, or using to pay off debt.

This bucket includes long term goals, such as retirement plan contributions (like a 401k or Roth IRA), college savings for your kids (like a 529 plan), emergency savings and paying off student loan or credit card debt.

This bucket also includes any shorter term goals, like saving for a wedding or a downpayment for a house.

Most fun of all, this bucket includes any investments you make to more quickly grow your wealth, like investing in real estate or the stock market.

You’ve probably guessed it already. Later Money is the key category that fuels your ultimate life goals, like financial independence.

The more you fuel this category, the faster you can reach your goals.

When your goal is to pay off credit card debt, any fuel you generate in this bucket should go to paying off that debt.

With the exception of contributing enough to receive your company’s 401(k) match and creating a small emergency savings account, all excess money should go towards paying off your credit card debt.

Don’t worry about assigning a percentage to each category.

I have intentionally not recommended target amounts or percentages to allocate to each of your three categories.

The reason is because of what I’ve learned from my students over the years. I’ll lay out my full reasoning in a separate post.

The short version is that in my experience working with law students, assigning target percentages for each category is counterproductive.

When I used to teach my students to aim for certain percentages in each category, I could tell that they would get discouraged as soon as I put the numbers on the slideshow. I completely understand why.

Each of us is starting in a different place. If you are currently spending 80% of your monthly income on Now Money, it’s not helpful to have someone tell you to create a budget that automatically drops that level to 50%.

My students would tune me out as soon as I put those numbers on the board.

Now, I teach my students to think and talk about their current personal realities and aim for steady and lasting improvements.

I want my students to create a plan that will last, not an unrealistic plan that they give up on after a few months.

So, whatever amount you’re currently spending in each bucket, that’s what we’re going to work with as we move on to step 3.

One other thing before you move on to step 3: don’t get hung up stressing about what type of expense goes into each category.

Sometimes, it gets tricky. Do clothes you buy for work count as Now Money or Life Money?

Don’t stress. It doesn’t really matter. It’s not worth the mental energy thinking about it. Just stay consistent and move on.

If you still want a target, aim for 20% of your income added to your Later Money each month.

All that said, I know that some of us operate better if we have a specific target in mind. If that’s you, the conventional wisdom is to aim for 20% of your income added to your Later Money each month.

Obviously, the more you add to Later Money, the faster you will pay off your debt. So, if you can afford more than 20% toward credit card debt each month, do it.

If you’re curious, targeting 20% savings each month was popularized in Elizabeth Warren’s book, All Your Worth: The Ultimate Lifetime Money Plan, first published in 2005 (before she was Senator Warren, she was a law professor and author).

Senator Warren advocated for a 50-30-20 budget framework with 50% going to fixed costs (what I call “Now Money”), 30% going to wants (“Life Money”), and 20% going to financial goals (“Later Money”).

Most personal finance experts agree that the 50-30-20 framework is a solid plan for your budget.

In theory, I agree.

In reality, I’ve become convinced through working with my law students that the 50-30-20 framework does not cut it in today’s environment.

While I agree the 60-30-10 framework may be more realistic, my experience has taught me that assigning rigid percentages is just not a practical framework for most people at the beginning of budgeting process.

Step 3: Make adjustments so your spending better aligns with your true motivations and desires in life.

OK, so now that you have assigned your spending to each of the three categories, the next step is to think and talk about your current habits and whether you’re spending matches your true motivations and desires in life.

If you decide that your spending does not match your life values, then it’s time to make some adjustments.

When you’re in credit card debt, the goal of these adjustments is to create more money each month to pay off your debt.

What kind of adjustments can you target?

In essence, my budgeting philosophy is to aim for steady and lasting improvements based on your current reality and your ultimate motivations.

What does that mean?

This is where we circle back to the importance of having a clear understanding of what we want out of our money. Money is just a tool.

Ask yourself:

“Is your current spending aligned with how you want to use your money to fuel your goals and ambitions?”

If not, you can make incremental adjustments as you progress towards your ideal spending alignment.

The idea will be to continuously add more fuel to your Later Money bucket so you can eliminate your debt faster.

You can make small adjustments, which are usually easier and faster to put in place. These adjustments might include dining out a bit less, cutting out a concert, or cancelling a gym membership or subscription you don’t use.

You can also make big adjustments, like moving to a cheaper part of town or getting rid of you car.

Small or big, the key is that when you make these adjustments, you repurpose that money in a thoughtful and intentional way. When you’re in debt, that means repurposing those savings to paying off debt.

Once your debt is paid off, you can put those savings towards your other financial goals.

You’ve already done the hard part. You’ve already aligned your budget with your money motivations.

With each thoughtful decision, you’re progressing towards your best money life. Most importantly, you’re learning about yourself and developing lasting habits. You won’t get discouraged and give up on budgeting.

