The financial independence community sometimes gets a bad rap for encouraging excessive saving at the expense of present day spending.

The reputation is not entirely undeserved.

I listened to a podcast once where the guest admitted to the folly of trying to replicate Trader Joe’s trail mix by buying each of the ingredients individually and mixing them himself.

I thought to myself, “This is what financial independence is about?”

That never sat right with me.

The podcast guest was happy enough to admit that the meager savings from making his own trail mix was not worth his time or energy. Still, if there was ever one aspect of the financial independence community that turned me off, it was advice like “make your own trail mix.”

He was not alone in promoting what I considered excessive frugality. The word “miser,” referring to someone extremely stingy with money, comes up regularly in criticisms of people pursuing financial independence at all costs.

To this day, I’ve never connected with the voices that promote extreme saving at the expense of present day convenience and fulfillment.

I’ve also come to learn that this type of personal finance advice doesn’t work for lawyers.

Advice like “make your own trail mix” doesn’t work for lawyers.

As lawyers, we invest a lot of time (and money) into our education and careers. It’s no secret that we work long, stressful hours. One of the tradeoffs for all the hours we put in is that we have the opportunity to earn high incomes.

Considering we work long hours and earn good money, advice like “make your own trail mix” isn’t very helpful. It’s not worth saving a few pennies in exchange for our limited free time when we could be doing the things that make us happy. When we’re not working, our time and energy should be better spent elsewhere, like being with our family, socializing with friends, or relaxing.

What I’ve learned teaching personal finance to lawyers is that we are generally not interested in saving every penny possible until we can quit our jobs. This makes sense to me. Putting that much constraint and pressure on ourselves does not sound like a fulfilling existence.

The lawyers that I work with know they need to save for retirement. At the same time, they want to use some of their hard-earned money for a better existence today.

That’s why I recommend that lawyers spend money in ways that increase happiness, convenience and time. One of the best ways to practice this type of intentional spending is to create a Budget After Thinking.

When you follow a Budget After Thinking, you give yourself permission to spend on things that make you happy today, while still achieving your long-term goals.

Personally, shopping at Costco is an example of spending money today that brings me happiness, convenience, and time.

What I learned about spending money by shopping at Costco.

This past Sunday afternoon, my wife and I took the kids to Costco. I was thinking about all this while we walked through the store loading up our two carts.

It was a nice family outing. We killed a couple of hours, the kids had fun, and we have food and supplies to last us for a month.

On average, we shop at Costco once per month. We get our staple items (toilet paper, ground beef, coffee, etc.) and always end up with a few things not on our shopping list. On this weekend’s trip, the kids talked their way into Kit Kat chocolate bunnies (didn’t even know they made those) and enough AA and AAA batteries to power an airplane.

The thing about shopping at Costco: no matter your best intentions walking into the store, the final bill is always big. Somehow, the cart always fills up. What a business!

Anyone who shops at Costco will instantly know what I’m talking about.

I’m no longer shocked or disappointed with the final bill. When my wife jokingly asks what the total is, my answer is always the same, “A lot.”

What I’ve learned is that despite spending a lot of money at Costco, I view this as money well spent. We usually pick up some fun items that are relatively inexpensive and make us and the kids happy. Plus, because we load up on essential items to get us through the month, we don’t spend much time or money each week at the grocery store.

Even though the final bill is always big, I view shopping at Costco as an example of intentionally spending money in a way that increases happiness, convenience, and time.

Which leads me to one of the most important money lessons I’ve ever learned:

Sometimes, you gotta spend the money.

Sometimes, you gotta spend the money.

Personal finance is not only about saving. Yes, saving is crucial to achieving our long-term goals. But, I don’t recommend that we save so dogmatically that we make ourselves miserable along the way.

As lawyers, we work hard and we work a lot. If all we did was save every penny we earned in hopes of quitting our jobs one day, we would quickly burnout.

Instead of making your own trail mix, remember this piece of advice:

Sometimes, you gotta spend the money.

Buy the direct flights.

Costco is only one such example of when it makes sense to spend the money. I spend a lot of money at Costco each visit. But, we enjoy our family outings and get most of the essential items we need for the month in one trip. That’s money well-spent on happiness, convenience and time.

If my goal was to save every penny possible, I wouldn’t feel the same way about Costco.

