I read an article the other day where the author says he’s not going to save another dime for retirement. He reasoned that waiting for compound interest to kick in takes way too long.

He found a better way, he claimed.

Instead of investing in the markets long term, he’s going to buy small businesses that generate cash flow. He gave an example of buying a website for $10,000 that kicks off $400 per month.

That’s money in his pocket right now that he can spend in early retirement. He figures that owning ten small business like that is a faster and better path to retirement than traditional investments.

When you buy businesses, your cash flow increases. When you invest in stocks, only your net worth increases. Since you can’t retire off your net worth, you’re better off owning businesses.

The author suggested that everyone can do this and should be doing this. In his opinion, investing for cash flow is much more important than investing for long term net worth.

Do you want to own and manage ten businesses?

Interesting philosophy. I hope it works for him.

Personally, I won’t be following his lead.

For starters, how are you supposed to select, acquire, and operate ten small businesses? Is that even possible? If it is, it sounds like a major headache. As attorneys, we have enough headaches in our day jobs.

On top of that, I don’t buy his main concept that owning ten businesses will allow you to retire early. To me, owning ten businesses sounds like ten jobs and a lot of work.

As attorneys, we already have a demanding job and a lot of work. If you don’t want to work as an attorney anymore but want to keep working, maybe this is an idea you want to explore. If you want to retire and not work, this doesn’t sound like the ticket to me.

Finally, this scheme sounds risky. How many small businesses would I have to buy to land on 10 that actually generate cash flow?

According to the US Bureau of Labor, 18% of small businesses fail within their first year, 50% fail after five years, and approximately 65% fail by their tenth year. What are the odds that I’m going to own ten successful businesses that stick around long enough to fund my retirement? Way too risky for me.

In the end, the internet is full of schemes like this one promising a better and faster way to retire. Some of them might even work!

I’m not interested in going down this path. I’m sticking with the personal finance concepts that have worked for generations.

For today’s conversation, that means investing early and often to benefit from the magic of compound interest.

It’s not sexy. It’s not exciting. But, it works.

Here’s why.

Invest early and often to benefit from the magic of compound interest.

Compound interest is the interest you earn on interest.

How’s that for a confusing definition?

Fortunately, the idea of compound interest makes a lot more sense with a simple example.

Let’s say you make an initial investment contribution of $1,000. Let’s assume that you earn 10% interest each year on that investment. We will also assume that you re-invest your investment gains.

After the first year, your initial contribution of $1,000 earns $100 in interest (10% of $1,000). That means after one year, you have $1,100 in your investment account.

Because we are re-investing our gains, that means that at the start of year two, you have $1,100 to invest: $1,000 from your initial contribution plus the $100 earned in interest.

If you earn the same 10% interest on that $1,100 investment, you will have $1,210 at the end of year two.

Notice that in year two, you earned $110 in interest, whereas in year one you earned $100 in interest. That’s because in year 2, you earned interest on the interest your previously earned.

This is the key point about compound interest: you earned more money in year two, even though the interest rate remained the same and you did not contribute any additional money.

That’s how compound interest works. Compound interest is earning interest on interest you’ve previously earned.

Importantly, you don’t have to work harder or make the right decisions like you would if you owned a small business. With compound interest, you make more money as time goes on by doing nothing.

So, why is compound interest so powerful?

Earning an additional $10 in interest year two may not seem like a lot.

Over the long run, those additional earnings add up.

