When it comes to investment decisions, we all want to make the right decisions. We work hard for our money and know that investing for the future is important.

We just don’t always know what the right decision is.

With so much marketing from big banks and investment companies, not to mention the financial media, the options can seem overwhelming.

Well, what if you decided to drown out the noise and take matters into your own hands?

What if the best thing to invest in was not a stock or a rental property?

What if the best thing to invest in was staring right back at you every time you look in the mirror?

Instead of spending your whole life investing in other companies and other people, what if you decided to invest in yourself?

For my money, there’s no better investment you’ll ever make.

We all invest in ourselves when we go to school.

Investing in yourself is something you’ve long done, even if you didn’t always realize it.

As a lawyer, doctor, consultant, etc., you’ve already made a major investment in yourself through your education.

Following high school, lawyers commit to another 7 years of education before they can start practicing. Doctors can take twice that long.

For consultants and other professionals, it’s not uncommon to return to school for an M.B.A., oftentimes while still working a full-time job.

All this education and training comes at a steep price. Most of us take on huge amounts of debt in exchange for our careers.

The point is that none of us are strangers to investing in ourselves. And, for the most part, we’ve all benefitted because we made major investments in ourselves.

The problem is that a certain point, we stopped investing in ourselves.

So, this leads us to the question of the day:

When was the last time you invested in yourself?

What are ways you can invest in yourself?

There is no shortage of ways to invest in yourself. Just as a few examples, you could:

When you invest in yourself, the cost of entry is very low.

Books are inexpensive. Blogs and podcasts typically offer free and timely content.

Even if you only learn one new idea or strategy from a book or blog post, the cost to learn that idea or strategy is basically zero.

This makes investing in yourself a near risk-free investment.

Let’s talk about the value in attending professional seminars for a minute.

Every professional field, in every corner of the world, offers seminars.

Law firms and businesses recognize the importance of seminars and will oftentimes pay the registration fee for its employees.

What happens when you attend seminars? Not only do you learn skills to help you excel in your career, you also meet people.

Meeting the right person can make your career. You just need to invest in yourself by registering for the seminar.

Online courses are an inexpensive and effective way to invest in yourself.

The same low cost and effective way to invest in yourself that applies to seminars also holds true for online courses.

There’s one crucial advantage to taking an online course:

If in-person seminars aren’t your thing, you can take an online course from the comfort of your home or office, at your own pace.

Many courses offer valuable insight based on the instructor’s personal experiences and acquired knowledge. This learning format can feel more intimate and relatable.

Additionally, online courses may provide the opportunity to meet the instructor and other participants. That gives you the chance to ask questions pertaining to your personal situation. You also get the advantage of building your network, like if you attended a seminar.

One last note about online courses: before you balk at the price, think back to what you paid for law school.

Law school costs hundreds of thousands of dollars. Many lawyers spend years in debt to pay off that education.

Now, compare what you paid to attend law school to the cost of completing an online course.

A quality online course will cost a fraction of what it cost to obtain your degree.

If you were willing to take out loans and pay hundreds of thousands of dollars to become a lawyer, why not invest a bit more in yourself to continue developing your skills?

Investing in yourself does not only relate to your career.

Investing in yourself is not limited to just acquiring skills or connections beneficial to your career.

As one example, I recently committed to running the New York City Marathon in 2026. I’ve never run a marathon before. I’ve never even run a half marathon before. I’m essentially clueless in how to properly train.

There are free articles and training plans for beginners and experienced runners. There is also a paid online course, which I plan to take in the coming weeks.

The thing is, if I’m going to take on the challenge and time commitment of training for a marathon, I want to do it the right way.

I want to learn from other people’s experiences. I don’t want to make preventable mistakes. I’m happy to pay for that knowledge and insight.

This logic applies whether you are training for a marathon or hoping to develop any other skill. Investing a little bit of money upfront can lead to massive benefits down the road.

Personal finance is one of the most important areas of self-improvement.

Investing in your physical wellness is important. Hardly anything could be more important.

You know what else is important to invest in?

Your financial wellness.

I’ll even go so far as to say that investing in your own financial wellness is the best investment you’ll ever make.

The potential rate of return for learning personal finance is greater than any other investment.

Whether you subscribe to a money blog, listen to podcasts, read books, or pay for an online course, the return on that investment is potentially infinite.

This especially holds true for anyone willing to pay hundreds of thousands of dollars for an education.

Paying another $1,500 to $2,000 for a quality financial wellness course ensures that the investment in your career will not be wasted.

To me, that makes it a no-brainer to invest in your financial wellness.

What’s the point in working so hard to make money if you’re not going to be knowledgeable or disciplined enough to keep it?

When you have money and understand personal finance, you control the circumstances.

When you empower yourself to make intentional choices with your money, something incredible happens.

You gain a new confidence as your walk through life.

You stop worrying endlessly about money.

Trust me, it’s a relief to know that all the money you’re earning at work is not being wasted.

The best part of investing in your financial wellness is that you’ll be on your way to financial independence.

That means the freedom to pursue work that is meaningful to you and the freedom to spend more time with people who are meaningful to you.

Today, I’ll walk you through my step-by-step guide to buy your first rental property.

If you can follow these steps (in order), you will be in great shape to acquire your first rental property.

And, if I can be of any assistance as you begin your search for a rental property, please feel free to connect via socials or by replying to one of my weekly emails.

You can sign up for my email list here. I personally respond to every email.

Step-by-Step Guide to Buy Your First Rental Property

Use common sense and your own life experience to develop your target criteria.

Pick an initial location that matches your criteria.

Learn the common, important attributes of properties in your area.

Study the average rent for units in that area.

Ballpark how much you’ll need to spend for an attractive property.

Work with a real estate broker to test your findings.

Contact a mortgage broker and determine your budget.

Return to your search and do basic deal analysis.

Start touring the properties that look good on paper.

Determine if the numbers will work in your area.

1. Use common sense and your own life experience to develop target criteria.

Don’t believe anyone who tells you he has a one-size-fits-all solution for evaluating properties. Every market is different. What works in Chicago won’t necessarily work in Los Angeles.

That said, there is certainly some advice that applies across the board.

For starters, regardless of what market you’re in, you can and should use common sense and your own life experiences to evaluate rental properties.

Don’t overcomplicate this part.

Before you do anything else, think about what you would personally want in a rental property.

Forget about complex formulas and deal metrics. We’ll get to the numbers soon enough.

Start with a basic question:

What would I want if I were a renter in this market?

Before anything else, write down a list of the most important features that you would want in an apartment. Then, use that list as a guide to finding the right kind of properties.

By the way, using your own common sense is one of the best parts about investing in real estate. You don’t need an advanced degree or a background in real estate.

We all have some idea of what makes a neighborhood a good place to live. The same goes for what makes an apartment a good apartment.

We may not always agree on what those things are, and that’s OK. It may be for a simple reason, like we are not targeting the same potential tenant pool.

The bottom line is you should absolutely use your common sense and life experiences to help formulate your investing strategy.

Ask yourself what you would want in an apartment. Don’t waste your time running the numbers on any property that doesn’t match your criteria.

2. Pick an initial location that matches your criteria.

There are potential investment properties in every part of the country. Before you start looking at individual properties, you first need to select an area you want to invest in.

Based on your own life experiences, you are probably already drawn towards certain parts of the country. You may even have a good sense for different neighborhoods within certain cities that match your general criteria.

From there, you should do some preliminary research online to confirm what you think you know about specific areas.