Not a Costco shopper? Here’s another recent example when I decided to just spend the money.

My brother-in-law’s wedding is in Scottsdale this fall. When I booked our flights, I could have saved real money by connecting in Denver or Los Angeles instead of flying direct to Phoenix. But, at what other cost?

Anyone ever flown across the country with young kids?

A four-hour flight with three young kids is hard enough. My wife has it especially tough with the baby on her lap the entire flight. By the time we land, it feels like we just worked out for 4 hours.

The last thing in the world that we need is to extend the adventure with a connecting flight, even if it saves real money. My priority is to arrive in Arizona feeling energized and excited to celebrate this once-in-a-lifetime event with my family.

Sometimes, you gotta spend the money.

Personal finance is tied to our emotions.

Humans are emotional creatures. Of course, we can rationally look at examples and charts and won’t dispute the long term magic of compound interest. At the same time, we have emotions and feelings that need to be tended to now.

At Think and Talk Money, we regularly explore how personal finance is tied to our emotions. There’s nothing wrong with admitting that in certain situations, the right choice is to spend the money.

Traveling is a good example of spending money to increase happiness. In fact, the happiness effect has been well-documented when it comes to traveling. People get a happiness boost in planning the trip, then taking the trip, and finally remembering all the fun things they did on the trip.

That’s why so many people “love to travel.” It brings them happiness before, during, and after the trip.

Personal finance is about how we spend money today, not just in the future.

Personal finance is not just about long term goals, like saving for retirement. Just as important, personal finance is about how we spend our money in the present.

It’s not realistic to expect people to put off all happiness until some unknown time in the future. It is realistic to make reasonable choices now to ensure a better future.

What might be a reasonable spending choice for one person may be totally unreasonable for someone else. That’s perfectly fine. Still, we all need to make those choices for ourselves.

What I’m suggesting is that if you’re spending most of your time each week at your job, like most of us lawyers do, shouldn’t we think about using some of the money we earn so we can elevate our present day lives?

The key is understanding what those things are, so we actually spend our money in pursuit of those things.

That’s the essence of what it means when I say, “s , you gotta spend the money.”

So, what’s a recent example of where you decided to spend the money?

As of this writing, the S&P 500 is down 3.3% in 2026 and the Dow is down 3.8%.

The market can change suddenly, for better or worse. Nobody knows what’s going to happen. Don’t believe anyone who tells you otherwise.

During times like this, it’s important for all of us, and especially young lawyers, to remember the fundamentals of investing.

I was asked recently, “What am I doing with my portfolio while markets are falling in early 2026?”

Despite how chaotic it may seem in the world today, this is not a difficult question for me to answer.

I’m not doing anything.

I invest in the stock market to help achieve my long-term goals. My two main long-term goals are to save for college and to save for retirement.

Each objective is so far away that time is on my side.

Our oldest child is six-years-old, so I have 12-13 years until she even begins college. Over the past two years, we super-funded a 529 college savings plan for my oldest daughter and my son. We plan to do the same for our baby girl.

I fully anticipate that the market is going to go up and down over the next two decades while my kids are in school. That’s part of the process.

As for retirement, I have even more time in front of me. Same as what we just talked about with saving for college, I fully expect the market is going to go up and down many times before I retire.

Time is on my side. That’s why I’m doing nothing.

Like you, I don’t enjoy seeing my portfolio drop so suddenly.

It’s not fun to read the headlines right now. My brain seems to jump to the worst case scenario. Maybe you do the same thing. As lawyers, we’re trained to think of the worst case scenario, right?

This is one of the reasons why I only look at my portfolio once per month when I track my net worth.

To remind myself to hold steady during the down times, I think of a study that examined what would happen if an investor missed the 10 best days for the market in each decade since 1930.

Looking at data going back to 1930, the firm found that if an investor missed the S&P 500′s 10 best days each decade, the total return would stand at 28%. If, on the other hand, the investor held steady through the ups and downs, the return would have been 17,715%.

These results illustrate how risky it would be for me to try to time the market. The last thing I want to do is miss the upswing. I have no idea when it’s coming.

But, time is on my side.

I’m going to be in the market when that upswing eventually comes. It may not be until years from now. That works for me and my investment horizon.

Think of it this way: the market is on sale right now.

