I recently attended a “financial empowerment” workshop hosted by a financial advisor.

The financial adviser was smart and very passionate about helping people plan for retirement. She shared a lot of valuable information, such as investing early and often.

She also shared good examples on how compound interest works and how inflation eats away at our purchasing power.

I liked just about everything she was sharing with the audience. It was solid advice, and her presentation included many informative charts and examples.

I was not even bothered that she was frequently pitching her services in hopes that audience members would hire her to manage their money. It was her presentation and she earned the right to promote herself.

The thing is, and I was not surprised by this in the least, the topic of fees hardly came up at all.

In fact, the first mention of fees did not come up until the very last slide. In total, fees were addressed for maybe 30 seconds in an hour-long presentation.

I don’t necessarily blame the advisor for not discussing fees until the very end. She’s trying to make a living and doesn’t want to scare people off before hearing what she had to say.

I think most people in her situation would have structured the presentation the same way.

That said, in my opinion, fees should be one of the first things discussed when it comes to investing. It should not be a throw-in at the end of a presentation.

The amount we pay in fees is one of the main things we as in investors can control.

There is not much we can control as stock investors. Markets are unpredictable. One of the only things we can control is the amount we pay in fees.

There are two primary types of fees: transaction fees and ongoing fees.

- Transaction fees are charged each time you make a transaction, like buying a stock.

- Ongoing fees are charged regularly, like account maintenance fees.

Whenever you are choosing how to invest your money, pay close attention to the fees associated with that investment option.

You cannot avoid fees completely, but you can minimize the amount you pay depending on the investments you choose.

Below, we will take a look at how even a seemingly small fee of 1% can have a huge negative impact on your account balance over time.

As a general rule, passively managed investments like index funds, charge lower fees. Actively managed investments charge higher fees.

If you choose to work with an investment advisor, be sure to understand all of the fees charged for those services. Pay particular attention to the ongoing fees, which can have a big impact on your investment portfolio.

I am not on a crusade against financial advisors.

Before all the financial advisors out there bite my head off, let it be known that I am not on a crusade against you.

Believe it or not, I’m not here to tell anybody whether he should work with a financial advisor or not. That’s not for me to decide.

I believe that advisors can offer significant benefits to a lot of people, including benefits that are difficult to quantify. For example, an advisor may help someone stay calm during market dips so that person stays invested for the long term.

I view my role in the personal finance food chain as that of an educator. I am not a financial advisor, and I won’t be giving personal investment advice.

My purpose in writing this post is to help you decide whether the cost of hiring an advisor is worth it to you.

I do the same thing when I teach personal finance to law students. I try my best to present options and information so they can make the best decisions.

When it comes to investment fees, it’s hard to know exactly what we’re paying. What does a 1% fee even mean?

By looking at the examples below, you should get a better idea of what a 1% fee looks like over the long term. Then, you can be better equipped to make a thoughtful decision on whether to work with an advisor.

In the end, I’ve done my job if I’ve helped you acquire enough personal finance knowledge to make educated choices with your money.

So today, we’re going to talk about fees.

Remember, none of us can control the market, and that includes financial advisors. The best any of us can do is project what may happen in the future based on what has happened in the past.

Since we can’t control the market, let’s focus on what we can control, like fees.

To help us understand how fees can be a drain on our investment returns, let’s revisit our friend Sally.

