Let’s say you receive a year-end bonus of $10,000.

You essentially have four choices for what do with that money:

- Choice 1: Do nothing.

- Choice 2: Spend it now.

- Choice 3: Invest it for retirement.

- Choice 4: Pay down student loan debt.

Let’s explore each option using two Think and Talk Money calculators to help with our decision: (1) Compound Interest Calculator and (2) Student Loan Calculator.

You may be surprised by the results.

Choice 1: Do nothing.

You may not have a plan for what to do with $10,000. When you don’t have a plan, the default is to let the money sit in your checking account until you need it.

This is a bad idea.

Those dollars will disappear faster than you think. I don’t need a calculator to tell me that.

The worst part is you won’t have anything to show for it. You’ll just wake up one day in the near future and wonder what happened to your bonus.

Whatever you want to do with your money, put some thought into it ahead of time. Come up with a plan.

In the end, being good with money is nothing more than consistently making thoughtful, intentional choices.

Choice 2: Spend it now.

I don’t hate the idea of spending some of your hard-earned money. If you’ve thought about it and are making intentional decisions, go for it.

Maybe you’ve had your eyes on a new sofa, a bigger TV, or a trip to Scottsdale.

When you spend on things or experiences that bring you joy, that’s a good use of your money.

We talk about it all the time: being good with money is not about a life of deprivation.

If this is the direction you’re leaning, what if you chose to spend some of the money and then save/invest/pay down debt with the rest?

That way, you get some immediate satisfaction and also stay on track to reach your long-term financial goals.

In this instance, I would recommend spending no more than half of the money and then using the rest for your financial goals.

What should you do if you’re pursuing multiple long-term financial goals?

When you have multiple long-term financial goals, such as investing for retirement and paying off debt, the question becomes: which goal is a better use of your money?

This is a common conundrum for many of us.

The answer will oftentimes combine math and emotions. That’s what makes personal finance so fascinating. That’s what makes life so fascinating.

Based on my own experiences and in teaching personal finance to law students, I’ve found that financial calculators can be a very useful tool in making these decisions.

I’ve also found that financial calculators can motivate people to take action in ways that words alone usually fail.

I could tell you all about the magic of compound interest. That might be enough for you to take action.

Even more powerful is when you see the potential results of your money decisions for yourself. That’s where a good financial calculator comes in.

With that in mind, let’s use a couple of Think and Talk Money calculators to explore what would happen if you invested the $10,000 or used the money to pay down debt.

Seeing these results may motivate you to put your money to work for you, rather than spending it.

Choice 3: Invest it for retirement.

For this example, let’s say you are 27 years-old, which means you have 40 years until you reach the standard retirement age of 67.

We’ll also assume that you earn an average annual return of 10%, consistent with the historical average returns of the S&P 500.

We’ll also plan for an interest rate variance range of 2%, which means you will see your potential returns at 8%, 10% and 12%.