To help you better understand how to make a budget to pay off debt, here is exactly how I did it when I was in debt in my twenties.

Here’s an example of how to make a budget to pay off debt.

In today’s budgeting example, we’ll look at how I made a budget to pay off debt in my twenties.

The dollar amounts below are what my actual income and spending looked like back then, adjusted for today’s dollars and rounded for easier math.

For some context, I was 26-years-old, living by myself in Chicago (no dependents, no pets), and working as a “slasher.” Not a joke, that was my actual job title.

I worked for a judge with the Appellate Court of Illinois, and as the junior member of the team, my responsibilities included lawyer duties and secretarial duties. I was a judicial law clerk “slash” secretary. Hence, slasher.

Lawyers are funny, huh?

In today’s dollars, I earned an annual salary of $90,000.00. That means I earned $7,500.00 per month. We did not have bonuses at the courthouse, so the $90,000.00 salary was my full compensation.

The benefit of going through an example like this is not to compare your situation to mine. Your income might be much higher or much lower. Same with your expenses.

Instead of the numbers, focus on the thought process so you can start to think about adjustments that suit your current life to help you pay off debt.

Below, you’ll see charts showing that I completed each of our three steps to make a budget to pay off debt:

Step 1: I tracked my spending for 3 months and reflected the average monthly amount for each expenditure in the column labeled “Baseline Budget.”

Step 2: I created a separate chart for each of the three main categories: Now Money, Life Money, and Later Money.

Step 3: I made thoughtful adjustments to better align my spending with my true motivations in life. I illustrated my decisions in the third column labeled “Budget After Thinking.”

Now Money

Recall that Now Money is what you need to pay for basic life expenses.

These are expenses that you can’t avoid and should be relatively fixed each month. If you have expenses for kids, pets, and other fixed life expenses, be sure to include them in your Now Money category.

Now Money

Baseline Budget

Budget After Thinking

Apartment rent

$2,200

$2,200

Renter’s Insurance

$20

$20

Parking spot

$430

$0

Gas for car

$40

$40

Car Insurance

$50

$30

Car Maintenance

$150

$150

Utilities

$120

$120

Internet

$60

$30

Cell Phone

$55

$35

Groceries

$300

$240

Personal upkeep(wardrobe, haircuts, etc.)

$100

$75

Gym Membership

$360

$360

Budget Busters

$300

$300

Now Money Total

$4,185

$3,600

What I learned tracking Now Money.

Now Money is pretty easy to track. There is not a whole lot of variance from month to month.

You’ll notice immediately that I had one major expenditure that needed immediate adjustment. That parking spot for $430? Definitely did not need that.

I lived 2 miles from work in one of the best cities for public transportation in the country. It was frustrating at times to look for street parking, but I didn’t use my car enough to justify the cost of a parking spot.

The other adjustments resulted in more minor savings, but don’t ignore these. Each adjustment took relatively no effort to make, just a little bit of thought beforehand.

When I say relatively no effort, I mean three phone calls and three reductions for car insurance, internet, and cell phone. That’s $70 saved per month, or $840 saved per year, for about 30 minutes of effort.

Otherwise, I decided to show a bit more restraint when grocery shopping and found a cheaper place to get my haircut.

All told, I reduced my Now Money Budget After Thinking by $585 per month with a little bit of thought and hardly any effort.

That meant $7,020 per year I could reallocate to paying off debt.

Life Money

This bucket, Life Money, is what you spend every month on things and experiences in life that you love.

Life Money

Baseline Budget

Budget After Thinking

Social Life (dining out, concerts, ball games, etc.)

$800

$700

Purchases (books, fun clothes, gifts, etc.)

$200

$150

Travel

$500/mo ($6,000/yr)

$400

Cubs Season Tickets

$400/mo ($4,800/yr)

$400

Budget Busters

$200

$200

Life Money Total

$2,100

$1,850

What I learned tracking Life Money.

When you’re reviewing your Life Money expenses, don’t be overly aggressive in cutting here. These are the things and experiences that make your life enjoyable. Even modest adjustments can make a big difference in the long run.

For tips on adjusting your Life Money without sacrificing the things and experiences you love, check out my post here.

As we saw with Now Money, with some thought and very little effort, I reduced my Life Money Budget After Thinking by $250 per month.

That meant another $3,000 I could use to pay off debt.

Some bonus tips for tracking Life Money

Life Money is the most annoying category to accurately track. These expenses vary month-to-month. You may buy concert tickets or have a trip planned some months, but not every month.

So, how do we get an accurate picture of our Life Money?

This is why I recommend you track your spending for at least three months.

You’ll get a more accurate picture because you can average your Life Money spending over those 3 months and balance out any inconsistencies.

Of course, if you have the patience to track your spending for even longer, you’ll get an even more accurate picture.