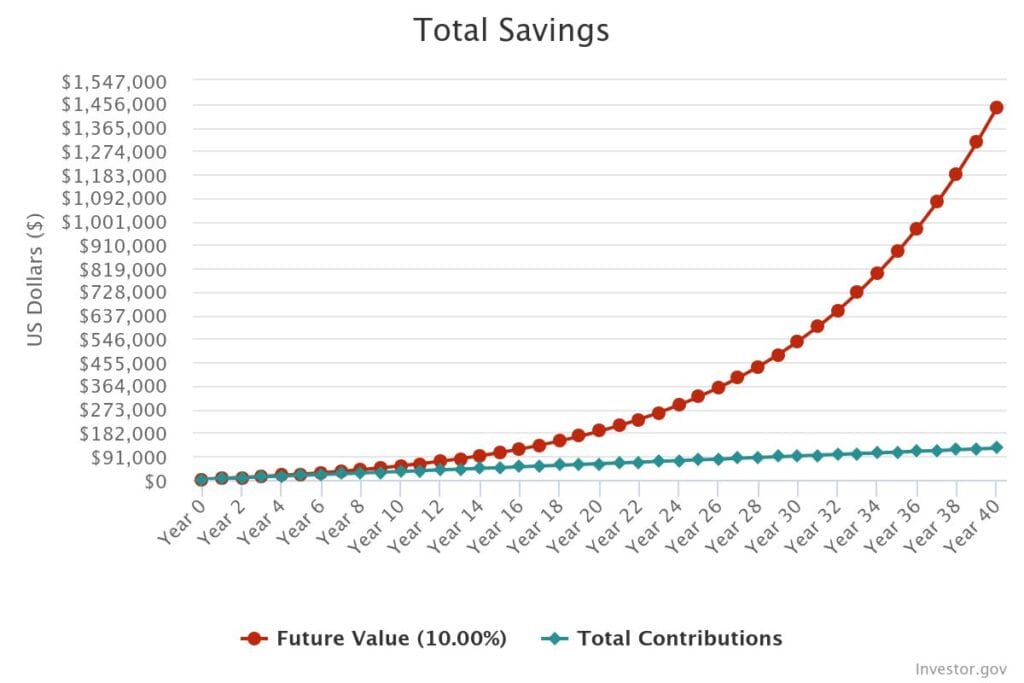

Sally earns 10% a year and pays no advisor fees.

Remember our friend, Sally?

While in her 20s, Sally funded her retirement account with an initial contribution of $2,500. She then made contributions of $250 every month for 40 years.

She was comfortable with reasonable risk and invested in the S&P 500, which has historically earned an average annual rate of return of 10%.

After 40 years, Sally had contributed a total of $122,500.00. Her retirement account grew to $1,440,925.81.

Sally set herself up to have a lot of choices come retirement.

Now, let’s make one slight adjustment to our hypothetical to account for a fee of “only 1%.”

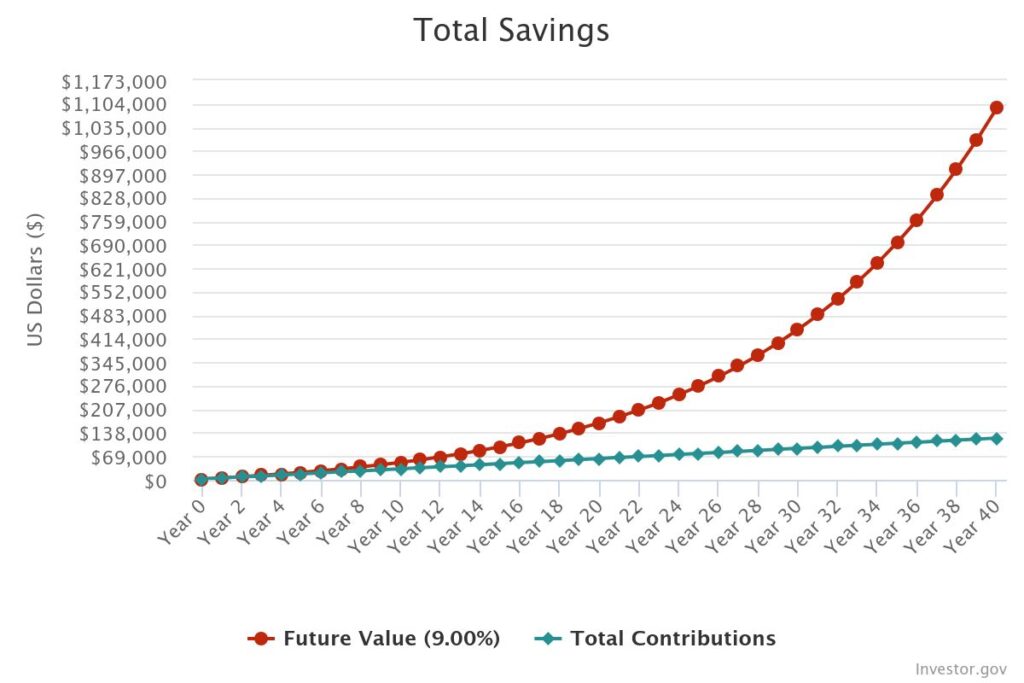

Sally earns 10% a year and pays a 1% advisor fee.

Let’s assume that Sally decided to work with a financial advisor that charges a 1% fee. That means every year, Sally pays her advisor 1% of her account balance.

