Two young coworkers, Terry and Sally, start the same job at the same time making the same amount of money.

While still many years away, Terry and Sally both know that they should invest early and often for retirement.

They each decide to fund a retirement account with an initial contribution of $2,500. They are also dedicated to making contributions of $250 every month until they retire.

Both plan to retire in 40 years while they’re in their 60s.

There’s one major difference between Terry and Sally.

They view risk differently.

Terry doesn’t like risk.

Terry doesn’t like risk. He wants to be able to sleep at night knowing that his hard-earned money is safe and sound in the bank. He can’t stand the idea of potentially losing money from one month to the next.

When Terry wakes up in the morning, he likes to check his bank accounts while he drinks his coffee. He gets a jolt out of opening up his mobile banking app and seeing exactly how much money he has.

In fact, at any given moment, Terry can tell you within a few hundred dollars what his net worth is.

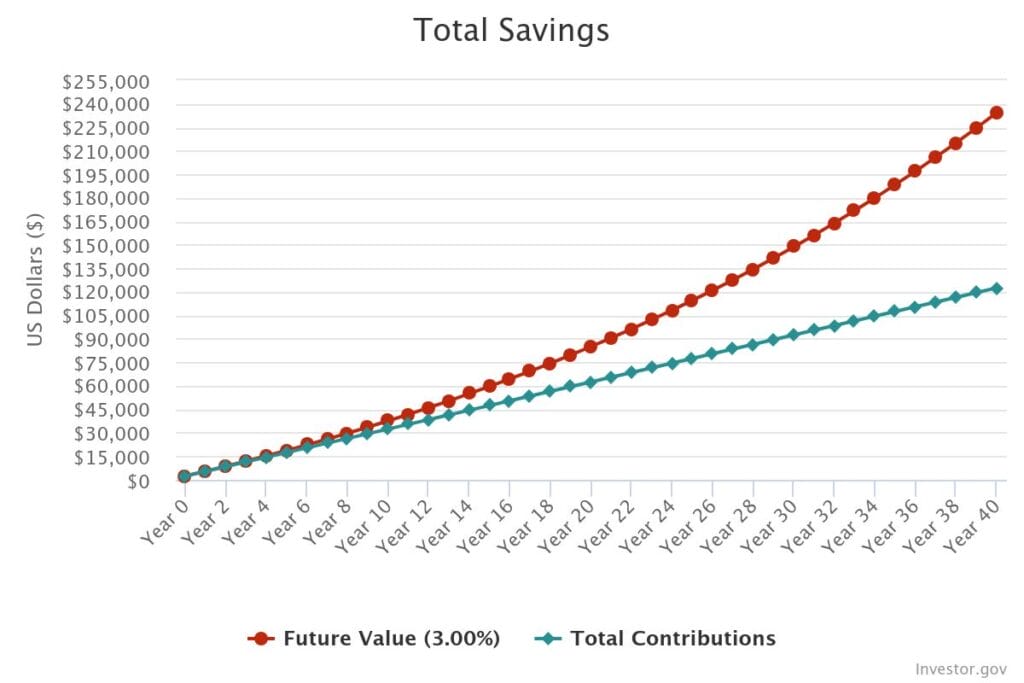

Because Terry doesn’t want to take any chances, he decides to stash all of his retirement savings in a savings account that earns an average annual return of 3%.

Terry is lucky because this is a pretty generous return for a savings account based on historical savings account interest rates.

Sally is more comfortable with reasonable risk.

Sally is more comfortable with reasonable risk. Upon starting her career, Sally was aware that she had never learned basic personal finance skills. She was determined to put in a little bit of effort early on to set herself up for a prosperous future.

She was a frequent reader of popular personal finance websites like Financial Samurai and Think and Talk Money.

Sally even read JL Collins’ book on investing, The Simple Path to Wealth.

Through the process of educating herself about personal finance, Sally started thinking about what she really wanted out of life. Since she was young and had just started her career, it wasn’t easy to come up with a good answer.

Still, Sally knew that whatever she wanted to do in life, investing was an important part of her financial journey. If she wanted to create more time for herself down the road, she would need passive income from investments to sustain her.