For example, I know through my own life experiences that many recent graduates from the Midwest move to Chicago after college. The question then becomes: where do these young professionals tend to live in Chicago?

To find out, I might Google something like “best coffee shops (or restaurants/bars/nightlife) in Chicago.”

Likewise, if you’re targeting families, you might search for “best schools” or “best parks.”

Performing this kind of basic research is how my wife and I stumbled upon the Logan Square neighborhood in Chicago.

The truth is that when we first started looking for rental properties in 2017, we knew very little about Logan Square, even though we both always lived in Chicago or the Chicagoland area.

3. Learn the common, important attributes of properties in your area.

Once you’ve picked an area to focus on, use an app like Redfin or Zillow to create a broad search for that area. You should filter your search based on the criteria you established above.

Take some time to casually study the listings in that area. At this point in the process, don’t worry about running the numbers. You’re still in learning mode.

If you study enough listings in a particular location, you’ll start to notice certain features that separate the premium properties from the mediocre properties.

For example, you may notice that the more attractive properties all have in-unit washer/dryer. Or, you may learn that the attractive properties all seem to have wood floors and stainless steel appliances.

Your goal is to understand the common and important property attributes in that area because those are the features potential tenants will expect to find.

Think of it like this: you don’t want to buy the only property on the block that doesn’t have in-unit washer/dryer. Even if you buy that property at a good price, you’ll struggle to find good tenants if the expectation is to have in-unit washer/dryer.

It’s not an exhaustive list, but here are some of the key attributes we’ve learned are important to young professionals renting in Chicago:

Location, location, location. Proximity to the L and social life (coffee shops, restaurants, bars, etc.) are crucial. Most of the young professionals we rent to are still in the “going out” phase of life. They want to live in fun neighborhoods so they can enjoy themselves when they’re not working. They typically stay in our apartments for 2-3 years, oftentimes before buying a place of their own and “settling down.”

Taxes. Property taxes can eat away your cash flow. We have high property taxes in Chicago across the board, but taxes vary widely from neighborhood to neighborhood. I look for properties in areas that have more attractive taxes.

Big bedrooms. One of the most common questions I get when I do apartment showings is, “Can I fit a king size bed in here?” People love big beds these days. This can be a challenge considering Chicago’s standard 25-foot wide lot. I look for properties with a minimum bedroom size of 10 x 10.

Outdoor space. Young professionals want to have outdoor space, even if they never use it. When I was a renter, I always wanted an apartment with a balcony for my grill. It didn’t matter to me that I only used it a handful of times each year. Maybe having outdoor space made me feel more grown up?

Parking. Even though Chicago is a very public transit-friendly city, people still like having cars. Because most young professionals aren’t using their cars every day, they want to keep it safe in a dedicated parking space.

When we shop for a rental property, we look for as many of these features as possible. We don’t expect to check every box because it’s nearly impossible to find a property that has all of these features (at least at a price that makes sense).

4. Study the average rent for units in that area.

Before you commit to a particular area, you need to know what kind of rent payments you might expect.

You can usually find rental information directly on the listing. You may see the actual rent for that property or the projected rent. For this part of the process, this estimate is good enough to get a basic sense of what you may be able to charge.

Word of caution: it’s not unheard of for these rental estimates to be exaggerated in the listings.

As you get to know your market better, you’ll know whether the projected rent is accurate. Plus, you’ll have a real estate broker on your team who can validate the numbers. More on that below.

Finally, studying the average rent goes hand in hand with the previous step of learning the important attributes of rental properties in your area.

For example, you may discover that a renovated 3 bed, 1 bath apartment with in-unit washer/dryer and a parking space rents for around $2,500. Similar units without parking may go for $2,300. Units that have not been updated may rent for $1,800.

Your mission is to differentiate between the property attributes that seem to increase the potential rent in your area from the attributes that don’t add much value.

For instance, we’ve learned that dedicated parking spots are important in Logan Square. However, renters don’t seem to care very much if the parking spot is in a garage or a parking pad.

For that reason, we don’t care too much whether a rental property has a garage, as long as there is dedicated parking available.

5. Ballpark how much you’ll need to spend for an attractive property.

By this point in the process, you’ll have a good idea of what constitutes an attractive property in your target area. You’ll also have a good idea of what these properties rent for.

Next, you can ballpark how much you’ll need to spend to purchase one of these attractive properties.

When I refer to attractive properties, I mean one that has most (but probably not all) of the features that you are looking for and still commands a decent rent. By “decent rent,” I mean not the absolute highest and also not the lowest for the area.

Additionally, the property should be priced reasonably for the market. That means it likely won’t be the most expensive property or the cheapest property.

The goal here is to have a general idea of how much good properties cost in your target area. With this information, you can then decide if it’s an area you want to target, or if you want to explore other locations.

One point that’s worth repeating: don’t expect to find a property that has every one of your key features. If you’re waiting on such a property to hit the market, you’re likely to be disappointed for one of two reasons.

First, you’ll likely end up overpaying for that property. If you overpay, you’ll struggle to earn cash flow. As investors, cash flow is crucial.

Or, you won’t ever buy a property because your expectations are too high. Investing in real estate is all about trade-offs. The fun part of the gig is deciding what trade-offs make sense.

Remember, you’re not searching for your picture-perfect, dream home. You’re searching for an asset that puts money in your pocket.

Now that you’ve educated yourself on your target market, it’s time to seek out the assistance of an experienced real estate broker.

A good broker will talk with you about what you’ve learned and offer additional guidance on your target market.

Also, a good broker will:

Send you properties that match your goals.

Tour properties with you to help identify any red flags.

Negotiate on your behalf to ensure you get the best possible price.

Connect you with other key members of your team.

Steer you away from making poor choices.

Don’t make the mistake of jumping right to this step without completing steps 1-5.

It’s important to have done your homework on your target market before talking to brokers. That’s because you need to know enough to have informed conversations with potential brokers.

You don’t have to know all the answers. But, you have to know enough to ask the right questions.

And, you have to know enough to recognize if your broker is giving you misguided advice.

Mortgage lending is big business. Just about every person out there needs a mortgage to buy a home or an investment property. As a result, there are a lot of banks and companies out there who want your business.

To be sure, not all mortgages are created equal.

And, not all brokers, banks, and lending companies are created equal.

That’s why your job as an investor is to find a mortgage broker who truly has your best interests in mind.

That means working with someone who wants what’s best for you and your family, not what’s best for him and his family.

Plus, because rental property investing is a long-term game, you want someone on your team who’s also in it for the long run.

A good mortgage broker will:

Recommend the best loan for your goals.

Stop you from borrowing more than you really can afford.

Help get your loan approved.

Explain the numbers.

Not let you refinance until the time is right.

In sum, a good mortgage broker understands exactly what you’re trying to accomplish with each purchase. You can be straight with him and he can be straight with you.

8. Return to your search and do basic deal analysis.

Now that you have a real estate broker and a mortgage broker on your team, you can start to analyze deals that match your criteria in your target area.

Don’t let this part of the process intimidate you.

Rest assured, you’ve already done the hard part of educating yourself on the key assumptions you’ll need to make to properly analyze deals.

Now, you just need to plug those numbers into a simple spreadsheet or online calculator.

For a step-by-step example on how to run the numbers, check out my post here.

9. Start touring the properties that look good on paper.

After running the preliminary numbers on properties that match your criteria, you should have a smaller list of properties that seem like real contenders.

These are the properties that you should tour.

Again, you want to make sure you don’t jump ahead to this step without having completed the other steps.