We’ll assume that her advisor also averaged a 10% annual rate of return for Sally. However, because Sally pays her advisor a 1% fee, Sally’s actual earnings rate drops from 10% to 9%.

Let’s see how that 1% fee changes Sally’s performance over 40 years.

After 40 years of earning 9% after paying a 1% fee to her advisor, Sally will have $1,092,170.89.

The 1% fee resulted in Sally’s account dropping by $348,754.92.

That’s 24% less money than she had in our example when she earned 10%.

The impact of even a 1% fee is monumental.

Through this example, you should be able to see that even a seemingly small fee can have major consequences on your long term gains.

When people start investing, the 1% fee does not seem like a bad deal. In my experience, whenever a financial advisor has explained fees to me, he uses words like “just 1%” or “only 1%”.

I think that language is misleading and deceiving. Sally would probably agree that words like “only 1%” do not accurately express a cost of $350,000.

If you look at the very beginning of Sally’s investment profile, it’s true that the 1% fee seems to have little impact.

In Sally’s case, the difference in her account in the two scenarios after 1 year is only $25.

- Sally’s account after 1 year at 10% interest: $5,750.

- Sally’s account after 1 year at 9% interest:$5,725.

That’s a pretty marginal difference. However, it takes time for the impact of fees to materialize.

The reason is because it takes time for the magic of compound interest to set in. That’s why we need to invest early and often.

Let’s look at the difference in Sally’s account over time:

10% Return | 9% Return | |

|---|---|---|

| After 1 year | $5,750 | $5,725 |

| After 10 years | $54,296.63 | $51,497.20 |

| After 20 years | $188,643.75 | $167,491.39 |

| After 30 years | $537,105.57 | $442,091.81 |

| After 40 years | $1,440,925.81 | $1,092,170.89 |

Looking at these numbers, it becomes clear how much a 1% fee can impact your overall investments.

One other consideration: the fee also typically gets taken straight out of your account. That can make it feel like the fee is relatively small or doesn’t exist at all.

It would feel much different if each month you had to go through the process of writing a check to your advisor. Maybe feeling that pain would impact your decision to pay the fee.

Decide for yourself if the real cost of an advisor is worth it to you.

You can play with these numbers to match your personal situation. Maybe you have an advisor charing less. Maybe yours charges more.

If you want to tweak the annual rate of return you expect to earn by working with an advisor, please do.

Or, maybe you just want to ask your advisor or potential advisor about fees and how they may impact your portfolio over the long term.

Hopefully, looking at these numbers gives you something to think and talk about.

I personally do not work with a financial advisor.

Let’s circle back to the financial empowerment workshop I attended the other day.

At its conclusion, the advisor’s husband came by to collect the sign-up sheet. I happened to be the last person to receive the clipboard.

Seeing that I had not signed up for a free consultation, he looked at me and said, “Oh, you forgot to sign up!”

I chuckled.

Uhh, no I didn’t “forget”.

I respectfully declined to be added to the list. I’ve chosen not to work with an advisor.

I shared my story about how I set $93,000 on fire when my former advisor pulled me out of the markets in 2008.

In that post, I also shared that it wasn’t her fault. It was my fault for not being educated.

Since then, I’ve been convinced by endless reports, such as this from Yahoo! Finance, that I’m better off without an advisor when considering the cost:

Making matters worse is that the professionals, who the average investor might turn to for guidance, have poor track records. In the past decade, an alarming 85% of U.S.-based active fund managers underperformed the broader S&P 500. Those who invest in these funds are essentially paying for unsatisfactory results.

How much does 1% matter to you?

I recently calculated how much I would have paid an advisor by this point in my life. I determined that If I had been working with an advisor, I would have paid more than $100,000 in fees so far.

When I think about all the things I could do with more than $100,000, I’m very happy that I chose to educate myself and keep that money instead of paying it to an advisor.

Maybe I would have earned more if I worked with an advisor. Maybe that $100,000 would have been a worthwhile price to pay. Then again, maybe not.

If you choose to work with an advisor, I won’t blame you. Hopefully your advisor consistently beats the returns of the S&P 500 or provides value to you in other ways.

Whatever the case may be, you now should have a better understanding of what you’re paying when you hear the phrase “only 1%.”

- Do you work with an advisor?

- What fee does your advisor charge?

- What are the top benefits you receive in exchange for the cost?

Let us know in the comments below.

Leave a Reply