When was the last time you drove to a new place without using GPS?

It’s hard to even imagine, right? Driving without GPS and just hoping you get where you need to go?

It’s so unthinkable, it’s almost laughable.

I still use GPS to go places I’ve been to plenty of times before. Even when I’m 90% sure I know where I’m going, I like the comfort of knowing I’m heading the right way.

I like knowing that I’m making progress on the way to my destination.

15 miles to go. Great, be there in about 20 minutes.

I also like knowing ahead of time when I need to turn.

Turn right in .5 miles. OK, need to switch lanes.

Most helpfully, I like being notified promptly if I start heading in the wrong direction. That way, I can make an adjustment before I get too far off course.

Make a U-turn. Oops, missed my exit.

Driving with GPS is so helpful it’s become part of my normal routine. The same for you, I’m sure?

Without GPS, I might be able to find my way. But, it’s so much harder.

Do I need GPS to drive my car?

No.

Is it possible to get where I’m going without it?

Sure.

But, it’s so much harder.

I guess I could write down directions before leaving the house and hope I don’t miss a turn?

Maybe throw a map in the car?

Stop at a gas station and ask for directions?

I don’t love these options but, in theory, they should work.

But, in reality, nobody is putting in all that effort in today’s world. We make it easy on ourselves by using GPS. It’s the best way to get where we want to go.

You see where I’m going with this?

Using GPS is the equivalent of tracking your net worth on your road to financial independence.

You wouldn’t leave the house on an epic road trip without GPS.

So, why would you work so hard to make money if you don’t keep track of what you’re doing with it?

Almost everyone uses GPS and hardly anyone tracks their net worth.

A recent survey found that more than 90% of drivers admit that they rely on GPS.

This does not surprise me at all. Nobody is busting out the map or stopping at gas stations for directions anymore.

You know what does surprise me?

Nearly 70% of Americans don’t track their net worth!

Think about that.

We are more concerned with getting lost in the car than we are getting lost with our money.

That’s a problem.

An easily fixable problem.

Why you need to track your net worth.

I recommend everybody, no matter where you are in your financial journey, track your net worth.

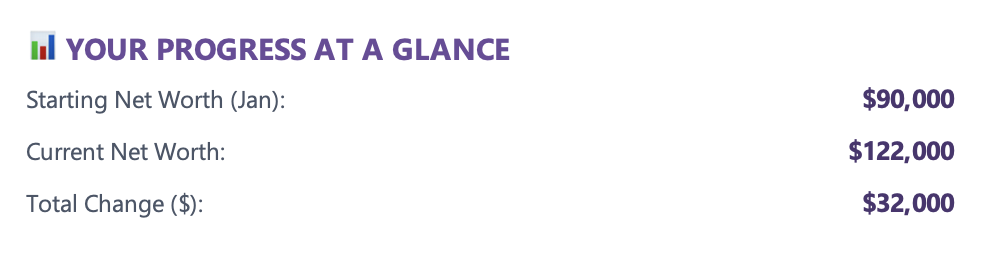

By tracking your net worth, you can quickly see if you are making good money decisions or need to make adjustments.

There’s no better way to learn how much money you’re keeping after a month of making money.

Without knowing your net worth, you risk years going by without making any measurable progress on your financial goals.

You may want to switch careers, buy a house, send your kids to college, or simply retire early.

Or, you may not know exactly what it is that you want. That’s completely normal.

Being good with money and giving yourself options is still the key.

The best way to give yourself options is to know where you currently are and forecast where you’re going. You do that by tracing your net worth.

Tracking your net worth is easy.

By the way, tracking your net worth is not a major time commitment.

It takes me less than 30 minutes each month to track and discuss what I consider to be one of the most important metrics in personal finance.

That’s all the time it takes to know if I am progressing towards my most important financial goals.

If you don’t know your net worth, now is the time to start tracking it.

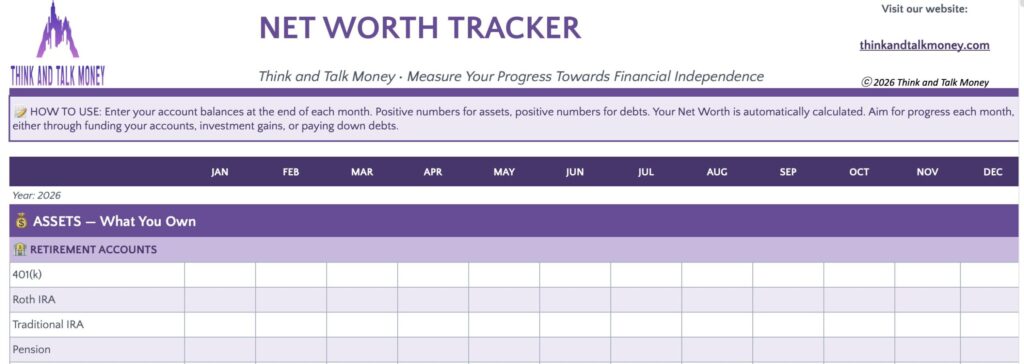

If you need help getting started, you can check out the TATM Net Worth Tracker™️.