One other mental hack that’s helping me right now:

I’m telling myself that the market is on sale. How so? I can buy the exact same stocks today for less money than they would have cost even a few days ago. I do love a good sale.

In the end, no matter how bad things seem right now, I plan to continue making regular contributions to each of my investment accounts.

Since I’m investing for the long run, I’ll let the market do its thing while I’m off doing my own things.

Disclaimer: Your situation may be different. I am not an investment advisor. Do your homework and make the best decisions for your personal situation.

What is my personal investing strategy?

When it comes to investing in the markets, I’m about as boring as can be.

My wife and I invest primarily in index funds. We are not active traders. We don’t seek out the newest, hottest stocks.

All we do is make regular contributions to our various investment accounts and let the markets take care of the rest.

As an example, for my daughter’s 529 plan, we chose a passive investment option that’s a mix of stock index funds and bond index funds.

Our portfolio automatically rebalances over time based on my daughter’s projected first year of college. Essentially, the closer we get to her first year in school, the more conservative our portfolio becomes.

We chose a similar option for our other kids’ 529 plans. It’s boring but it works.

Like so many others in the financial independence community, I fell in love with index funds after reading J.L. Collins’ book The Simple Path to Wealth. You can read my full review of The Simple Path to Wealth in my post here.

Even if you work with a financial advisor, it’s crucial to educate yourself so you can make informed decisions, especially in times of economic uncertainty like we’re in right now. As Collins explains, benign neglect of your finances is never the solution.

By the way, it’s not just Collins urging us to invest in broad based index funds. So does the single greatest investor of our lifetimes, if not ever: Warren Buffett.

In 2013, Buffett famously instructed that after he dies, his wife’s cash should be split 10% in short-term government bonds and “90% in a very low-cost S&P 500 index fund.”

How much money should you put towards each of your financial goals?

Between saving for emergencies, saving for college, and saving for retirement, there are a lot of options. In addition, you may have other short term goals, like paying for a wedding or a house. Or, you may want to invest in real estate.

So, how do you determine how much to allocate to each goal?

Once you know what you’re striving for, it’s time to commit to a Budget After Thinking. The primary focus of a Budget After Thinking is to generate fuel for the most important goals in your life.

Are you saving too much for retirement?

Spend enough time on the internet, and you’ll get many different answers about how much to save for retirement. There are just too many variables in play to generally answer this question, like what kind of retirement you want and when you want to retire.

My perspective on retirement savings evolved after reading Die with Zero by Bill Perkins.

In Die with Zero, Perkins suggests that many of us are saving too much for retirement at the expense of using that money to live our best lives now.

Perkins’ book is one of the most compelling personal finance books I’ve read in a long time, and I highly recommend it.

Perkins is not suggesting that saving for retirement isn’t important. He’s saying that the hard data shows that most of us are over-saving.

Believe it or not, you may be closer than you think to achieving your retirement goals.

That’s a very powerful realization.

Think about the options you can create for yourself if you no longer need to save a hefty chunk of your paycheck for retirement.

Personally, after reading Die with Zero, I used the Think and Talk Money Coast FIRE calculator to estimate my projected retirement savings. As Perkins would have expected, at our then-savings rate, my wife and I risked over-saving for retirement. In other words, we have reached Coast FIRE.

With that realization, I made some adjustments and am now targeting my other financial goals at a faster rate. I’m also not skipping out on any experiences that appeal to me because of fears about retirement.

Coast FIRE relates to Perkins’ thesis that many of us are over-saving for retirement.

The central idea behind Coast FIRE is to aggressively fund your retirement accounts early in your career so you won’t have to save for retirement as you get older.

For lawyers more established in their careers, Coast FIRE represents the idea that all those earlier years of saving means you no longer need to worry about retirement. You can sit back and let compound interest do its thing. Your retirement years are covered.

This is the essence of Coast FIRE: knock out retirement planning early on to create more career and life flexibility later. Coast FIRE does not mean you can stop working altogether. It means that you no longer need to save for retirement.

Why is achieving Coast FIRE so beneficial?

Because once you hit your projected magic retirement number, you no longer need to fund your retirement accounts. With retirement covered, you can reallocate those funds to other financial or life goals. That means you have more optionality in life.

For example, you won’t need to earn as much money if you’re not allocating a big chunk of your income to retirement. That opens up the possibility of switching jobs or working fewer hours. It also means that you can focus more dollars on your present-day self.