Fortunately, it is easier to track our spending today with the availability of apps and online banking platforms that can automatically track your spending.

Keep it simple when tracking your Life Money.

I highly recommend you keep it simple when tracking your Life Money. Many of my students give up on budgeting because they make this category more complicated than it needs to be.

I really struggled with this at first because I was so concerned about doing it right.

What I learned was that it doesn’t matter. If you go to happy hour with friends, don’t agonize over whether that goes into your “Dining Out” category or your “Drinks” category?

It doesn’t matter. Make it easy on yourself. Have one category called “Social Life” and move on.

Don’t forget that the point of budgeting is to learn your current habits so that you can make thoughtful adjustments.

Don’t let yourself become so obsessed with the details that you get stressed and give up on budgeting.

Break down large, annual expenses on a monthly basis.

One last tip, when you have large expenses, like season tickets or a big vacation, it’s helpful to break down those expenses on a monthly basis.

That way, you can see how much those individual purchases are impacting your overall monthly goals.

I’m not suggesting you actually pay for that trip over 12 months (like on a credit card), or that you can only spend that much on travel in a certain month. Think of it this way: you likely will not take a trip every month of the year.

Using my Budget After Thinking figures, let’s say I did not take a trip in January, February or March. That would mean that for my planned April trip, I would have $1,600 available that I can use, assuming I didn’t let those dollars disappear.

Later Money

Later Money is what you are saving, investing, or using to pay off debt.

This is the fuel for your most important goals.

When you’re in debt, this is the bucket that matters the most.

Later Money

Baseline Budget

Budget After Thinking

Student Loans

$1,100

$1,100

Credit Card Debt

$150

$900

Savings

$0

$50

Pretax Retirement (401k)

$300*

$300*

Other Investments

$0

$0

Total Later Money

$1,250

$2,050

*This was pretax money to my employer’s retirement plan. For budgeting purposes, it’s easier not to count the amount here.

This is where all your efforts in tracking your spending and making thoughtful adjustments starts to pay off, IF you have a plan for your next dollar before you earn it.

My plan was to pay off debt as quickly as possible.

In my baseline budget, I was very good about paying my student loan debt in full every month. I knew enough not to mess with student loans.

The consequence was my credit card bills were the last to get paid each month. This usually meant only paying the required minimum since I had run out of money by this point. It also meant no money for savings or investments.

In my Budget After Thinking, because of the thoughtful choices I made with my Now Money and Life Money, I created $800 of excess cash.

With that cash, I had committed myself to paying off my credit card debt as quickly as possible.

I also wanted to start the habit of saving each month. So, I added $750 of fuel to my credit card bills and $50 of fuel to my savings.

I stayed true to my plan and put that money to work. Within a few years, I had paid off all of my debt.

Some bonus tips for tracking Later Money.

Make budgeting as easy as possible for yourself.

In my example, I excluded the $300 pretax retirement savings because I am creating a plan for the $7,500.00 that hit my checking account each month. These are the dollars in jeopardy of disappearing.

The entire point of your budget is to create a plan for your next dollar before you earn it. You already wisely chose to save your pretax dollars by enrolling in your employer’s retirement plan.

Those dollars are already accounted for and working for you. They are not disappearing dollars. You did your job!

Like in my example above, you can exclude the amount you’re saving for retirement in pretax dollars from your budget calculations.

Feel good knowing that you’re saving that money. It’s icing on the cake. No need to worry about it when budgeting.

Now you know how to make a budget to pay off debt.

Let’s look at the complete picture before and after I started the budgeting process:

Baseline Budget

Budget After Thinking

Now Money

$4,185

$3,600

Life Money

$2,100

$1,850

Later Money

$1,250

$2,050

Total

$7,535*

$7,500

*Income of $7,500

With some thought and relatively little effort, I was able to stop the disappearing dollars and start making progress towards my ultimate life goals.

In my baseline budget, I was spending more than I earned each month. That meant I had no money to pay my credit card bills, which kept getting bigger because I kept spending.

In my Budget After Thinking, I broke my habit of living above my means and generated $9,600 of fuel in one year to help pay off debt faster.

Taking these first steps may seem like minor steps on the way to financial independence, but they were the most important steps I ever took on my personal financial journey.

Like I did, you can follow these three steps if you are truly motivated to make a budget to pay off debt:

Step 1: Track your spending for at least 3 months.

Step 2: Separate your spending into 3 main categories.

Step 3: Make adjustments so your spending better aligns with your true motivations and desires in life.

As you start to implement these steps, you’ll start to have a clearer picture of how your money can work for you.

When you’re in debt, that means putting your money to work for you to eliminate that debt.

The benefit to creating a Budget After Thinking is that it works whether you are in debt or you are focused on fueling other financial goals.

If you can put in the hard work now to create your budget, you’ll be in good shape no matter what you’re trying to accomplish.