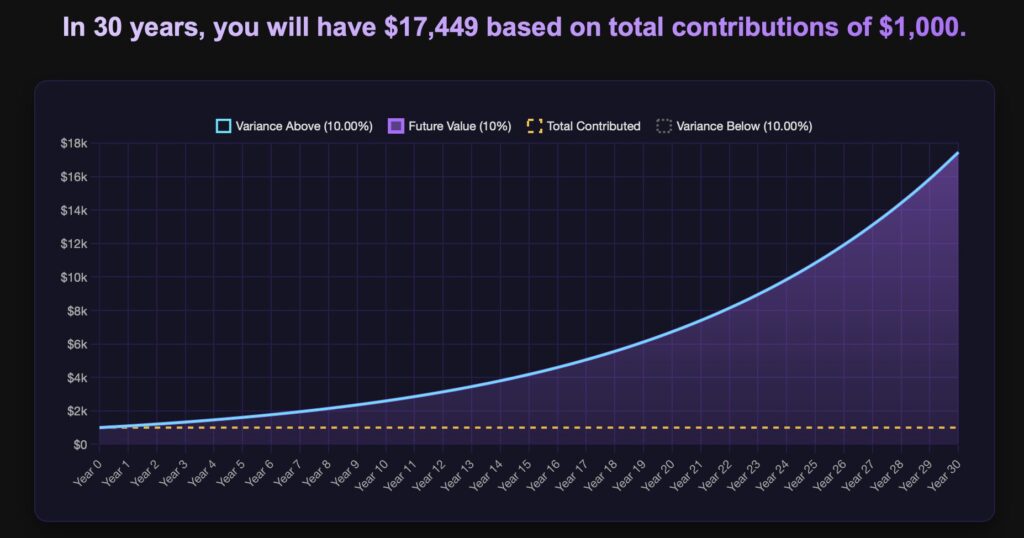

Let’s look at an illustration from the Think and Talk Money Compound Interest Calculator of what happens to that initial $1,000 contribution over a 30-year period:

In 30 years, you will have a total of $17,449.40. That’s a pretty good result from total contributions of only $1,000.

However, for this example, that total is not the important part. The important part is to visualize how compound interest worked its magic to get that result.

Look closely as the two lines on the graph. The dotted line that doesn’t change represents your initial $1,000 contribution.

The blue line represents the amount of money you have over time.

Notice how in the first 10 years or so, the dotted line and the blue line mirror each other pretty closely. Around year 12, you start to see some separation between the two lines.

While the dotted line stays flat, the blue line begins to arc upwards. That’s because all that interest you earned during the previous decade has been earning interest. Your investment begins to accelerate upwards without any additional contributions from you.

By the end of year 30, look at how steep the blue line is jetting upwards.

Like I said, compound interest is not sexy. But given enough time, it works incredibly well.

Look at the specific amount of money you’d earn each year in this hypothetical.

When you use the Compound Interest Calculator, you can also see how much more interest you earn each year as time goes on. Just click the button that says “Show/Hide Data Table.”

As we mentioned earlier, you earned $100 in interest during year 1. Then, you earned $110 in interest during year 2. That’s a good, but modest, increase.

During year 12, you earned $285.31 in interest. That’s significantly more than you earned in the early years, all without any additional contributions on your part.

During year 30, you earned $1,586.31 in interest!

The more time that you stay invested, the more money you’ll earn as compound interest works its magic.

That’s the power of compound interest.

Invest early and often to be a millionaire with very little effort on your part.

Compound interest is so powerful that it can make you a millionaire with very little effort on your part. All it takes is time and consistency.

Compared to owning ten small businesses, that sounds much easier.

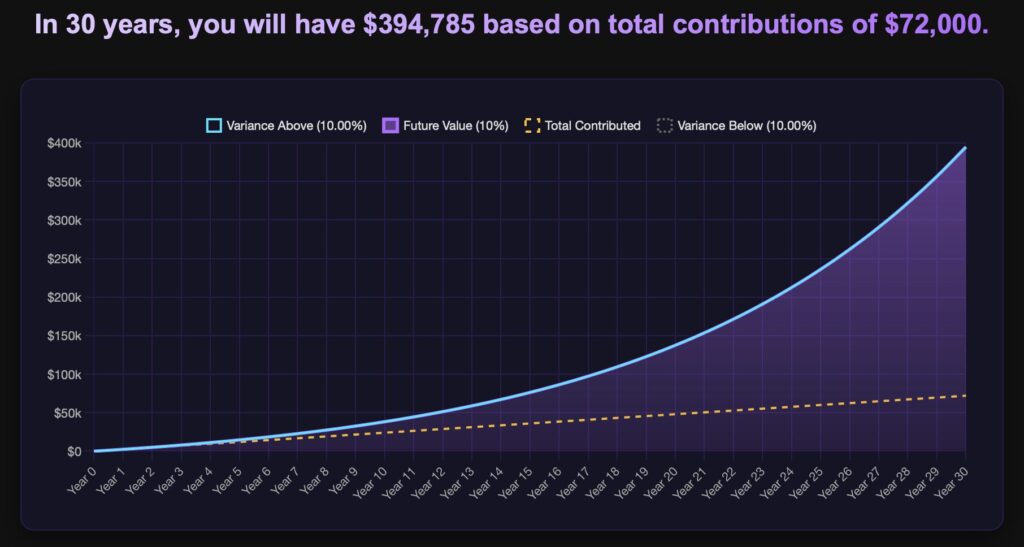

Let’s look at another example to see how you can easily become a millionaire if you invest early and often.