What do you get with the TATM Net Worth Tracker™️?

The TATM Net Worth Tracker™️ is based off of the template I’ve personally used for years and shared with hundreds of lawyers and law students in my personal finance course.

You’ll get everything you need to track your net worth in less time than it takes to drink a cup of coffee.

What you’ll get:

- Fully customizable template to track your net worth every month for the next 10 years.

- Total privacy: no need to share your private banking information with a 3rd Party App.

- Instructions and links explaining why it’s so important to track your net worth.

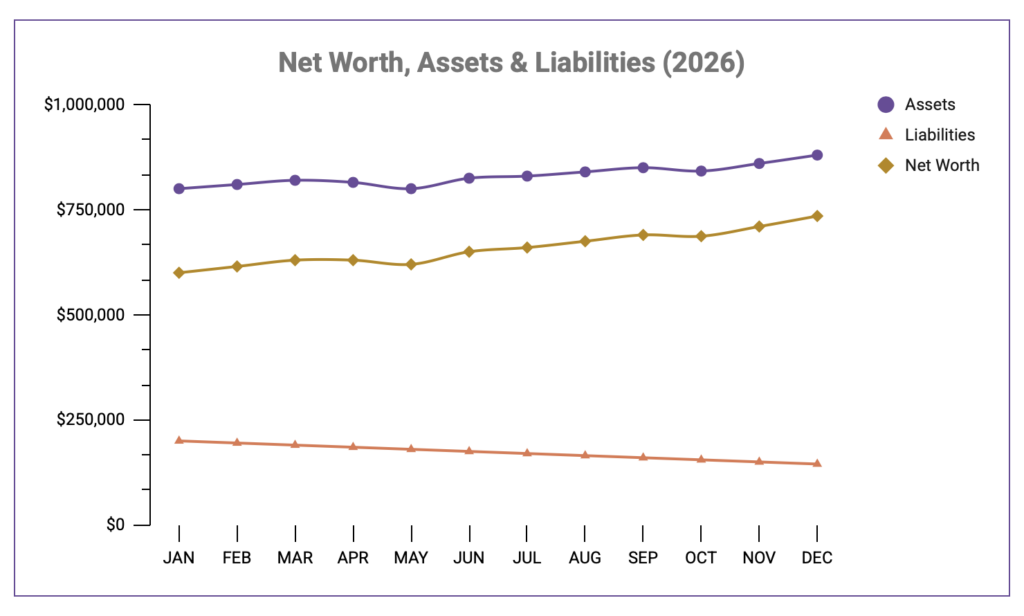

- Visuals on how your net worth grows over time with automatically generated graphs.

As a practicing attorney and law professor… with a real estate business, a personal finance education company, and three young kids… I’m all about using good tools to make things as easy as possible for myself.

The TATM Net Worth Tracker™️ is as easy as it gets.

Now is the perfect time to start tracking your net worth.

If you don’t currently track your net worth, now is the perfect time to get started.

Not convinced?

Maybe the GPS analogy isn’t working for you?

OK, think of tracking your net worth in terms of keeping score during a basketball game.

If you don’t know the score of the game, you don’t know if your strategy is working. You don’t know if you need to make adjustments before time runs out.

The same applies to tracking your next worth. The point is to educate yourself on your current financial situation so you can make adjustments while there is still time.

Do you track your net worth?

Have you been tracking it for a while? Can you imagine not tracking your net worth anymore?

Let us know in the comments below.

Testimonials from my personal finance course.

- “To begin, thank you very much for teaching this seminar. I cannot believe how ill-equipped I was to address budgeting, managing my debt, and saving for my future… Classes like this should be a graduation requirement for all students.”

- “This was a great and very important class for people to take… I think Professor Adair’s course should be a required class, especially for full-time students who are usually just out or recently out of college.”

- “This course addressed a huge need in education. I am so happy that my law school sees this and is doing something to address this need.”

- “Thank you so much for teaching the personal finance class this weekend! I couldn’t have thought of a better class to take as a 3L thinking about life after law school.”

- “This class gave me clarity on many issues including financial mistakes I made that I didn’t even know were mistakes… I have degrees in both business and economics, and I worked in financial advisement at Morgan Stanley.”

- “I absolutely loved the course! It will help me the rest of my life and I hope the school continues to have it! Thank you, Professor Adair.”