That’s because it’s impractical (if not impossible) to tour every property that appeared in your initial search. By running the numbers first, you can weed out the properties that would be a waste of time to see in person.

After touring a property, you should then update your preliminary analysis based on what you learned.

For example, maybe you learned that the bedrooms are smaller than advertised. Maybe the finishes aren’t as nice as in the pictures.

The point is that after seeing a property in person, you may determine that you previously overestimated what the unit will rent for.

You also will have a better idea of what you think the property is worth.

A final word here: some investors are content buying properties without touring them in person.

Personally, I would never buy a property without walking through it first. I want to see for myself what condition the property is in and make my own assessment of what it could rent for.

10. Determine if the numbers will work in your target area.

The final step is to put together everything that you learned in steps 1-9 to determine if it’s a good idea to invest in your target area.

If you like what you’ve learned, you can stay disciplined and wait until you find an attractive property to offer on.

On the other hand, you may find that your initial target area is not ripe for investment.

That’s OK. It’s certainly better to find that out before you commit hundreds of thousands of dollars to a poor investment.

Before my wife and I settled on Logan Square, we went through this process and ruled out a number of other promising neighborhoods.

By putting in the effort to complete steps 1-9, we learned that the math simply did not work in certain parts of the city.

In some neighborhoods, the properties were just too expensive to earn positive cash flow. Then, in other areas, the rent was not high enough to justify the purchase price or high taxes.

In the end, we determined that Logan Square had the right combination of attractive properties and decent rents.

Step-by-Step Guide to Buy Your First Rental Property

Use common sense and your own life experience to develop your target criteria.

Pick an initial location that matches your criteria.

Learn the common, important attributes of properties in your area.

Study the average rent for units in that area.

Ballpark how much you’ll need to spend for an attractive property.

Work with a real estate broker to test your findings.

Contact a mortgage broker and determine your budget.

Return to your search and do basic deal analysis.

Start touring the properties that look good on paper.

Determine if the numbers will work in your area.

Like any new skill in life, implementing this step-by-step guide takes some time and effort in the beginning.

The upshot is that if you can follow these steps, you’ll get that first rental property and have the skills to acquire additional properties when you’re ready.

If I can be of any assistance as you begin your search for a rental property, please feel free to connect via socials or by replying to one of my weekly emails.

You can sign up for my email list here. I personally respond to every email.

When I graduated law school in 2009, I never thought about money.

Within a year, I had racked up $20,000 in credit card debt ($30,000 in today’s dollars).

And, that was on top of my student loan debt.

My salary at the time was $62,000. This was a problem.

After all these years, I still ask myself, “How did I let that happen?”

The answer, I now realize, is actually pretty simple.

I never learned about personal finance.

I wasn’t thinking about money. And, I certainly wasn’t talking about money.

It wasn’t until later that I learned that I had made every common money mistake in the book.

Rented a fancy apartment with a garage parking spot that I didn’t need?

Paid for Cubs season tickets I couldn’t afford?

Traveled coast-to-coast? Traveled overseas? Put it all on credit cards?

Check… check.. and check.

It’s not that I intentionally decided to get into debt. Frankly, there was nothing unusual about me at all.

I generally wanted to make good choices. I am a relatively smart human. You are, too. You’re reading a personal finance blog with the entire internet at your fingertips.

I didn’t know the first thing about money when I began my career.

When I graduate law school, I blindly assumed that I would earn a high enough income that I didn’t have to worry about money.

As I fell deeper and deeper into debt, I realized what a huge mistake that was.

Maybe that’s why I still remember the day so clearly when I realized I was financially heading in the wrong direction.

It was an ordinary Monday. I had grabbed my mail on the way out the door as I headed to my job at the courthouse. When I got to my desk, I opened my credit card statement and was stunned by what I saw.

$20,000 owed ($30,000 in today’s dollars) one year into my career.

I was ashamed. I was supposed to be smart. Responsible. Trustworthy.

Looking back, I shouldn’t have been so hard on myself. I had never learned about personal finances.

It would be like getting upset today that I’m bad at playing the piano when I never learned how to play in the first place.

I’m certain that if I taken a personal finance course, or read a personal finance blog, I wouldn’t have made the same mistakes.

I would have saved myself a lot of worry, frustration, and time if I had a basic personal finance education.

I also would have learned that so many others were struggling with consumer debt like I was. There was no reason to make it harder on myself by keeping my debt a secret and struggling alone.

I unnecessarily did it the hard way, but I figured out personal finance.

At that moment when the full weight of my debt hit me, I made it a priority to turn things around.

At the time, I didn’t know the solution.

But, I had been trained to do research in law school so I could find answers to hard questions. So, that’s what I did.

Along the way, I realized that the fundamental and basic personal finance principles are, well, basic.

George S. Clason wrote “The Richest Man in Babylon” nearly a century ago. His collection of parables set in ancient Babylon is legendary.

Everyone should read it. His advice is simple and excellent: spend less than you earn. Save. Invest.

The same fundamentals are as true today as they were then.

Personal finance education should be a constant in your life.

Money is about continuous mindset and choices.

The basic concepts are easy enough to understand. Consistently making good choices is hard.

Even as I was racking up credit card debt, I could have aced a quiz that asked, “Is it a good idea to spend more money than you earn every month and plummet deeper and deeper into debt?”

I knew that I was supposed to spend less than I earned. That didn’t stop me from overspending.

Knowing the right answer is not the same as actually doing the right thing.

The law students and lawyers I teach are smart people. Like me back in 2010, they generally know the right answers. They don’t need me to tell them to spend less than they earn.

I help them get to the next level by building a strong money mindset. Then, we work on the habits and skills that will allow them to consistently use money as a tool to control their circumstances.

It’s not enough to learn the basics of personal finance and then stop. As your life changes, you need to regularly evaluate your personal finances so your money stays in line with your values.

That’s why it’s important to make personal finance education a constant in your life, whether it’s through a blog, a course or coaching.

Too many of us choose to struggle with money alone.

For some reason, though, most of us choose to deal with money on our own. Alone, we struggle with anxiety about credit card debt and guilt about splurging on things we love.

This has never made sense to me.

Making good choices with our money is essential to a healthy and meaningful life.

Why don’t we talk more about these things with our friends and family?

That’s what I’m trying to change.

I’m done with this stigma that we shouldn’t talk about money.

I want us to get comfortable with the idea of going to our friends and loved ones to talk about money, just as we would talk about anything else.

There should be no embarrassment or shame in it. We’re all dealing with the same challenges.

By talking about money, we can help each other turn those challenges into opportunities.

If we can alleviate our money stress, perhaps we can reverse the trend of lower happiness levels among young people today.

Talking about money is not about numbers.

We’ll have plenty more to say about how to talk money. For now, let’s agree that talking about money is not about prying into how many dollars we each have in the bank.

We can benefit by talking about our money mindset, habits, and strategies, while still keeping certain information private.

Let’s also agree that talking money is a “no judgment” endeavor.

We have all had different experiences that have shaped our relationship with money.

It’s important not to pass judgment, especially when talking to our significant others. Your conversation won’t last very long if you ignore this advice.

Each session I’m with my students, I learn from their experiences and money mindset, same as they learn from mine. I encourage them to continue the conversation outside the classroom with their loves ones.

When my students report back, they tell me how empowered they felt after starting these conversations. The more we can talk money, the less we’ll feel alone. We’ll all make better choices because of it.

People tend to skip this step. They want to jump straight to investing and real estate before learning about money mindset.