Have you ever made a budget to pay off debt?

What was the key to successfully paying off that debt?

Looking at each of these explanations can help us understand and avoid common pitfalls that lead us into debt.

Of course, it’s expected that young lawyers will have student loan debt. While student loan debt may be considered good debt, the problem is that it can spiral into other forms of bad debt.

For example, student loan debt becomes the excuse for why we fall into consumer debt:

“I have to pay my loans this month, but I also want to eat out with my friends. I’ll just use my credit card.”

This is exactly what happened to me at the beginning of my career as a lawyer, and what I want to help you avoid.

If you fall into bad habits early, the problems only magnify when your income rises and your potential to spend rises.

The key is to eliminate the bad habits before they become bad habits. If it’s too late for that, now is the best time to correct those bad habits before the situation spirals.

Before we get to my theories why lawyers are in debt, realize that you’re not alone if you are a lawyer in debt.

Unfortunately, the data shows that debt is all too common in today’s world. Let’s begin with some scary stats about debt.

Here are some scary stats to help explain why lawyers are in debt.

According to the Federal Reserve Bank of New York, total household debt in the United States grew to $18.04 trillion by the end of 2024.

That’s such a big number, it’s hard to know what to do with that information.

Let’s break it down by the type of debt:

Credit card balances increased by $45 billion from the previous quarter and reached $1.21 trillion at the end of December 2024.

Auto loan balances increased by $11 billion to $1.66 trillion.

Mortgage balances also increased by $11 billion and reached $12.61 trillion.

HELOC balances increased by $9 billion to $396 billion.

Other balances, reflecting retail cards and other consumer loans, increased by $8 billion.

Student loan balances increased by $9 billion to reach $1.62 trillion.

While these numbers are still too big to comprehend, one powerful conclusion is hard to miss:

In every category, the amount of debt increased from the previous quarter.

This pattern of increasing consumer debt has been consistent for some time now.

HELOC balances have increased for eleven consecutive quarters.

Credit card balances have increased or remained the same for 10 of the last 11 quarters.

Let’s look closer at credit card debt for a moment.

According to a recent survey looking at credit card debt in 2024 by Bankrate.com:

48% of credit card holders carry a debt balance, an increaseof 9% since 2021.

53% of the people have been in credit card debt for more than a year.

The main causes of credit card debt are unexpected medical bills (15%), car repairs (9%) and home repairs (7%).

According to another Bankrate.com survey, 33% of Americans report they have more credit card debt than emergency savings.

These last couple stats help us understand why so many people fall into debt in the first place.

Some of it has to do with the failure to have emergency savings. When we don’t have savings, the first place we turn is to our credit cards.

Even more has to do with the failure to keep our spending in check, or living below our means.

Why is it so hard for lawyers to live below our means?

“Live below your means.”

“Money doesn’t grow on trees.”

“Don’t break the bank.”

We’ve all heard these common money phrases. If you were to ask someone older than you for one piece of personal finance advice, I’m betting you’ll hear one of these lessons.

Let me know if I’m right about that in the comments below.

There’s a reason these phrases are so common. They’re simple and easily reflect some of our core personal finance principles:

I didn’t have any idea how to budget or make intentional choices with my money. I had never thought about why or how to be good with money.

Like many people, I failed to create a budget and assumed that my W-2 income was plenty. I ignored emergency savings and never even thought about creating Parachute Money.

The saddest part is that I didn’t even realize that I was slipping backwards. I had no idea because I didn’t track my net worth or saving rate. I worked hard all year long and just hoped things would work out.

By the way, if this sounds familiar, you should know by now I’m not judging anyone. I’ve been very open about my money mistakes.

So, being careless with money is one common reason lawyers fall into debt. Another common reason is that bad things happen in life.

This might include medical emergencies, home repairs or car troubles. It’s not our fault that these things happen. But, it is our fault if we’re not prepared in advance.

While these events are unfortunate, and maybe even tragic, they are not unexpected. We all need to expect that bad things will happen.

Preparing for the unexpected is part of every solid organization’s planning.

In government, planning ahead means having a “rainy day fund.”

When managing properties, planning ahead for big repairs means having a “Capital Expenditures” or “Cap Ex” fund.

For our personal finances, planning ahead means having an emergency fund.

Whether it’s government, business, or personal finance, the goal is to have options other than taking on debt to get through challenging circumstances.

3. Blame the Kardashians.

Besides carelessness and emergencies, there’s another powerful force that contributes to rising debt levels across the world.

This force is nearly impossible to ignore. It’s become a part of our daily lives, whether we want to admit it or not.

What is this powerful force that contributes to our rising debt levels?

The era of social media and on-demand entertainment has made it harder than ever to avoid temptation. It’s everywhere we look.