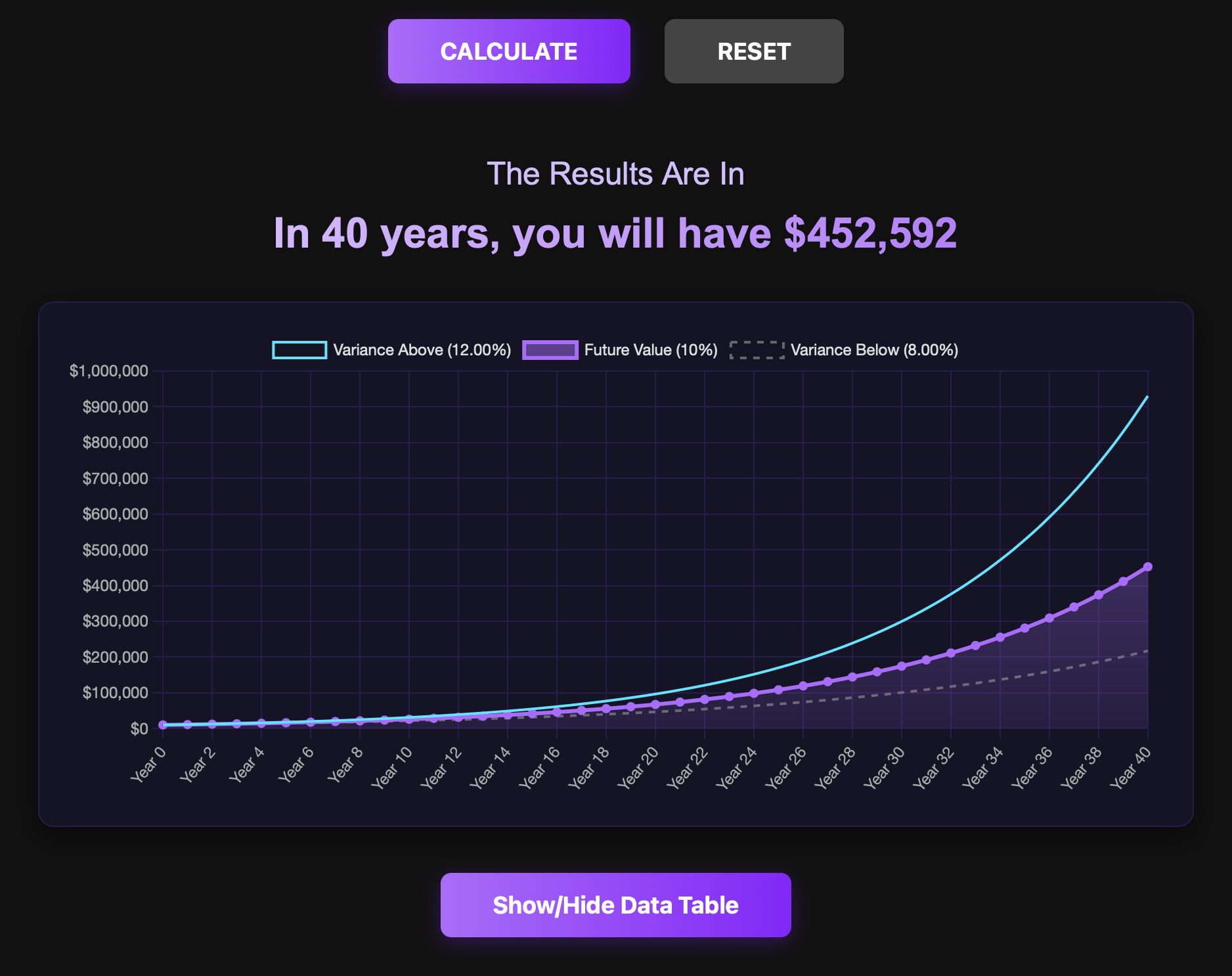

Here’s what it looks like when you plug those assumptions into the Think and Talk Money Compound Interest Calculator:

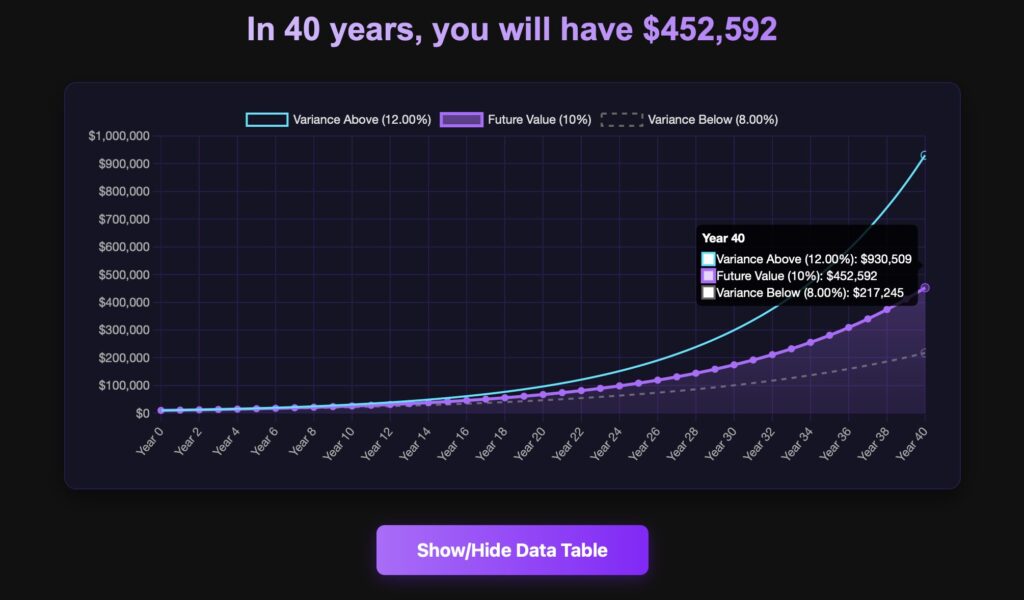

Now, here’s what your results look like:

After 40 years, you would have $452,592 at a 10% interest rate. Remember, that’s your total balance without ever making another contribution.

You can also see that you would have $217,245 if you earned an 8% annual return. Your balance jumps up to $930,509 if you earned a 12% return.

Now, you can evaluate the results and make an informed decision.

Knowing that $10,000 today projects to nearly a half million dollars at retirement age may make this an easy decision for you.

One important note: when studying your results, pay attention to the shape of the compound interest graph.

Compound interest takes time to work its magic. That’s why your $10,000 investment doesn’t skyrocket right away. In fact, it can take a couple of decades or longer for compound interest to show its true power. This is why it’s important to invest early and often.

Choice 4: Pay down student loan debt.