Achieving Coast FIRE also means that you can focus on adding present day liquidity to your portfolio. Liquidity means having cash and investments immediately available in case you need it. Increasing liquidity is an important step for maximizing optionality in your life.

On top of that, when markets are dropping, knowing that you have cash-on-hand can give you a lot of confidence to ride out the dip.

How do you figure out if you have achieved Coast FIRE?

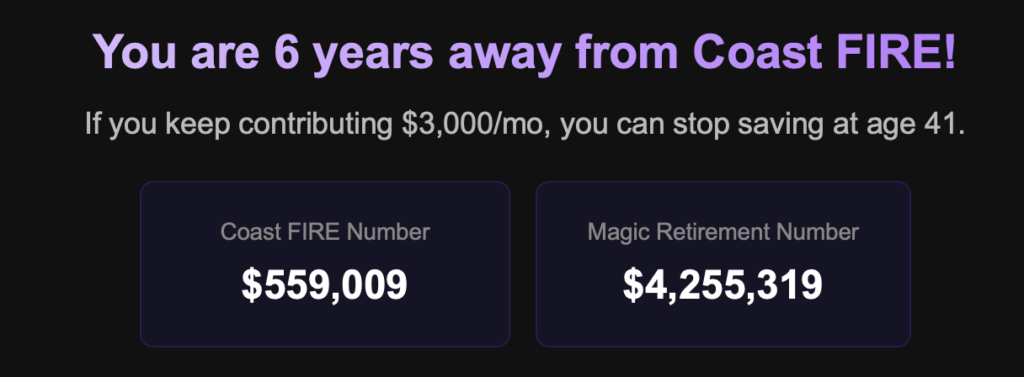

Let’s say you are 35-years-old and plan to retire at age 65. After 9 years of working at a law firm, you have $400,000 saved up in your various retirement accounts. You also currently contribute $3,000 per month to your retirement accounts.

Your goal is to have $200,000 annually to spend in retirement.

We’ll assume an average annual return of 10% (on par with the historical results of the S&P 500). We’ll also factor in a 3% inflation rate (the historical average in the United States). Finally, we’ll assume a safe withdrawal rate of 4.7% in light of the updated “4% Rule.”

Based on the above variables, your Coast FIRE number is $559,009.

What does this mean?

At your current saving rate, you will have $559,009 saved up and will reach Coast FIRE in six years. That means that at the age of 41, you will no longer need to fund your retirement.

The big win is that the $3,000 you had been saving for retirement can be repurposed for other life goals or experiences.

Yes, you need to keep earning money to sustain your present lifestyle. However, you have the option to pursue a lower paying, lower stress job because your retirement years are already covered.

Note: Your FI number (magic retirement number) is significantly higher: $4,255,319. That’s how much money you’ll need saved up by the time you turn 65 in our example to spend $200,000 annually in retirement and not run out of money. Because of compound interest, your balance should grow to that amount without any additional contributions after age 41.

When markets are falling, stick to investing fundamentals.

If you are a young lawyer with a long investment horizon, you shouldn’t be concerned when markets are falling like they recently have been.

Time is on your side. Stick to the fundamentals.

I prefer to invest in broad based index funds, like Collins and Buffett recommend. Regardless of markets rising or falling, I make regular contributions and let compound interest work its magic.

Because I have already achieved Coast FIRE, I am now focused on building more liquidity, which translates into more optionality.

It’s not as much fun to track my net worth these days, but the cyclical nature of the markets is part of the process we need to accept.

Young lawyers: what do you tell yourself when markets are falling, knowing you have a long horizon?

Does it help stay the course if you talk to your people?

Jay Leno: former host of The Tonight Show and famous comedian.

Rob Gronkowski: Super Bowl champion and celebrity spokesperson.

Matt Adair: just like them.

At least, in one way.

The three of us follow the same money philosophy when it comes to how we earn and spend.

This philosophy has become known as the “Jay Leno Rule.”

Here’s how the Jay Leno Rule works, as explained by the man himself in an interview with CNBC:

From the moment he entered the working world, “I always had two incomes,” [Leno] explains to CNBC. “I’d bank one and I’d spend one.”

And he made sure to spend the smaller amount.

