The holiday season is upon us.

As W-2 employees, now is the time to strategize what we can do before January 1 to optimize our taxes.

Let’s be honest: throughout the year, most W-2 employees don’t think very much about their taxes.

As a side, that’s one of the major differences between W-2 employees and business owners or real estate investors. If you own a business or own rental properties, you are always thinking about ways to lower your taxable income. More on that below.

OK, getting back to W-2 employees:

When was the last time you took a look at your actual pay statement?

Most of us working W-2 jobs have direct deposit, meaning our paychecks are automatically deposited into our bank accounts. On pay day, all we have to do is wake up, open our banking app, and confirm we got paid.

When we do this, all we see is our net pay, or take-home pay. Our net pay is what we earn after all deductions are subtracted from our gross pay.

Deductions reduce our taxable income and may include voluntary contributions to our 401(k) and HSA.

That’s all nice so far.

Not so nice is that our paychecks are further reduced by mandatory tax withholdings.

For high earning lawyers and professionals, taxes can easily reduce our W-2 income by 25%-40%.

The question as year-end approaches is: can we take any steps now as W-2 employees to reduce our taxable income?

The short answer is: yes, but the options are limited.

Let’s dive in.

Do you expect to take the standard deduction or itemized deductions?

Before we look at the options to reduce your taxable income, the first question is whether you plan to take the standard deduction or itemized deduction.

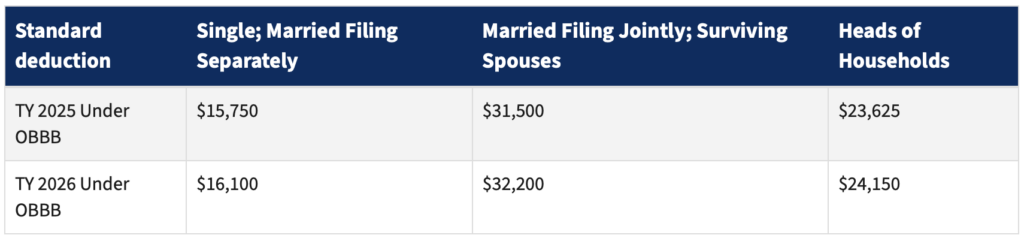

The standard deduction is an amount set by the IRS that reduces your taxable income and likely your tax bill. Here are the standard deductions for tax year 2025 and 2026:

How does the standard deduction reduce your taxable income?

Let’s say you are single and made $100,000 in 2025. If you take the standard deduction, you can reduce your income to $84,250. That means you only owe taxes on $84,250 instead of $100,000.

Assuming you elected typical tax withholdings from your paycheck throughout the year, you should get a tax refund upon filing your tax return.

Besides the standard deduction, the other option to reduce your taxble income is to itemize your deductions.