But, why focus on investing if you and your significant other are not aligned on what those investments are for?

The same logic applies to budgeting. While very few people enjoy the budgeting process, it’s a crucial step to generate fuel for our savings and investments, which ultimately fund our major life goals.

When I teach my personal finance seminar to lawyers or law students, I typically reach out ahead of time asking about topics of interest.

The most common response I get is something like, “I want to learn about investing.”

The other common response is, “I want to invest in real estate.”

I totally get it. Investing in the stock market and owning real estate are sexy topics.

Without a doubt, these are both important topics to cover in a personal finance seminar. We spend a lot of time in my course and here in the blog talking about investing and owning real estate.

Of course, the best way to generate wealth is through consistent investments over a long time horizon.

So, my students are asking the right questions when they are concerned about investing and real estate.

The hard part is constantly generating enough money to fuel those investments.

That’s why investing and owning real estate are “Day 2 topics.” On Day 1, we have to build the foundation.

Think about it like this:

Before we can invest, we need excess money to invest.

To have excess money to invest, we need a budget that actually works.

For a budget that actually works, we need clear motivations.

Clear motivations means a strong money mindset.

Can you spot the issue of investing without a solid foundation?

When my students ask me a question about how to start investing, I tend to respond with a question of my own:

“How much savings does your budget generate each month?”

Yes, I know. It’s so annoying to answer a question with a question.

This particular question usually leads to a double dose of annoyance from my students.

My students are first annoyed that I ignored their question about investing. They didn’t come to me to talk about something boring, like budgeting.

They want to know about the exciting stuff, like earning huge returns in the stock market.

Next, after this initial annoyance fades away, another form of annoyance sets in.

My students get annoyed because they can’t actually answer the question.

They realize they have no idea how much money they’re saving each month because they don’t have a budget.

That’s a problem.

Not having a budget is a problem for anyone who wants to consistently invest.

To be a successful investor, you need to consistently fuel your investments. There will be ups and downs in the markets. That’s to be expected.

Your job is to stay in the game and keep feeding your accounts.

For example, most of us can be successful investors by simply investing in an index fund, like VTSAX.

Once we’ve selected that investment, our job is to constantly add money to your investment account.

That means having a budget that works.

If you skip this part of the process, sure, you may be savvy enough to open and initially fund the account. But, my prediction is you won’t be fueling that account regularly.

Having a budget for your personal finances is even more important when it comes to owning real estate.

Investing in real estate means running a business. Money comes in and money goes out. To be successful, you have to make sure that more money comes in than goes out.

This is obvious stuff, right?

The same logic applies to your personal budget: if you want to get ahead in life, more money needs to come in than goes out.

The problem is most people have a hard enough time managing their personal finances. How are they going to handle managing business finances?

That’s why I ask my students, “If you haven’t mastered this idea with your personal budget, are you sure you want to take on the stress and risk of an investment property?”

It’s usually around this point when my students start nodding in understanding.

Before focusing on stocks or real estate, make sure your personal finances are in order.

My goal here is not to dissuade you from investing in stocks or real estate.

We all need to invest if we want to generate wealth.

My goal is to help you avoid the mistakes that so many of us make in the early stages of our careers.

One of the biggest mistakes I see is people wanting to jump to the final steps in the process without starting from a strong foundation.

If you’ve been following along on the blog, you likely noticed the progression in topics we’ve covered. This is the same progression that we follow in my personal finance course.

You’ll see links to each one of these topics featured on the top of the Think and Talk Money homepage:

We initially covered each of those topics in order from top to bottom. First, we talked extensively about the mental side of money. Without having your money mindset in the right place, nothing else matters.

We then spent a lot of time talking about personal finance fundamentals, like budgeting, saving, and handling credit and debt responsibly.

Only after having our personal finance foundation in place did we talk about more fun concepts like investing and real estate.

There’s a reason we’ve covered these topics in this order.

If your money mindset is not in the right place, you won’t be able to stay on budget.

If you can’t stay on budget, you’ll likely fall into debt.

When you’re falling deeper and deeper into debt, it doesn’t make a lot of sense to prioritize investing.

Why bother with investing if any profits are just going to disappear?

Let’s focus on that last point for a minute.

What sense does it make to invest if you’ve never proven to yourself that you can use those investment gains responsibly?

I never want to see people take on the risks of investing just to have any profits disappear because they don’t have a strong personal finance foundation in place.

For example, imagine someone does the work to find and sustain a good rental property that generates $1,000 per month in cash flow.

It’s not easy to earn that much. It takes time and effort, not to mention the risk involved.

If that same person blows the $1,000 he earned on things he doesn’t care about, what was the point?

Why take on the risk and do the work if the money will all be gone by the end of the month?

Unfortunately, this is how many people go through life. They work hard, make good money, and then have nothing to show for it.

I don’t want that to be your fate. I want you to have a plan for your money before you earn it.

That means sticking to a budget that consistently moves you closer to living freely on your terms.

Most of us don’t know where our next dollar is going.

The reason most people never get ahead with their finances is because they don’t have a plan for where their next dollar is going.

Their income hits their checking account, they spend it on this or that, and pretty soon that money has disappeared. They haven’t used the money to advance any of their priorities.

It’s just gone.

To me, this is one of the most important money mistakes that we need to fix right away. We definitely need to fix it before we start fantasizing about big investment returns.

If not, you’ll just be making the same mistakes, just with more money to lose.

Having a plan for our money, before we earn it, is essential if we want to reach our goals. With a plan, we can eliminate the disappearing dollars with confidence that our money is being used to serve our purposes.

How do you create a plan for your money before you earn it?

You need to have a budget.

If you don’t currently have a budget that results in excess money at the end of each month, I encourage you to start there before thinking bout real estate.

When you have strong fundamentals in place, money becomes fun.

Being good with money doesn’t have to be stressful. Once you have the fundamentals in place, you’ll start to see how each dollar you earn gets you one step closer to financial freedom.

Before you think about investing in stocks or in real estate, make sure that your personal finances are in order.

Otherwise, the effort, stress, and risk of investing is not worth it. Any dollar you earn is likely to disappear as quickly as it comes in.

To prevent that from happening, establish good money habits before you buy real estate.

In the end, you’ll be so happy that you did.

For any investors out there, did you jump in before establishing strong personal money habits first?

Did any benefits you earned from investing simply disappear because you didn’t have a plan for those dollars ahead of time?

What advice do you have for beginners thinking about investing?

I just wrapped up another personal finance seminar with a great group of law students. After two full days of leading class, my voice is hoarse and my body is sore.

If you’re interested in learning more about my personal finance course for law students and young lawyers, please reach out.

I’ve taught law students and lawyers, both in-person and virtually, and would be happy to discuss how I can help you or your group.

My favorite part of class is when my students share their Tiara Goals.

We spent the first portion of class talking about money mindset. Without the right motivations, none of the other tools matter.

Without a doubt, this is always my favorite part of class.

When I say I’m on a mission to convince you that talking money is not taboo, I think of my students sharing their goals.

I get so energized by hearing their goals. My students report the same sentiment after learning what drives their friends and peers.

Over the years, my students have shared countless impactful stories. As unique as these goals can be, it’s remarkable how most of us want the same things in life.

Year after year, I hear the same motivating forces:

Spend more time with my family.

Travel and enjoy experiences around the world.

Stay healthy and fit.

Provide for my children and my aging parents.

Work for a cause I believe in.

Have time to volunteer.

Enjoy more hobbies like baking, golf, jogging, sewing, and pickleball.