Blaming the Kardashians realtes to another timeless, common money phrase: “Keeping up with the Joneses.”

The Kardashians are the modern day Joneses.

Once upon a time, “the Joneses” represented your neighbors, people you could observe from a distance on a regular basis.

The idea behind the phrase is that you can see what your neighbors are spending money on and are either consciously or subconsciously tempted to do the same.

If your neighbors buy a new car, you buy a new car to keep pace.

If your neighbors vacation in Australia, you research diving tours at The Great Barrier Reef.

When you notice your neighbors hosting a backyard BBQ party with lots of happy looking people, you decide to host a party the next weekend.

As humans, it can be difficult to ignore the temptation to keep up with our neighbors.

Whether we like it or not, we are concerned with our social status. Part of our self-worth gets tied to comparing ourselves to others.

Who better to measure up against than the people in our neighborhood who we probably have a lot in common with?

Keeping up with the Joneses is compounded in the professional setting.

This same idea is oftentimes compounded in the professional setting, like at law firms. It is not uncommon to compare ourselves in the same way to our colleagues at the office.

This is especially difficult for lawyers. Fair or not, society generally expects lawyers to make a lot of money and have nice things.

If a partner at your firm joins a country club, wears fancy clothes, or sends her kids to private school, you may feel pressured to do the same.

It’s easy to get caught up in expensive tastes when you’re expected to fit in, even if you don’t have the money to spare.

One of my favorite personal finance books, The Millionaire Next Door, discusses this concept in detail.

I highly recommend you read this book if you are struggling with comparing yourself to others.

Instead, the first part of the solution is to recognize when you’re making careless money decisions based on what you think other people are doing.

Making money decisions based off of your neighbors, let alone the Kardashians, is the fast road to debt.

You have no idea why or how another person is spending money. For all you know, it’s all for show and that person is barely getting by.

Do you really want to blindly follow this person’s choices? Wouldn’t it be better to confer with people you trust to help you think through money decisions?

The second part of the solution is to recognize that everywhere you look, companies are clamoring for your dollars.

Have you ever dreamed about owning a cute condo in a bustling city?

You know, the type of place where you can have your friends over and everyone gushes over how great your condo is?

If so, you’re not alone.

Many young professionals follow a traditional path in hopes of buying that cute condo as a “starter home.”

First, they spend a lot of money for an education to get a good job.

Then, after a few years of working that good job, they think about buying a starter home instead of continuing to rent.

These young professionals go into the home-buying process knowing that the home they may purchase will only be a temporary fit.

Even though it may be years down the road, they tell themselves they can simply upgrade if a significant other or children enter the picture.

For professionals living in cities, the search for a starter home typically leads them to condo buildings.

This makes sense. Condo buildings are attractive for a number of reasons.

I get the temptation to buy a cute condo.

Condo buildings are usually in locations ideal for young professionals.

Condo buildings oftentimes come with enticing amenities.

Plus, condo buildings typically offer one or two bedroom units, the perfect size for an individual.

Because of these features, condo buildings tend to attract other young professionals, making the building even more attractive.

While I never owned a condo in Chicago, I happily rented directly from owners in condo buildings for 10 years before buying my first rental property. So, I certainly appreciate the allure of living in a condo.

All this being said, I highly encourage you to think twice before buying a condo, or any other “starter home” for that matter.

That’s because owning a unit in a condo building comes with two significant downsides: (1) the actual cost and (2) the opportunity cost.

Instead, I recommend you think about these two alternatives to buying a starter condo:

Continue renting until you’re ready to buy a more permanent residence; or

Buy a small multifamily building where you can live in one unit and rent out the other units.

Before covering these two alternative ideas, let’s talk about the (1) actual costs of owning a condo and the (2) opportunity costs of owning a condo.

What are the actual costs of owning a condo?

The actual cost of owning a condo is like owning any other property, with one additional cost to be acutely aware of.

Besides the mortgage, insurance, taxes, and maintenance, condo buildings involve an additional cost that can be very expensive:

HOA Dues and Special Assessments.

Remember all those attractive amenities that drew you to the building in the first place?

Those amenities come with a price. Oftentimes, a substantial price.

On top of the HOA dues, be aware of unexpected special assessments, which can wreak havoc on your finances.

Special assessments may be needed to cover major maintenance or renovation projects in the building. When special assessments are due, you don’t have a choice but to pay up.

Ask any former condo owner why they no longer own a condo. My bet is most of them will blame the HOA dues and special assessments.

The other reason you’ll hear from former condo owners?

They outgrew their place.

This should not come as a surprise to any single person who buys a condo while also seeking a significant other.

You know how the saying goes: first comes love… then comes marriage… then the condo’s got to go.

That means additional money to prepare your condo for sale, for closing costs, and for moving expenses.