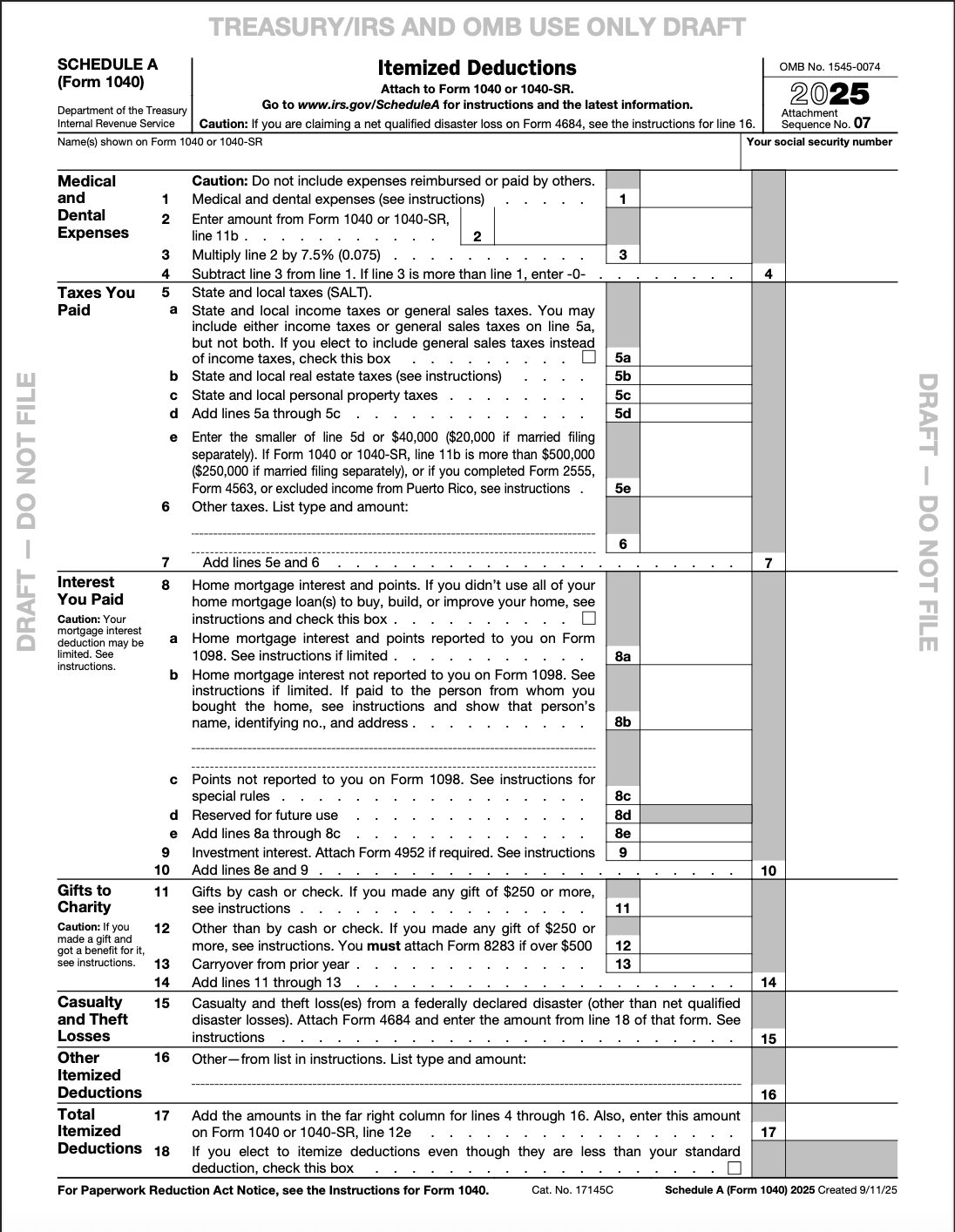

When you choose to itemize, the IRS allows you to claim deductions for expenses like mortgage interest, state and local taxes you paid, and gifts to charity.

Here’s a draft of Schedule A (Form 1040) which shows the common deductions if you itemize:

Importantly, if you take the standard deduction, you cannot also itemize your deductions. It’s one or the other.

So, before you start thinking about ways to lower your taxable income, you first need to decide if you’ll save more money by itemizing.

Generally speaking, most W-2 employees take the standard deduction. It’s the easiest way to file your taxes and provides the biggest refund for most typical W-2 employees.

On the other hand, if you have a mortgage, pay a good amount in state and local taxes, and/or make sizable charitable contributions, you may benefit from itemizing.

Donate to charity before the year ends to increase your itemized deduction.

Let’s say you and your tax professional decide you would benefit from itemizing. Maybe you reached that conclusion because the amount you pay in mortgage interest plus state and local taxes already surpasses the standard deduction.

If that’s the case, you may be wondering if there is anything you can do to further reduce your taxable income this year.

As you can see on Schedule A, the options for reducing your taxable income as a W-2 employee are limited.

You cannot control what you’ll pay in mortgage interest (that’s already determined). The same goes for your state and local taxes.

As a high earning attorney or professional covered by health insurance, it’s unlikely you’ll qualify for the medical expenses deduction.

The bottom line is that the only realistic option to reduce your taxable income as a W-2 employee is to make additional charitable contributions.

That leads us to today’s year-end tip.

Consider making additional charitable donations in 2025 if you want to reduce your taxable income.

This doesn’t mean that you have to donate more money that you previously budgeted for. You can simply accelerate the timing of when you make those contributions so you receive tax benefits this year.

For example, let’s say you budgeted for and typically donate $100 per month to your favorite charity. If you wanted to reduce your taxable income for 2025, you could instead make a lump sum contribution for $1,200 before the year ends.

The benefit is that you can claim a larger tax deduction for 2025 and get some of that money back as part of your tax refund. How much you get back depends on a variety of factors, most notably your tax bracket.

At the same time, your favorite charity benefits from your full donation sooner.

It’s a win-win for you and the charity.

As employees, we are accustomed to having significant taxes withheld from our paychecks.

As a W-2 employee, if you were hoping for more ways to reduce your taxable income… don’t look at me.

The tax code favors business owners and real estate investors.

We’ve become so accustomed to paying taxes as W-2 employees that none of this should surprise us. Taxes are just part of the bargain when you’re an employee.

In contrast, owning rental real estate comes with massive tax benefits.

I earn income through W-2 employment and rental properties.

As a W-2 employee and a real estate investor, I know firsthand that not all income is created equal.

My W-2 income is heavily taxed every month. I have very few ways to reduce my taxable income, like we just saw above.

On the other hand, I have a number of completely legal ways to reduce my rental property income.