I also regularly hear one thing that my students, and the rest of us, don’t want:

I don’t want to be stressed about money.

Isn’t it telling that year after year, most of us want the same things in life?

Be specific, but not too specific, when you think about financial freedom.

When we talk about what we do with financial freedom in class, I encourage my students to get specific without being so precise that the goal becomes restrictive.

When we’re thinking about goals related to financial freedom, the idea is to focus more on big-picture, core values.

There will be a time and a place to strategize how to get there. The point here is to help define what you’re even trying to get in the first place.

For example, instead of “spending more time with family,” I would suggest something like, “never miss my child’s soccer game or dance recital because of work.”

Instead of “travel around the world,” I would suggest “at least one overseas trip of at least 2 weeks per year.”

Adding that little bit of specificity will help you visualize what you’re striving for with your money decisions.

Don’t get discouraged if you think you are not close to financial freedom.

Even when you feel like financial freedom is only a distant dream for you, it’s important to actively think about what you want out of life.

I’d even suggest that the further away you feel from financial freedom, the more important it is to think about what it would mean for you.

When you’re at your lowest point, visualizing what you would do with financial freedom is a helpful escape.

If you haven’t ever actively thought about what you would do with financial freedom, hopefully hearing about what my students shared in class will encourage you to do so.

Don’t forget to write down whatever you come up with.

I suggest you share your version of Tiara Goals with your friends and loved ones. It’s OK to keep some of your goals private.

By sharing, you will get the benefit of them cheering you on. You’ll also hopefully encourage them to share their goals with you, which can be very inspiring.

Budgeting is all about generating fuel for your ultimate goals in life.

Following our chat about money mindset, we launched into budgeting.

The essential purpose of making a budget is to generate fuel for your ultimate goals in life. This fuel is what feeds your savings, pays off debt, and grows your investments.

It’s not easy to track every penny. It’s not enjoyable to realize that your dollars are disappearing on stuff you don’t care about. But, these are crucial steps on the way to financial independence.

Learning how to create a budget that you’ll actually stick to is so important that we practiced implementing a Budget After Thinking in class.

Debt and credit are essential parts of a healthy financial life.

After focusing on the fundamentals of budgeting, we moved on to debt and credit.

Most of us have (or will have) some form of debt, whether it’s credit card debt, student loan debt, or mortgage debt.

With the right tools, we can attack that debt and eliminate it as quickly as possible.

Just as important, we can appreciate how we got into debt in the first place so we don’t make the same mistakes again.

When we talked about credit in class, we emphasized that credit impacts our largest purchases in life, like buying a home or a car. For that reason, it’s essential to understand how our credit history impacts our credit score.

From there, we explored why credit cards are a privilege.

I am a big fan of using credit cards responsibly to earn free travel. If you don’t overspend and pay your bills in full every month, credit cards can be a useful tool.

Student loans are front of mind for most law students and young lawyers.

Of course, no personal finance seminar geared towards law students and young lawyers would be complete without addressing student loans.

This year, we focused on the changes to federal student loans. We learned how to navigate paying back loans while advancing some other important financial goals, like investing.

Following our conversation on student loans, it was time to talk about building wealth through investing.

When it comes to investing, the key is to let compound interest work its magic.

With time on your side, you can concentrate on low fees, the proper asset allocation, and consistently fueling your investments.

Using an online calculator, we saw how even seemingly small contributions to our investments will make a huge difference over the long run.

This point demonstrates why we begin with budgeting before we talk about investing. Remember, one of the main purposes of your budget is to create money for your investments.

Every dollar that you invest rather than spend early in your career will lead to massive wealth if given enough time.

Finally, we discussed real estate, a topic that I am very passionate about.

We learned how to analyze when the time is right to buy a home (and when not to buy a home). We then saw how having a strong money foundation is key to qualifying for the best mortgages.

From there, we moved on to real estate investing. With real estate, investors benefit from cash flow, appreciation, debt pay down, and tax breaks.

For people pursuing financial independence, there may not be a more powerful strategy than buying a small multifamily property, living in one of the units, and renting out the others. This strategy is known in some circles as “house hacking.”

With this one decision, you can eliminate your housing costs entirely, which is traditionally the largest expense in our budgets.

That means you can repurpose the money you had been spending on housing to other goals, like paying off student loan debt.

At the same time, you have a long-term asset that you can keep for years after you decide to move out. That asset can kick off monthly cash flow, which can be saved for other investments or used to pay for current living expenses.

Money is nothing more than a tool.

In the end, I encouraged my students to recognize that money is nothing more than a tool that can be used to build a life on our terms.

When we learn how to use money in this way, we control the circumstances. The circumstances don’t control us.

Being good with money involves consistent choices. I can’t make those choices for you, but I can give you the tools to properly think through and evaluate whatever dilemma you face.

I left my students with one final request: keep the conversation going with your loved ones and friends.

Talking about money is not taboo. We can all learn so much from each other if we are just willing to share and listen.

There’s no reason to struggle with money decisions alone.

Our journeys towards financial independence should not be solo missions.

We can achieve financial wellness together.

All we need to do is think and talk about money.

If you’re interested in learning more about my personal finance course for law students and young lawyers, please reach out.

I’ve taught law students and lawyers, both in-person and virtually, and would be happy to discuss how I can help you or your group.

Have you ever asked yourself what you would do with financial freedom?

I asked myself that powerful question on a beach years ago and came up with my Tiara Goals.

Debt is a major obstacle on the way to financial freedom. To help you stay motivated to eliminate debt, write down your version of Tiara Goals.

By reminding yourself what you’re actually striving for, you’re more likely to stay on track.

Whenever we talk about good money habits, it always starts with establishing strong motivations. This is especially true when it comes to debt. There are too many temptations that can push us off track.

When you’re faced with these inevitable temptations, take a look at your Tiara Goals. I keep my Tiara Goals in my notes section on my phone. I also have a picture on my phone of the original sheet of notebook paper I scribbled on.

All it takes is a quick glance at my most important life values to overcome whatever temptation is in front of me.

Getting out of debt is not easy. Make it easier by regularly reminding yourself what you would do with financial freedom.

If you’re currently in debt, it’s crucial that you stop that debt from getting larger.

Think about it. If you’re paying off $1,000 of credit card debt each month, but you’re still spending $1,200 more than you earn, your efforts will be for nothing.

Your debt is growing faster than you’re paying it off. You’re not getting any closer to being debt-free.

Once you’ve stopped the disappearing dollars and learned where your money is going each month, you can make thoughtful decisions to pay off debt on a budget.

Then, you can be confident that any money you allocate to debt will actually lower your debt balance.

3. Prioritize Later Money funds to pay off debt.

The art of budgeting is to generate fuel for your Later Money goals. The more fuel you can generate each month, the faster you will achieve your personal finance goals.

There are lots of options on what to do with your Later Money. For example, you can invest in real estate or the stock market.

When you’re in debt, I recommend you prioritize using your Later Money to eliminate that debt. This is especially true if you have Bad Debt, like credit card debt. Your number one money focus needs to be to eliminate that debt.

This is the key to learning how to pay off debt on a budget.

There’s a good reason to focus on paying off your Bad Debt.

The interest rate on Bad Debt is generally very high. The amount you pay in interest each month will be significantly greater than what you may reasonably expect to earn through investments.

If you only have Good Debt, like student loan debt, you have some more flexibility in whether to focus on that debt or your other investment goals.

This is because Good Debt generally carries lower interest rates, so your investment returns may match or even exceed what you’re paying in interest.