“When I was younger, I would always save the money I made working at the car dealership and I would spend the money I made as a comedian,” he says. ”When I started to get a bit famous, the money I was making as a comedian was way more than the money I was making at the car dealership, so I would bank that and spend the car dealership money.”

“When I got ‘The Tonight Show,’ I always made sure I did 150 [comedy show] gigs a year so I never had to touch the principal,” Leno says. “I’ve never touched a dime of my ‘Tonight Show’ money. Ever.”

″So many people get to be the age I’m at now and they’ve got nothing because they just blew it all,” he says. “I put my money in a hammock and say, ‘You relax. I’m going to go work.’ And when I come back, I put some more money in the pile.

“It sounds ridiculous, but if everything ends tomorrow, I know I’ll be fine.”

The Jay Leno Rule is such a simple and powerful money philosophy.

The Jay Leno Rule boils down to three simple steps:

Earn income from multiple sources.

Spend only the money from one income source, preferably the smaller one.

Save and invest the rest.

If you can employ this strategy, you can create significant wealth for you and your family.

I’ve been following the Jay Leno Rule since 2011 when I started with my law firm and got my first job teaching at a law school. More on that below.

First, let’s revisit Leno’s story.

When we think of Leno today, we think of the famous and wealthy host of The Tonight Show. His net worth is estimated to be $450 million. He could buy anything he wants.

But, read his story again. He developed good money habits before he got famous. He earned two incomes from working at a car dealership plus doing standup comedy shows and always saved one of those incomes.

Don’t gloss over that part. Leno established a strong financial foundation early in his career, before he started making a ton of money.

Because he had established the habit, he continued earning multiple salaries, even after his income soared with The Tonight Show. That’s impressive.

Leno’s story shows why practicing good money habits is so important early in our careers.

You’ll also notice that Leno took nothing for granted: “if everything ends tomorrow, I know I’ll be fine.”

Leno wasn’t referring to the world ending. He was talking about losing his job. He meant that if is income went away, he had saved enough that he didn’t have to worry about it.

NFL legend Rob Gronkowski applied the Jay Leno Rule during his career as an NFL superstar and celebrity endorser. He explained his money philosophy recently on the “Bussin’ with the Boys” podcast:

“I didn’t know how long the NFL was gonna last. I was a second-round pick, so it was like a four-year, $4 million deal, and I was like, if I can play this contract out, I’ll be set for life.

I just always wanted to save it, and I just used my money that I was getting off the field to just spend it on whatever I needed to spend it on. Technically, I have not spent any of my NFL money.”

Gronk is a very smart man. Just like Leno, he established the habit of saving one of his sources of income early in his career.

Again like Leno, he didn’t take his career for granted. He didn’t fool himself into thinking that his high salary would always be coming in. Even if he got injured or failed to perform during his initial contract, he would be just fine.

Imagine how much confidence that gave him on and off the field. Because he knew he was set financially, he did not have added pressure to perform. He could be himself and play the sport that he loved without worrying about his next contract.

There’s no doubt in my mind that feeling of financial freedom helped him perform at his best on his way to winning four Super Bowls.

How I’ve applied The Jay Leno Rule to build significant wealth.

Just like Gronk, I have applied the Jay Leno Rule since I first earned multiple income streams in 2011.

Back then, I had just left my first job after law school as a judicial law clerk and started at my law firm. It was also the first year I taught a law school course.

My primary financial goal at the time was to pay off my student loan debt. The Jay Leno Rule helped me do just that in a fraction of the time it otherwise would have taken.

Executing the strategy was easy. When I received my monthly paycheck from teaching, I immediately made an extra payment on my loans. It gave me an emotional boost to put that money to good use before I was tempted to blow it on something else.

I wasn’t earning a lot teaching back then, but every bit helped to accelerate my debt payoff.

You can play around with my Student Loan Payoff Calculator and see for yourself how even small extra payments can make a huge difference.

I did the same thing with any bonus I received: as soon as it hit my account, I used it to pay off my loans.

The Jay Leno Rule works because it forces you to save money.

Even though most of us would agree that we should be saving more money, sometimes it’s easier said than done. That’s where Jay Leno’s Rule is so helpful. If you commit to the philosophy, you’ll be forced to automatically save your supplemental income.

Once you commit to the philosophy, the execution is easy.