Real estate investors benefit from massive tax benefits.

The federal government has long encouraged investment in real estate. People need places to live, work, and socialize.

The government long ago decided to reward investors who take on the risk of providing these opportunities.

These incentives come largely in the form of tax benefits.

To accomplish its goal, the government allows real estate investors to deduct certain rental property expenses from their income.

When you earn rental income, you must report this income on your tax return. Rental income is treated the same as ordinary income.

However, the major difference between rental income and W-2 income is that there are a number of completely legal ways to deduct certain expenses from your rental income.

Common rental property expenses may include mortgage interest, property tax, operating expenses, depreciation, and repairs. We’ll touch on a few of these deductions below.

With all of these available deductions, the end result is that most savvy real estate investors pay little, or nothing, in taxes on their rental income each year.

Yes, you read that right.

I’ll say it again, just to be clear:

Most savvy real estate investors legally pay nothing in taxes on their rental income each year.

Would you rather have rental income or W-2 income?

This post is not meant to be a primer on income taxes, but we can use a very basic tax bracket calculator to highlight the distinction between rental income and W-2 income.

I currently receive both types of income so readily appreciate the difference in how each form of income is taxed.

Let’s say you live in Illinois and are a high-earning lawyer or professional making a gross annual income of $250,000. Based on 2024’s federal tax rates, you will owe $53,015 in federal income tax. That’s 21% of your income.

Illinois is one of the 42 states that also levies a state income tax. Illinois levies a flat state income tax of 4.95%. For our example, that means an additional $12,375 in taxes each year.

In total, a W-2 employee earning $250,000 in Illinois pays $65,390, or nearly 26%, in income taxes each year.

Again, this is not meant to be a tax primer. And yes, most W-2 employees take the standard deduction, meaning they’ll get a small refund when they file their tax returns.

Still, there’s no getting around the reality that when you’re a W-2 employee, you have limited options to reduce your taxable income.

In the end, you will pay a significant percentage of your income to the government every year.

Real estate investors have a number of legal tax deductions at their deposal.

On the other hand, a real estate investor earning $250,000 in rental income likely pays very little, or even nothing, in income taxes.

How is that possible?

We already mentioned that the government allows real estate investors to deduct rental expenses.

For today’s purposes, I’ll highlight one key deduction that shows just how much the government wants to encourage real estate investment:

Depreciation.

What is Depreciation?

Depreciation is an accounting method that allows real estate investors to deduct some of the cost of owning a property over time.

This accounting process is not a trick and is completely legal.

Calculating your property’s depreciation can get complicated and is best left to the tax professionals.

In general terms, if you own residential rental property and use standard depreciation like me, you can deduct the cost of owning that property over 27.5 years.

Each year, you can then reduce your rental income by that annual depreciation.

Here’s an example to help illustrate how depreciation works.

Let’s say you buy a rental property for $500,000, and the closing costs are $10,000. The property’s in excellent shape so no capital improvements are needed.

That means your total initial cost for this rental property is $510,000.

When you buy a rental property, you are actually buying the land and the building. Your city, county or town’s assessor typically attaches a value to each the land and the building.

For depreciation purposes, only the value of the building is depreciable. The land is not.

In our example, let’s say the land was valued at $110,000. You are not allowed to depreciate the value of the land.

So, your depreciable basis is the initial cost of the property less the land value:

Initial Cost – Land Value = Depreciable Basis

$510,000-$110,000=$400,000

For residential rental properties, you can spread out that depreciable basis over 27.5 years to figure out the annual depreciation.

Depreciable Basis / 27.5 = Annual Depreciation

$400,000 / 27.5 =$14,545.45

What this means is that you can deduct $14,545.45 from your rental income each year.

Combined with the other available deductions, you can see why real estate investors end up paying very little, or nothing at all, in rental income taxes each year.

Note: If you sell your rental property, you are responsible for paying depreciation recapture tax, which is a topic for another day. To keep it simple, depreciation recapture is a non-factor for this conversation for many reasons. The most important reason for that is because you have to pay this tax even if you never claimed depreciation on your tax return.

Don’t forget to make your charitable gifts if you itemize your taxes.

I firmly believe every lawyer should only at least one rental property to accelerate his path to financial independence.

If you’re not a real estate investor, you may want to consider this conversation on taxes as you plan your financial goals for 2026.

Maybe a rental property is in your future.

For now, if you are a W-2 employee, consider making additional charitable donations in 2025 if you want to reduce your taxable income.

Charitable gifts may just be the only way to reduce the amount you pay in taxes this year.

Do you take the standard deduction or itemize?

If you itemize, do you know of other ways for a typical W-2 employee to reduce his taxable income?

Let us know in the comments below.

Leave a Reply