By the time you add up all these costs, you likely won’t walk away with any profit from owning a condo as a starter home because you only gave yourself a few years to benefit from appreciation.

Even if you do make a profit, it’s a gamble. Owning any home for a short period of time is not a good investment strategy. The transactional costs are simply too high.

Besides these actual costs, you should also consider the opportunity cost of owning a condo early in your career.

What is the opportunity cost of owning a condo?

While you may be OK with taking on the risk and these actual costs, don’t ignore the opportunity cost of owning a condo.

The opportunity cost refers to what you are losing out on by choosing to buy a condo.

In this context, the opportunity cost is that whatever you paid for the condo could have been used to invest in other assets. For example, instead of a down payment on a condo, you could have invested in stocks.

Or, you could have purchased a rental property that generates long-term wealth for you and your family (or future family). More on that below.

So, before you opt for the cute condo, think about both the actual costs and opportunity costs involved.

There’s nothing wrong with renting until you are ready to buy a more permanent home.

Owning real estate is a long-term proposition. The conventional wisdom is that you should not buy a property unless you plan to hold it for at least 7-10 years.

If you are not planning on staying in your starter home for at least that long, just keep renting. Invest your money elsewhere.

Save yourself the headaches of being a homeowner while building your net worth through an increased saving rate and other investments.

This is not groundbreaking information. This is Personal Finance 101.

Yet, many young professionals can’t resist the temptation to finally own a property after years of school and finally earning an income.

It’s up to you to set aside your ego, keep renting, and build a strong financial foundation.

By the way, many smart people think it’s financially foolish to buy a primary residence instead of renting.

And, I’m not just talking about buying a cute condo early in your career.

These really smart people think it’s almost always a better idea to rent instead of own in any circumstances.

While it’s beyond the scope of this post, you can find an in-depth analysis on the question of buying vs. renting in this video from Khan Academy.

I believe in the power of real estate as an asset class, especially small multifamily properties.

Instead of buying a condo for a starter home, consider these four reasons to invest in rental properties:

With cash flow, you can cover your immediate life expenses. For anybody hoping to reach financial freedom, it is essential to have income to pay for your present day life expenses.

For my money, cash flow from rental properties is the best way to pay for those immediate expenses.

If your present day expenses are already covered, you can use your cash flow to fund additional investments.

That might mean buying another rental property or investing in another asset class, like stocks.

Appreciation simply refers to the gradual increase in a property’s value over time.

While cash flow can provide for my immediate expenses, appreciation is all about the long-term benefits.

Like investing in stocks over the long run, real estate tends to go up in value. The key is to hold a property long enough to benefit from that appreciation.

To benefit from appreciation, all I really need to do is make my monthly mortgage payments, keep my property in decent condition, and let the market do the rest.

When I buy a rental property, I take out a mortgage and agree to pay the bank each month until that mortgage is paid off. At all times, I remain responsible for paying back that debt.

However, I do not pay that debt back with my own money.

Instead, I rent out the property to tenants. I do my best to provide my tenants with a nice place to live in exchange for monthly rent payments.

I then use those rent payments to pay back the loan.

As my loan balance shrinks, my equity in the property increases. Equity is just another way of saying ownership interest.

When my equity in a property increases, my net worth increases.

When you earn rental income, you must report this income on your tax return. Rental income is treated the same as ordinary income.

However, the major difference between rental income and W-2 income is that there are a number of completely legal ways to deduct certain expenses from your rental income.

Common rental property expenses may include mortgage interest, property tax, operating expenses, depreciation, and repairs. We’ll touch on a few of these deductions below.

With all of these available deductions, the end result is that most savvy real estate investors pay little, or nothing, in taxes on their rental income each year.

Yes, you read that right.

I’ll say it again, just to be clear:

Most savvy real estate investors legally pay nothing in taxes on their rental income each year.

I highly recommend you consider house hacking if you’d like to start investing in real estate.

When you buy a small multifamily property, you can live in one of the units and rent out the others.

If you pick the right property, you can end of living for free because your tenants pay your mortgagee.

The strategy of living in a building you own while tenants pay for it has been around for ages. Brandon Turner popularized the name “House Hacking” for this timeless concept.

You can read all about house hacking on BiggerPockets here.

My wife and I house hacked for years before buying our forever home.

Without a doubt, there is no better strategy for entry level real estate investors than house hacking. We talked about the financial upside earlier in this post.

Besides the financial upside, it’s like landlording with training wheels. Since you live on site, you can more easily learn how to manage a rental property, including responding to tenants and handling routine maintenance.

The naysayers will say something like, “I don’t want to live with my tenants. They’re going to stress me out. I don’t want to be bothered at 2 a.m.”

Ignore them.

My wife and I lived with our tenants for five years at our first property and two more years at a subsequent property. We did this while working full-time jobs as lawyers and raising two kids (now three kids).