In this scenario, I suggest that you consider splitting your Later Money between debt pay down, savings, and investments. This is what my wife and I are currently doing in 2025.

Seeing your savings and investments grow while focusing on how to pay off debt on a budget can provide an emotional lift.

Establishing good savings and investment habits now will also have longterm benefits that should survive your debt phase.

Our Top 10 Strategies for staying on budget will help you generate more money to allocate to debt. These tips are crucial if you’re trying to learn how to pay off debt on a budget.

For example, when you see something that you might want to buy, make a note in your phone instead of buying it right away. After a couple weeks, you probably won’t even want that thing anymore. Take that money you didn’t spend and put it towards your debt.

As another example, how about playing The $500 Challenge Game? When you come in under budget that month, use the excess funds to pay down debt.

You’ll see for yourself that the emotional high of paying down debt is better than the feeling you’d get from spending that money on things you don’t care about. It’s important not to ignore these emotional wins when learning how to pay off debt on a budget.

5. Talk to your people about how to pay off debt on a budget.

Talking money is not taboo. That includes talking about our current money goals and money challenges. Of course, it includes talking about how to pay off debt on a budget.

What are your current money priorities? If you don’t want to share with us, are you sharing with your friends or family?

I struggled with debt when I began my career as a lawyer. For years, I kept that to myself. I wish I had been more open. I’ve recently learned that many of my friends were struggling in the same way.

The problem was that none of us talked about it.

I think about how much stress we could have saved each other if we were just willing to talk about money like we talked about everything else. Instead, we hid our truths from each other.

Even worse, we likely enabled each other’s poor spending habits.

I now know that it didn’t have to be that way. I would have been better off if I was open about it.

This part still bothers me today: I also might have helped my friends facing the same challenges just by starting the conversation.

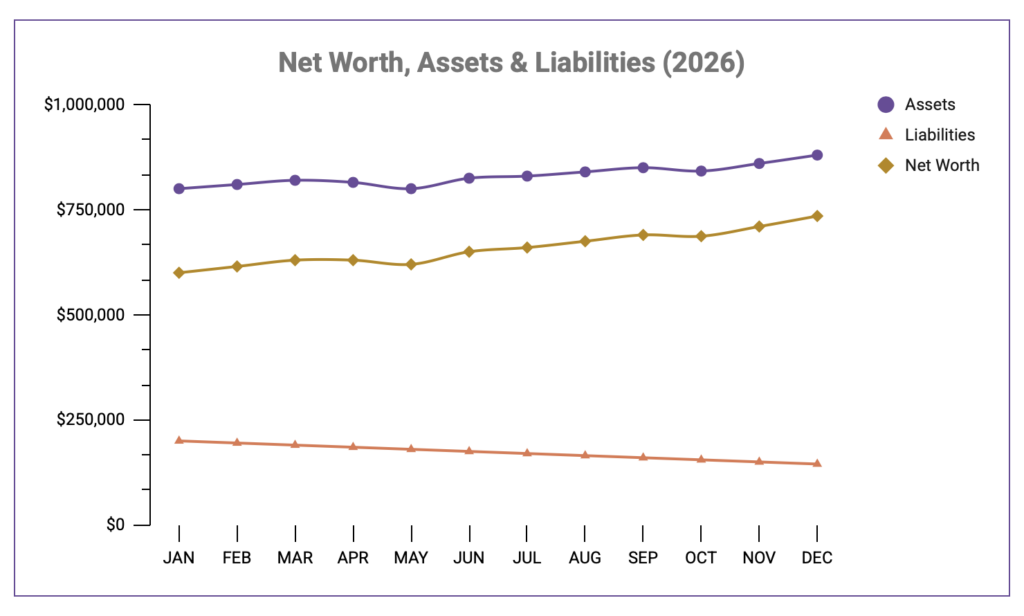

6. Track your net worth and savings rate for small wins.

Remember that your net worth grows when you reduce your liabilities, meaning debt.

When we think of net worth, it’s common to focus on growing our assets. Don’t forget that reducing your debts has the same impact on your balance sheet.

For example, when tracking your net worth, eliminating $1,000 in debt is the same as an investment that grows by $1,000.

Even when you’re focused on how to pay off debt on a budget, tracking your net worth can be very motivating. Every payment you make to reduce that debt improves your net worth.

This is especially helpful if you are focused on paying off student loans or paying down a mortgage. You may not have many appreciating assets, but you can still make a positive impact on your net worth by reducing your debt.

The same logic applies to tracking your saving rate. Measure and feel good about each additional amount you dedicate to eliminating debt.

The goal is to stay motivated while you pay off debt on a budget.

There are two common strategies to consider when you hope to pay off debt on a budget. These strategies are referred to as “Debt Snowball” and “Debt Avalanche.”

Debt Snowball means paying down your smallest debt balance first, regardless of interest rate. When you’ve paid off that loan completely, you then move to the next smallest balance, again regardless of interest rate.

Debt Snowball is ideal for people that are motivated by the emotional wins that come with eliminating a loan completely, even if it costs more money in interest in the long run.

Debt Avalanche means you pay down the debt that has the highest interest rate first, regardless of the balance. Once that debt is gone, you move to the loan with the next highest interest rate.

Debt Avalanche is for people who would prefer to pay less overall interest, even if it will take longer to pay off a single loan and receive the emotional win.

I discussed the pros and cons of each strategy here. Some people will prefer the emotional wins of the Debt Snowball method, while others will prefer the mathematical advantage of the Debt Avalanche method.

I’ve experienced firsthand that our money choices have more to do with emotions than they do math. If you prefer to play it strictly by the numbers, I completely understand.

The key is that whichever strategy you pick, stick with it. You’ll save yourself a lot of unnecessary mental gymnastics by choosing one approach and then moving on.

One word of caution: whichever method you choose, be sure to always pay the minimum on all of your loans. Otherwise, you’ll be in violation of your loan terms and face devastating penalties.

The idea with either of these methods is to allocate whatever funds remain to the single loan you have prioritized after paying the minimum on all loans first.

8. Think about loan consolidation or balance transfers.

Whether you have credit card debt, student loan debt, or even mortgage debt, you may have the option to consolidate each type of loan into a single loan.

If you do your homework, you should end up with a lower overall interest rate and have only one loan payment to make each month.

If you choose to go this route, make sure you fully understand the fine print involved.

For example, if you’re thinking about consolidating your student loans, you’ll end up sacrificing certain loan forgiveness provisions that accompany federal loans.

The same caveat applies when considering a credit card balance transfer.

A balance transfer is when you move the balance from one credit card to a different credit card with a lower interest rate. Most major credit cards accept balance transfers from other banks’ credit cards.

The main reason to consider a balance transfer is if the card you are transferring into carries a significantly lower interest rate than your current card.

In some instances, you may even qualify for a promotional rate with no interest charged for a limited period of time.

I used balance transfers when I was focused on eliminating credit card debt at the beginning of my career. I did my homework and found a card that was advertising 0% interest for 12 months with no balance transfer fees.

That meant that for an entire year, I paid no interest. Every payment I made went directly to lowering my overall debt.

If you’re considering a balance transfer, be mindful that there are usually upfront fees involved, usually around 3%. That fee may end up cancelling out any benefit from doing the transfer in the first place.

9. Get a side hustle to help pay off debt on a budget.

You’re not too busy or too important for a side hustle.

At the end of the day, there are really only two ways to more quickly pay off debt on a budget: spend less money and/or make more money.