As soon as the money hits your checking account, you move it to one of your savings or investment accounts, or use it to pay off debt. Do this right away so you don’t get tempted to spend the money elsewhere.

This is exactly what I continue to do today because I knew that if the money sat in my checking account, it would slowly disappear.

One other tip: don’t include this money in your Budget After Thinking. Pretend you never even had the money. This is a money mindset trick that will help you solidify the habit.

Because my teaching paychecks and bonuses were irregular, I did not factor them into my budget. It might sound silly, but I just pretended that extra money wasn’t really mine. As soon as it came in, I put it to good use.

Help yourself out by pretending your supplemental income isn’t even yours. This applies to side hustles, bonuses, windfalls, etc.

Use this extra money to advance your financial goals and continue living off of your salary.

The key to establishing the habit is starting early in your career, like Leno and Gronk did. It’s important to do this before you become dependent on spending the supplemental income.

I have used the Jay Leno Rule since 2011 to turbocharge my net worth.

As the years went on, my wife and I have added income streams and continue to use the Jay Leno Rule. Here’s a snapshot of our income streams:

My salary as an attorney

Bonuses earned as an attorney

My wife’s salary as an attorney (until 2025)

Chicago Rental Property 1

Chicago Rental Property 2

Chicago Rental Property 3

Colorado Rental Property

Law School Course 1: Financial Wellness for Lawyers

Law School Course 2: Moot Court & Appellate Advocacy S.1

Law School Course 3: Moot Court & Appellate Advocacy S.2

Adhering to the Jay Leno Rule, my wife and I have only ever spent our salaries as attorneys. The rest of the income we earn goes directly to our financial goals.

Since 2011, we’ve built significant wealth by applying this simple strategy. Our financial goals evolved, but the strategy remained the same: earn multiple sources of income, live off of one source, invest the rest.

Early in my career, my primary financial goal was to get out of debt. Whenever I earned a bonus or a paycheck from teaching, I immediately transferred the money out of my checking account to pay down the debt.

Within a few years, my debt was gone.

But, I didn’t stop applying the Jay Leno Rule just because I was out of debt.

I had already done the hard part and established the habit of using any supplemental income for financial goals. That made it easy to then use any supplemental income to build up my assets.

That meant I could more aggressively invest in the stock market and more quickly acquire rental properties.

Today, my wife and I continue to apply the Jay Leno Rule. Any income from bonuses or side hustles goes immediately to paying off debt or to fueling our investments.

At first, I didn’t fully appreciate the impact the Jay Leno Rule had on my finances. That’s how personal finance works. It takes time for compound interest to work its magic.

Now, I’m seeing the results from the “forced savings.”

And, I’m so grateful that I learned the Jay Leno Rule early in my career.

I’ve had side hustles for just about my entire career as a lawyer.

My first side hustle was as an adjunct professor at a local law school, teaching just one class. I made hardly any money when I started teaching. It didn’t matter to me. I wasn’t dependent on the money to feed my lifestyle.

I was playing the long game. Because I got my foot in the door and did a good job, the school took notice. At my peak, I was asked to teach four classes. That meant I earned a lot more and could put all that extra income to financial goals.

At the same time, I also launched a rental property business with my wife. We now manage 11 rental units in Chicago and Colorado.

By the way, earning more money does not only apply to side hustles.

There are always ways to make more money within your primary job.

For example, can you earn a larger bonus by performing better?

Can you ask your employer for more responsibilities and a corresponding raise?

Or, can you earn additional money by generating business for your company?

It’s no secret that lawyers have the ability to earn more money if they generate business. That means bringing in clients.

How can you find these clients?

You can make it a priority to go to more events where you might meet potential clients.

You could launch a blog or create other content to help people find you and know what you do.

Either one of these pursuits could be your side hustle.

There are endless opportunities for anyone that is motivated and is looking to earn more money.

And when you earn and invest that additional money, you’re on your way to financial independence without having to sacrifice the things that make your daily life enjoyable.

If you take on a side hustle, don’t forget the Jay Leno Rule.

I recommend that every young lawyer take on a side hustle or look to earn supplemental income. And, when you start earning extra money, don’t spend it. Apply the Jay Leno Rule.

Never forget that when it comes to side hustles or supplemental income, it’s what you do with that extra money that makes it worth it.

A side hustle is another time commitment, after all. If you’re going to take on the responsibility, make sure it counts.