Because we didn’t listen to the naysayers, we now have four income-generating properties and our “forever home” just outside Chicago.

Even though we’re no longer living for free, the income from our rental properties is enough to cover the expenses of our home.

Before buying that cute condo, think about house hacking instead.

There’s no better time to house hack than at the beginning of your career. This one decision can pay massive dividends for years to come.

No, your friends might not gush over your cute condo.

But, you’ll be well on your way to generating long-term wealth for you and your family.

Even if you’re not just starting out in your career, house hacking is still an incredible wealth-building strategy.

My wife and I house-hacked until I was nearly 40 years-old with two kids. We wouldn’t be where we are today if we instead opted for a cute condo.

Did you buy a starter home in your 20s or 30s? Any regrets?

Let’s say you are fresh out of law school working in big law.

At the current salary scale, that means you’re making $225,000 in salary, plus another $25,000 or so in bonuses. We’ll call it $250,000 in total compensation.

That’s a lot of money.

It’s so much money, in fact, that you convince yourself you can make some lifestyle changes.

For starters, you figure it’s time to leave the old law school roommates behind and move into a nicer, but smaller apartment by yourself.

Even though the tradeoff for living by yourself is paying more in rent, you justify it because your income is so high.

Besides paying more in rent, you can’t help but order in more meals now that you’re earning a high income. Plus, you’re working long hours, afterall. Who has time to cook?

Even though you survived on frozen chicken breasts in law school, that won’t cut it anymore now that you’re a practicing attorney.

Finally, you start taking Ubers to get around town. It’s only $15 per ride, and you make more than $20,000 per month.

Even though you took the bus or the “L” home in law school, you can afford a ride! Uber it is!

Does this sound familiar to you?

Maybe it sounds completely ridiculous?

Personally, this story is all too familiar.

When I graduated law school, I spent money based on my income instead of my wealth.

As soon as I started making money after law school, I started spending on things I really didn’t need.

About a year after I graduated, I moved into an apartment by myself. I started spending more freely. I took taxis (no Ubers back then) when I could easily have hopped on the bus or walked.

What made it worse in my case was that I was not even making big law money. At the time, I was a judicial law clerk making around $70,000 per year.

It was because I was careless with my money that I fell into credit card debt so quickly after beginning my career as an attorney.

On top of my poor spending choices, I had student loan debt. Because I had debt and hardly any assets to my name, my net worth was less than zero dollars.

That means I had negative wealth, even though I was earning a decent income.

This is all background for the main question behind today’s post:

Do you spend money based on your income or based on your wealth?

Let’s revisit our fresh big law attorney who’s earning $250,000 per year.

Earlier, I said “That’s a lot of money.”

And, it is.

But, what I should have said was, “That’s a lot of income.”

See, earning a lot of money is not the same as having a lot of money.

There’s a key difference.

Income is temporary. There’s no guarantee that your income will always be there. People lose their jobs all the time. People also switch careers, which can result in lower income.

Wealth is your financial foundation. When you have money, meaning you don’t spend it, you can build wealth.

Of course, when we talk about wealth, we are talking about all of your assets minus your liabilities. This is your net worth.

When your liabilities are greater than your assets, you have a negative net worth, like I did when I graduated law school. By the way, the same is true for most people when they graduate law school.

A high income is not a bad thing, but it can be a wasted thing.

A high income means you have a lot of money coming in.

That’s not a bad thing, but it can be a wasted thing.

What you do with that money is what determines your wealth and financial progress.

If you use your high income to acquire assets, you are winning the game. The same goes for paying off your liabilities.

If you use your high income to buy expensive things, you’ll be stuck in place. At the end of the year, you’ll likely be in no better shape than someone making a fraction of what you make.

That’s why I prefer to think about how much money I keep each year, instead of how much I make.

You may think that a new lawyer earning $250,000 per year should be splurging on life’s finer things.

Would your opinion change if you acknowledged that lawyer’s net worth is a negative number?

Think about it: most new lawyers leave law school with hundreds of thousands of dollars in debt. They also have little to no assets. That means they have a negative net worth.

Should someone with a negative net worth really be splurging on a fancy apartment?

If that person is looking to build a solid financial foundation, the answer is obviously, “No.”

This person should continue living like a law student and spending in accordance with his net worth, not his income.

I recommend you use your high income to acquire assets and eliminate liabilities.

Don’t get me wrong. I am not suggesting that earning a lot of money is a bad thing.

Having a high income is a major benefit.

In fact, I recommend that all of my law students take the high paying job right out of school, if they can get it.

A high income means you can pay off your debt faster. It means you can build up your emergency savings and fund your investment accounts sooner.

There can be no doubt that a high income can accelerate your progress to financial freedom.

You just need to use that income to acquire assets and eliminate liabilities.