We already talked about creating a Budget After Thinking to help on the spending side.

If you still believe that your income is the reason you have debt, there are always ways to improve your income.

Of course, if you really want to get rid of your debt faster, earning more money and the same time you’re spending less money is a dominate combination.

If you take on a side hustle, you can use every dollar you earn to pay off debt. Since this is new money you’re earning, you shouldn’t need it to fund your Now Money or Life Money.

Avoid the temptation of using that money on things you don’t really want anyways. Think about how much faster that debt will disappear if you’re able to throw additional money at it each month.

If you’re not ready for a side hustle, the same logic applies anytime you earn a bonus or commission at your primary job. Put that money to good use by paying down your debt.

10. Don’t let yourself fall backwards while you pay off debt on a budget.

When you do succeed in eliminating a debt, don’t let yourself fall back into bad habits. It’s hard to pay off a debt. It takes time. It takes patience and discipline.

Don’t let it all be for nothing.

When you pay off a loan, celebrate that accomplishment!

Be proud of yourself and let that good feeling motivate you to continue on your journey towards financial freedom.

Before you know it, debt will be part of your past life. You can shift all your attention to the opportunities that comes next for you and your family.

Top 10 Tips to Pay Off Debt for Lawyers and Professionals

To recap, here are my top 10 tips for lawyers and professionals to pay off debt:

If you have credit card debt, your immediate financial goal should be to pay off that debt as quickly and efficiently as possible. To get you started, I’ll show you exactly how to make a budget to pay off debt.

On your journey to financial freedom, getting rid of credit debt is crucial.

It is nearly impossible to get ahead financially if you are paying 20% interest or more on credit card debt. That type of drag on your money is just too strong.

Think about it: the stock market has historically averaged a 10% annual rate of return.

Does it make any sense to prioritize investing in the stock market to earn 10% per year if, at the same time, you are paying 20% in interest on your credit card debt?

Each year you follow this pattern, you are losing more and more money.

So, the first thing you should do is come up with a plan to pay off your credit card debt. Once the debt is gone, use that money for investments.

Today, we’ll look at how to make a budget to pay off debt so you can begin fueling your investments.

If you can follow these three steps, you’ll have a budgeting framework in place that will serve you well, long after you’re out of debt.

Paying off debt is the hard part. If you can do it, you’ll soon realize that it is a lot more fun to see your money grow each month instead of only seeing your debt shrink.

Let’s dive in.

Making a budget to pay off debt is about having a plan ahead of time.

The art of budgeting is to know what you want to do with your money before it hits your checking account.

Otherwise, it’s too late. Those dollars will disappear.

How do you come up with a plan, or budget, to pay off debt?

I teach my students that to create a budget to pay off debt, you need to first study your own personal situation to figure out where your dollars are currently going.

Then, you can figure out a plan for how to use your next dollar before you earn it. This applies not just to bonuses or other unexpected dollars, it applies to every dollar you earn.

When you put the time in to study your own habits, you can then create a realistic budget. When you have a realistic budget, you will have confidence that your dollars are working for you.

Some dollars will be used to pay your ordinary life expenses, some dollars will be used for all the things in life you love, and some dollars will go to your financial goals, like paying off debt.

That’s all there is to it.

If you don’t currently maintain a budget, here are three steps to follow to get you started.

Step 1: Track your spending for at least 3 months.

I recommend everyone, regardless of where you are in life, start with this first step of tracking your spending for at least three months.

Without knowing where your money is currently going, you won’t be able to make adjustments so you can pay off debt faster.

In other words, before you can reduce your debt, you have to make sure your debt is not growing each month.

That means not spending more than you can afford to pay off each month.

That’s a problem if you’re hoping to make a budget to pay off debt.

To address that problem, you need to track every penny for at least three months. Then, you’ll know exactly how much you’re spending and can begin to think about areas of improvement.

So, before you go any further in the budgeting process, you need to commit yourself to tracking every penny for three months and only charging what you can afford to pay off.

Fair warning, you probably won’t enjoy this part of the budgeting process.

Tracking your spending is important even if it’s not enjoyable.

I won’t lie to you.

This step can be hard and you probably won’t like it. This is the step that makes people think budgeting is a nasty word.

I get it and don’t blame you for having that reaction.

Still, there’s no getting around this first step. You don’t have to budget forever, just long enough to learn your own behaviors towards money.

Please know that many of us struggle with this first step. You might not like what you learn by tracking your spending.

When I first started budgeting, I learned that I was $20,000.00 in debt and was spending way more than I earned.

That wasn’t fun, but I’m happy that I put in the effort to find my blindspots and make adjustments.

I often think to myself, “Where would I be today if I didn’t go through this process 15 years ago? How much further into debt would I have fallen?”

The good news is, tracking your spending is easier today than it’s ever been. I’ve used apps, spreadsheets, and even the notes function on my phone.

Regardless of how you track your spending, be honest with yourself. If you intentionally or mistakenly leave out certain expenditures, you won’t learn where your money is actually going.

A budget, which is just a plan, is only as good as the data it’s built off of. Be honest about your data.

Last note: Budgets are usually done monthly, so you’ll want to create a separate accounting for each month you tracked.

The reason we track three months of spending is so you’ll be able to identify any patterns or inconsistencies in your spending from month-to-month.

This helps ensure you’re making decisions based off the best data possible.

Step 2: Separate your spending into three three main categories.

Great work completing the first step! That wasn’t easy, but you did it.

Now that you have tracked your spending for three months, you can assign each expense into separate categories.

Most personal finance experts agree, though we have different names for each category, that you should divide your money into three main buckets.

I refer to these buckets as:

Now Money

Life Money

Later Money

1. Now Money

Now Money is what you need to pay for basic life expenses.

These expenses include housing, transportation, groceries, utilities (like internet and electricity), household goods (like toilet paper), and insurance.

These are expenses that you can’t avoid and should be relatively fixed each month.

If you’re making a budget to pay off debt, it’s going to be hard to cut from this category, unless you are willing to make major changes. That means moving to a less expensive home or giving up your car, which are not always feasible.

That said, if you are in the position to make these kinds of big changes resulting in serious savings, you can accelerate your path towards being debt-free.

2. Life Money

Life Money is what you are going to spend every month on things and experiences in life that you love.

This bucket includes dining out, concerts, vacations, subscriptions, gifts, and anything else that brings you joy.

We can’t be afraid to spend this money. This bucket is usually what makes life fun and exciting.

The key is to think and talk so you are spending this money consistently on things that matter to you.

If you are truly dedicated to paying off debt, this is the major category to focus on. If it costs $100 to go out to eat, and $10 to eat dinner at home, that’s $90 that could potentially go towards paying off debt.

When you repeat that decision over and over, you can aggressively attack your debt.

3. Later Money

Later Money is what you are saving, investing, or using to pay off debt.

This bucket includes long term goals, such as retirement plan contributions (like a 401k or Roth IRA), college savings for your kids (like a 529 plan), emergency savings and paying off student loan or credit card debt.

This bucket also includes any shorter term goals, like saving for a wedding or a downpayment for a house.

Most fun of all, this bucket includes any investments you make to more quickly grow your wealth, like investing in real estate or the stock market.

You’ve probably guessed it already. Later Money is the key category that fuels your ultimate life goals, like financial independence.

The more you fuel this category, the faster you can reach your goals.

When your goal is to pay off credit card debt, any fuel you generate in this bucket should go to paying off that debt.

With the exception of contributing enough to receive your company’s 401(k) match and creating a small emergency savings account, all excess money should go towards paying off your credit card debt.