Let’s say you begin your career after going to law school or grad school at age 25. During your first year working, you saved up $3,000 and decided to invest in a low cost index fund.

You also make a plan to contribute an additional $300 per month to your investment account for the next 40 years, setting yourself up to retire at age 65.

We’ll also assume you earn the same 10% interest from our prior example, and you don’t make any withdrawals from your account.

To provide a fuller picture, we’ll also factor in a 2% variance rate, meaning you can see what would happen if you only earned 8% interest and also if you earned 12%.

Now, let’s see the results.

By the time you reach retirement age, you’ll have $1,729,110.97 in your retirement account at 10% interest.

That amount increases to $3,040,682 with 12% returns and drops to $997,777 with 8% returns.

That’s after contributing only $3,000 initially and $300 per month after that.

Put another way, your total contributions of only $147,000 turns into $1,729.110.97 by the end of your career. Even if the market performs below historical averages, you would still have nearly $1 million.

Take a look at the graph and notice the similarities to our prior example.

You’ll notice this graph looks almost identical to our prior example, even with the additional contributions that you make over time.

You can once again see that the lines mirror each other closely for the first 10-15 years.

Then, the dotted line stays relatively flat while the investment lines gradually arc up before skyrocketing towards the end.

Now, there’s no way to predict exactly when you’ll start to notice the magic of compound interest. There are too many variables at play.

The point is that given enough time, your personal investment trajectory should look similar because of compound interest.

You can play with your own numbers in an investment calculator like this one to match your personal situation.

If you’ve created a Budget After Thinking, you may be able to invest much more than $300 per month.

No matter what initial contribution you make and what interest rate you assume, you should notice a similar investment picture over the long run.

When I say investing is the easy part, this is what I mean.

I just showed you how an early contribution of $3,000 and regular contributions of $300 can turn into more than $1.7 million.

You don’t have to understand the math behind compound interest.

You just have to trust that it works.

Then, invest early and often.

Given enough time, assuming normal, historical market conditions, your investments will gradually increase before shooting up in the later years.

Read that sentence again. “Given enough time” is the key phrase.

The magic behind compound interest is time.

The earlier you can start investing, the better off you will be.

Since we can’t control investment returns, I prefer to focus on what we can control when it comes to investing.

We can control when we start investing and how long we invest for.

By making regular contributions over a long period of time, compound interest ensures that your wealth will grow.

Invest early and often.

People smarter than you and me preach the power of compound interest.

Warren Buffett, the world’s greatest investor, fully appreciates the power of compound interest. He’s famous for saying that his favorite holding period for an asset is “forever”.

Buffet’s not literally saying that there’s never a time or reason to sell an asset, like a a stock. He’s simply making the point that compound interest benefits people who stay invested over the long term.

If the world’s greatest investor isn’t impressive enough for you, how about the world’s greatest thinker?

Albert Einstein is often credited with this famous quote about compound interest:

Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.

You don’t have to be as smart as Buffet or Einstein to benefit from compound interest.

You just have to invest early and often.

Lawyers: would you rather manage ten businesses, or let your money quietly grow in the background thanks to compound interest?

Let us know in the comments below.

12 responses to “Why Personal Finance for Lawyers is so Important”

Well written, Matt! Best wishes to you in future endeavors.

Thank you, Bill!

Excited for the valuable advice!

Thank you, Clarke!

Hey, I think your ideas are very interesting. Thanks for your thoughts. Maybe keeping money journal is a good idea for me too. A fresh outlook and clean slate for starting out the new year makes sense too.

Great attitude, Laurie! Keep me posted on your money journal!

Smart young man! He listens to people! He takes what he hears and learns from it! Great stuff here! Your law students are lucky to have you as a money mentor!

Thank you, Jeff! Glad you enjoyed the first post!

This was a great read — thanks for sharing!

Thank you, Diana!

Matt What are your thoughts on index funds vs individual stocks ?

Great question! I invest in index funds and think that’s the best choice for many of us. We’ll have to revisit this topic in a future post. Stay tuned!