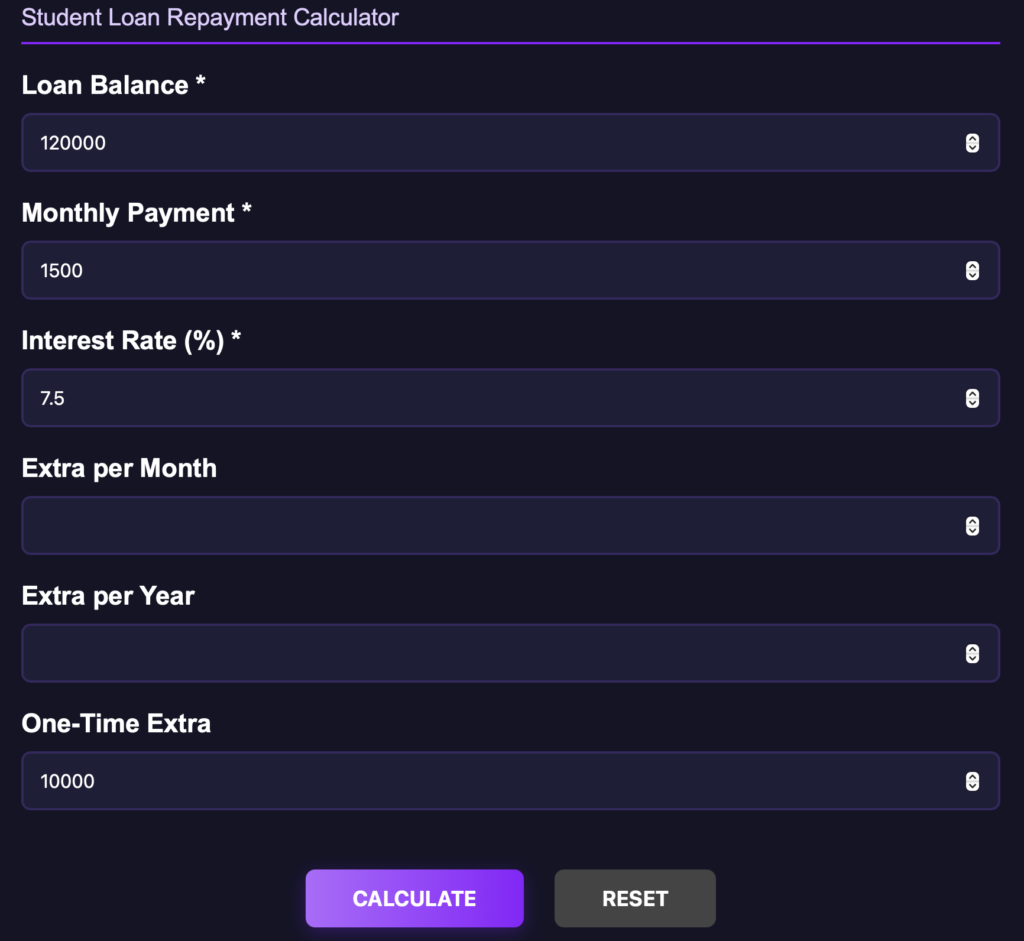

Let’s continue our previous assumption that you are 27 years-old. Now, we’ll add it some additional assumptions regarding student loans.

Let’s assume you have $120,000 in loans and your monthly payment is $1,500. Let’s also assume that your interest rate is 7.5%.

With the Think and Talk Money Student Loan Calculator, you can see how much money and time you will save by making extra payments.

Here’s what it looks like when you plug in a one-time extra payment of $10,000:

Now, let’s look at how much money and time you saved by making this one-time payment:

This one-time payment of $10,000 saved you $19,269.97.

It also knocked off 13 months of loan payments from your payoff schedule.

Focus on just those 13 months for a moment. By making this one choice to use your $10,000 bonus to pay down debt, you bought yourself more than a year of freedom from paying off loans.

That is an incredibly freeing feeling.

Not only will your debt be eliminated more than a year faster, you’ll also be able to prioritize your other financial goals a year faster.

Think about how exciting it will be to repurpose the $1,500 you had been paying toward debt each month.

Once again, that’s an incredible feeling.

Play around with your own numbers in the Think and Talk Money calculators.

If you’re anything like me and the law students I’ve taught over the years, financial calculators can be powerful motivational tools.

As we saw with our examples today, you will receive outsized benefits in the future if you can just stay disciplined with your spending today.

Using the Think and Talk Money calculators, you may decide to prioritize investing for retirement. Or, you may be driven to eliminate your loans faster.

Take some time to play around with the calculators using your own financial situation. You will be amazed at the progress you can make towards your goals with even slight adjustments.

You may even be motivated to take action with your bonus to accomplish your long-term financial goals.

Have you used financial calculators before?

Were you surprised by the results?

Let us know in the comments below.

Leave a Reply