Don’t worry about assigning a percentage to each category.

I have intentionally not recommended target amounts or percentages to allocate to each of your three categories.

The reason is because of what I’ve learned from my students over the years. I’ll lay out my full reasoning in a separate post.

The short version is that in my experience working with law students, assigning target percentages for each category is counterproductive.

When I used to teach my students to aim for certain percentages in each category, I could tell that they would get discouraged as soon as I put the numbers on the slideshow. I completely understand why.

Each of us is starting in a different place. If you are currently spending 80% of your monthly income on Now Money, it’s not helpful to have someone tell you to create a budget that automatically drops that level to 50%.

My students would tune me out as soon as I put those numbers on the board.

Now, I teach my students to think and talk about their current personal realities and aim for steady and lasting improvements.

I want my students to create a plan that will last, not an unrealistic plan that they give up on after a few months.

So, whatever amount you’re currently spending in each bucket, that’s what we’re going to work with as we move on to step 3.

One other thing before you move on to step 3: don’t get hung up stressing about what type of expense goes into each category.

Sometimes, it gets tricky. Do clothes you buy for work count as Now Money or Life Money?

Don’t stress. It doesn’t really matter. It’s not worth the mental energy thinking about it. Just stay consistent and move on.

If you still want a target, aim for 20% of your income added to your Later Money each month.

All that said, I know that some of us operate better if we have a specific target in mind. If that’s you, the conventional wisdom is to aim for 20% of your income added to your Later Money each month.

Obviously, the more you add to Later Money, the faster you will pay off your debt. So, if you can afford more than 20% toward credit card debt each month, do it.

If you’re curious, targeting 20% savings each month was popularized in Elizabeth Warren’s book, All Your Worth: The Ultimate Lifetime Money Plan, first published in 2005 (before she was Senator Warren, she was a law professor and author).

Senator Warren advocated for a 50-30-20 budget framework with 50% going to fixed costs (what I call “Now Money”), 30% going to wants (“Life Money”), and 20% going to financial goals (“Later Money”).

Most personal finance experts agree that the 50-30-20 framework is a solid plan for your budget.

In theory, I agree.

In reality, I’ve become convinced through working with my law students that the 50-30-20 framework does not cut it in today’s environment.

While I agree the 60-30-10 framework may be more realistic, my experience has taught me that assigning rigid percentages is just not a practical framework for most people at the beginning of budgeting process.

Step 3: Make adjustments so your spending better aligns with your true motivations and desires in life.

OK, so now that you have assigned your spending to each of the three categories, the next step is to think and talk about your current habits and whether you’re spending matches your true motivations and desires in life.

If you decide that your spending does not match your life values, then it’s time to make some adjustments.

When you’re in credit card debt, the goal of these adjustments is to create more money each month to pay off your debt.

What kind of adjustments can you target?

In essence, my budgeting philosophy is to aim for steady and lasting improvements based on your current reality and your ultimate motivations.

What does that mean?

This is where we circle back to the importance of having a clear understanding of what we want out of our money. Money is just a tool.

Ask yourself:

“Is your current spending aligned with how you want to use your money to fuel your goals and ambitions?”

If not, you can make incremental adjustments as you progress towards your ideal spending alignment.

The idea will be to continuously add more fuel to your Later Money bucket so you can eliminate your debt faster.

You can make small adjustments, which are usually easier and faster to put in place. These adjustments might include dining out a bit less, cutting out a concert, or cancelling a gym membership or subscription you don’t use.

You can also make big adjustments, like moving to a cheaper part of town or getting rid of you car.

Small or big, the key is that when you make these adjustments, you repurpose that money in a thoughtful and intentional way. When you’re in debt, that means repurposing those savings to paying off debt.

Once your debt is paid off, you can put those savings towards your other financial goals.

You’ve already done the hard part. You’ve already aligned your budget with your money motivations.

With each thoughtful decision, you’re progressing towards your best money life. Most importantly, you’re learning about yourself and developing lasting habits. You won’t get discouraged and give up on budgeting.

To help you better understand how to make a budget to pay off debt, here is exactly how I did it when I was in debt in my twenties.

Here’s an example of how to make a budget to pay off debt.

In today’s budgeting example, we’ll look at how I made a budget to pay off debt in my twenties.

The dollar amounts below are what my actual income and spending looked like back then, adjusted for today’s dollars and rounded for easier math.

For some context, I was 26-years-old, living by myself in Chicago (no dependents, no pets), and working as a “slasher.” Not a joke, that was my actual job title.

I worked for a judge with the Appellate Court of Illinois, and as the junior member of the team, my responsibilities included lawyer duties and secretarial duties. I was a judicial law clerk “slash” secretary. Hence, slasher.

Lawyers are funny, huh?

In today’s dollars, I earned an annual salary of $90,000.00. That means I earned $7,500.00 per month. We did not have bonuses at the courthouse, so the $90,000.00 salary was my full compensation.

The benefit of going through an example like this is not to compare your situation to mine. Your income might be much higher or much lower. Same with your expenses.

Instead of the numbers, focus on the thought process so you can start to think about adjustments that suit your current life to help you pay off debt.

Below, you’ll see charts showing that I completed each of our three steps to make a budget to pay off debt:

Step 1: I tracked my spending for 3 months and reflected the average monthly amount for each expenditure in the column labeled “Baseline Budget.”

Step 2: I created a separate chart for each of the three main categories: Now Money, Life Money, and Later Money.

Step 3: I made thoughtful adjustments to better align my spending with my true motivations in life. I illustrated my decisions in the third column labeled “Budget After Thinking.”

Now Money

Recall that Now Money is what you need to pay for basic life expenses.

These are expenses that you can’t avoid and should be relatively fixed each month. If you have expenses for kids, pets, and other fixed life expenses, be sure to include them in your Now Money category.

Now Money

Baseline Budget

Budget After Thinking

Apartment rent

$2,200

$2,200

Renter’s Insurance

$20

$20

Parking spot

$430

$0

Gas for car

$40

$40

Car Insurance

$50

$30

Car Maintenance

$150

$150

Utilities

$120

$120

Internet

$60

$30

Cell Phone

$55

$35

Groceries

$300

$240

Personal upkeep(wardrobe, haircuts, etc.)

$100

$75

Gym Membership

$360

$360

Budget Busters

$300

$300

Now Money Total

$4,185

$3,600

What I learned tracking Now Money.

Now Money is pretty easy to track. There is not a whole lot of variance from month to month.

You’ll notice immediately that I had one major expenditure that needed immediate adjustment. That parking spot for $430? Definitely did not need that.

I lived 2 miles from work in one of the best cities for public transportation in the country. It was frustrating at times to look for street parking, but I didn’t use my car enough to justify the cost of a parking spot.

The other adjustments resulted in more minor savings, but don’t ignore these. Each adjustment took relatively no effort to make, just a little bit of thought beforehand.

When I say relatively no effort, I mean three phone calls and three reductions for car insurance, internet, and cell phone. That’s $70 saved per month, or $840 saved per year, for about 30 minutes of effort.

Otherwise, I decided to show a bit more restraint when grocery shopping and found a cheaper place to get my haircut.

All told, I reduced my Now Money Budget After Thinking by $585 per month with a little bit of thought and hardly any effort.

That meant $7,020 per year I could reallocate to paying off debt.

Life Money

This bucket, Life Money, is what you spend every month on things and experiences in life that you love.

Life Money

Baseline Budget

Budget After Thinking