As you take those steps, you’ll see your net worth climb, and you’ve earned the right to start spending more.

We all know that it’s bad to live beyond our means. The problem is we don’t evaluate our means properly.

You don’t have to be a personal finance expert to know that living beyond your means is a bad idea.

Most of us intuitively understand that we should live within our means. Actually doing so can prove to be more problematic.

Part of the explanation may be that we don’t think of our spending in terms of our net worth.

We may not appreciate that if we are spending extravagantly while our net worth is still low, or even negative, we are living beyond our means. It doesn’t matter what our income level is.

That’s why I recommend you spend based on your level of wealth (your net worth) instead of your income.

Of course, this lesson applies to all of us, not just recent graduates.

This is challenging for lawyers and professionals who feel compelled to keep up with the Joneses.

When you’re making $750,000 per year, you may think you need to buy the $100,000 luxury car. Or, you may not hesitate to spend $10,000 to upgrade your family’s plane tickets to first class.

But, can you really justify that level of spending when your net worth does not match up with your income?

What happens if that income goes away?

Instead, you should prioritize saving and investing until your net worth justifies that higher spending threshold.

Spending money based on your wealth does not spending from your wealth.

When I say spend money based on your wealth, I don’t mean that you should spend from your wealth.

In other words, this is not a post on spending down your wealth in retirement.

Rather, what I mean is that you should consider your net worth before deciding how much of your income you are comfortable spending.

For example, if you earn $250,000 per year from your job and have a negative or low net worth, you should continue living like a law student.

If you earn $250,000 per year and have a net worth of $1M, you would be justified in splurging from time-to-time.

If you earn $250,000 per year and have a net worth of $10M, you shouldn’t worry about spending extravagantly with all of that income.

Why not worry about spending so much?

The reality is that your investment earnings on $10M will far exceed your $250,000 income from work.

Even a 5% investment return on $10M would earn $500,000 per year, double what you earn from your job. You actually might start thinking about why you still have that job in the first place.

These numbers are just for illustration purposes. Still, the idea is that your spending decisions should factor in your net worth at least as much, if not more so, than your income.

Don’t ignore your wealth when it comes to spending.

Whenever you are evaluating your current financial position, especially your spending decisions, I recommend that you focus on your wealth at least as much as your income.

Income is temporary. It can go away at any moment.

If you are fortunate enough to earn a high income, use that high income to acquire assets and pay down liabilities. That means you’ll have to avoid spending extravagantly until your level of wealth can justify it.

Wealth is foundational. Yes, there will be drops in the markets and your net worth can decrease. That is to be expected.

However, if you focus on spending in line with your net worth, you’ll naturally adjust your spending if your net worth temporarily drops. When it rises again, you can justify spending more. The key is to be flexible.

If you can think in these terms, you will build a strong financial foundation that will give you choices down the road.

Making headlines this week, the federal government shut down, resulting in hundreds of thousands of federal employees being furloughed.

When someone is furloughed, he doesn’t receive a paycheck. Even if that person eventually receives backpay, furloughs can be a huge problem for those individuals.

Why?

Because most people, even high-earners, live paycheck to paycheck.

When you’re furloughed, money stops coming in. But, money keeps flowing out.

But even federal workers who eventually receive back pay can suffer during a shutdown, as many of them live paycheck to paycheck, [Dan Koh, former chief of staff of the Labor Department] added.

“Even if you are entitled to back pay, a lot of people can’t go even a couple of days without their regularly scheduled paycheck,” he told CBS News. “If you have to pay your subway fare, for gas, if something breaks in your home, and you’re not getting paid, it places extreme stress on government employees,” he said.

So, what can we do to help protect ourselves from furloughs or any other sudden loss of income?

The first savings account you need is commonly referred to as an emergency savings account. This is your ultimate security blanket for whatever life throws at you.

For example, if you are furloughed and lose your source of income, your emergency savings will keep you afloat until you’re working again.

The idea is to use your savings so you don’t have to pull from your long-term investments.

Your emergency savings is not just for when you get furloughed or lose your job. Your emergency savings will also protect you in times of emergency (brilliant, huh?), like unexpected medical bills or expensive home repairs.

The idea remains the same: instead of pulling from your investments, you will have cash available in your savings account to cover your needs.

Aim for 3-6 months of Now Money saved for emergencies.

Aim for building up 3-6 months of your Now Money saved in a dedicated emergency savings account.

In your Budget After Thinking, Now Money represents the consistent, reoccurring expenses that you need to pay every month to take care of yourself and your family.

Since you will only be using this money in times of emergency, you can, and should, forego some of life’s luxuries until you get back on track.

The same is true for fueling your Later Money goals. Take a pause until you sort out whatever it was that caused you to spend your emergency savings in the first place.

While your emergency savings account is your first line of defense when you are furloughed, I prefer having an extra layer of protection.