Before you consider a side hustle, have a plan in place for why you want additional money.

Are you looking to pay down debt faster?

Save for a wedding?

Invest in your first rental property?

To help you think through why you might want a side hustle, check out these three posts:

BTW, you’re not too busy or important for a side hustle.

Some lawyers reading this will automatically think, “I’m way too busy to even think about another job.”

In my personal finance class for law students, we spend a lot of time challenging that notion. Very few people- and I mean very few- are too important or too busy to take on a side hustle.

You may think you’re one of those “too important” people. I would challenge you to assess whether you’re confusing “too important” with “too stressed.”

Setting that conundrum aside, the ideal side hustle is something you enjoy doing that can earn you extra money at the same time. Some examples my students have come up with in class include:

Bartending. Entice your friends to come to your bar by offering cheap drinks. You get to hang out with them and get paid at the same time.

Fitness instructor. Instead of paying $48 for the spin class you love, become the instructor and get paid to lead the class.

Dog Walker. If you love dogs and don’t currently have one of your own, what better way to fill that void in your life while making money. The same applies to babysitting.

Home Baker. Make homemade treats with your kids and sell them to parents who don’t have the time.

The point is there are always ways to make more money by doing things you like to do anyways. Even if you’re busy. You just have to exert some mental energy to figure out how.

This idea of being “too busy” reminds me of a conversation my dad and I had when I was in high school.

Growing up, my siblings and I were busy kids. Sports, clubs, performances, classes, you name it. I made a remark to my dad about it at one point.

He responded that being busy wasn’t a bad thing because you don’t have time to fool around. When you have no choice other than to stay focused, you actually perform better in all facets of life.

You’re not thrown off by distractions because you’re locked in on accomplishing your goals. Back then, that meant going to class followed by soccer or basketball practice, a quick dinner, some homework and bed. I didn’t have any time for fooling around.

The same is true today.

I take care of business as best I can, while prioritizing my family and my health, and don’t have a lot of time to goof around.

I can see your eye rolls through your screen.

This guys is nuts. He’s a workaholic.He has no life.

If you want to get ahead financially, you really only have two options.

At the end of the day, there are really only two ways to get ahead financially: spend less money and/or make more money.

Of course, if you really want to get ahead financially, earning more money at the same time you’re spending less money is a dominate combination.

This is what Jay Leno and Gronk did. It’s also what I did.

I was talking to a friend recently. He wants to improve his financial situation. After all of life’s expenses, he doesn’t have much left to invest and get ahead.

We talked about how there are no shortcuts. He either needed to start making more money or needed to spend less. It wasn’t what he wanted to hear at first. He wanted a quick fix.

Money doesn’t work that way, even if you win the lottery, inherit a large sum of money, or earn a huge bonus. If you don’t have a strong foundation, that money will disappear as soon as you get it.

If you take on a side hustle, you can use every dollar you earn to get ahead. Since this is new money you’re earning, you shouldn’t need it to fund your life’s expenses.

Avoid the temptation of using that money on things you don’t really want anyways.

One more tip: use a financial calculator to see how much faster you’ll reach your goals if you’re able to throw additional money at them each month. Track and watch your net worth grow.

If you’re not ready for a side hustle, the same logic applies anytime you earn a bonus or commission at your primary job. Put that money to good use by paying down your debt.

Start using the Jay Leno Rule and never look back.

This concept of living off of my salary and not spending any bonus or side hustle income is one of the biggest reasons for my net worth today.

I recommend anyone striving for financial independence make the same commitment to not spend your supplemental income.

The hard part is getting past the initial temptation to spend your bonus money. If you can convince yourself that you don’t need the money right now to live the good life, you will be significantly better off down the road.

One of my favorite experiences teaching personal finance to law students involved a side hustle story. A couple of years ago, a student approached me during a break and told me about his credit card debt. It had been weighing heavily on him.

After our discussion about side hustles, he committed himself to driving for DoorDash and using the income to pay off his credit card balance.

Six months later he sought me out to share that the plan worked. His side hustle allowed him to pay off his credit card in less than six months. All while working a full-time job and attending law school par-time.

I couldn’t have been happier.

Jay Leno would certainly have approved.

Do you adhere to the Jay Leno Rule?

Has it helped accelerate your progress towards financial independence?