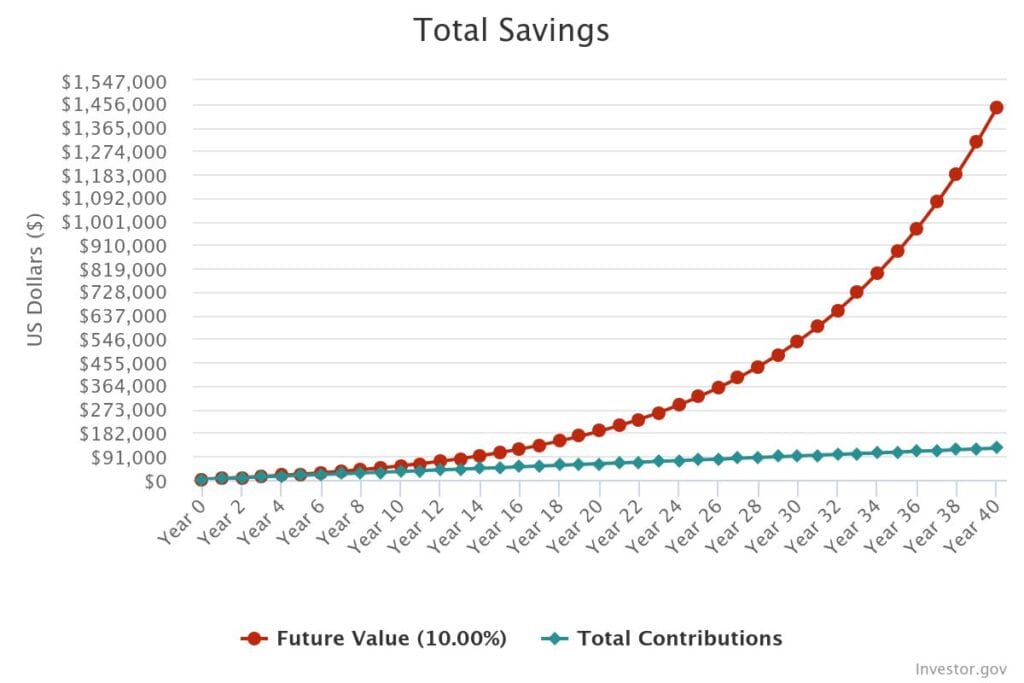

So, after doing her homework, Sally decided to invest her money in a low cost S&P 500 index fund.

While she appreciated that there are no guarantees when it comes to investing, Sally knew that the S&P 500 has historically earned an average annual return of 10%.

Unlike Terry, Sally only checked her accounts once per month when she tracked her net worth and savings rate. Sally slept fine at night because she knew time was on her side.

Let’s see how Terry and Sally turned out 40 years later.

Using a simple online calculator like the one at investor.gov, let’s see how much money Terry and Sally will have in their retirement accounts after 40 years.

Terry’s retirement savings total $234,358.87.

After 40 years, Terry will have contributed a total of $122,500.00 to his retirement savings account.

At a 3% interest rate, Terry will have a total of $234,358.87 after 40 years.

In other words, Terry has just about doubled the value of his total contributions in his account.

Not bad, Terry.

Now, let’s check out Sally’s account.

Sally’s retirement savings total $1,440,925.81.

Sally likewise contributed $122,500.00. After 40 years, at a 10% interest rate, Sally’s retirement account will have a total of $1,440,925.81.

Wow, Sally!

Sally’s retirement account is worth 10 times more than what she personally contributed. Terry failed to even double his account.

Recall in our little hypothetical, Sally did the exact same things as Terry, with one key difference. Sally was more comfortable taking on reasonable risk.

Because Sally was comfortable taking on some risk, her retirement savings were worth more than six times as much as Terry’s savings. She has over a million dollars more than what Terry has!

Look at compound interest in action.

One last thing: take a look at the pictures of Terry and Sally’s investments over time. Notice the gaps between each of their red and blue lines.

While they each benefited from compound interest, Sally benefited exponentially more.

Look at how Terry’s red line stayed much closer to his blue line. Because he wasn’t earning as much overall interest, he didn’t have as much money to multiply from compound interest.

Sally’s red line mirrored her blue line closely for the first 12-15 years. Then, the gap widened before the red line skyrocketed over the final decade or so.

That’s the power of compound interest kicking in.

So, what can we learn from Terry and Sally?

The point of this hypothetical is to introduce the concept of risk when it comes to investing.

We’ve all heard the saying, “You don’t get something for nothing.”

That motto applies to investing as much as anything else. There is always risk involved in investing.

The question is how do you react to that risk.

Some people are so fearful of that risk that they don’t invest at all, like our friend, Terry.

Other people are so desperate to get rich quickly that they take wild risks.

The people that tend to reach and sustain financial independence are the ones who educate themselves and become comfortable with taking on reasonable risk. This is what Sally did.

In future posts, we’ll dive into the various ways you can reduce investment risk.

At this point, knowing why you’re investing and taking on risk is a powerful first step. I was recently reminded of my Money Why when my baby girl was born.

Think of risk as the cost to invest.

If you want to reach true financial independence or any other financial goal, it’s going to cost you something.

Think of risk as the cost to invest.

Sure, there may be some people out there who are able to reach financial independence on a massive salary.

For the rest of us, we’re going to have to get comfortable with investing.

There’s a reason we spend so much time talking about our ultimate life goals. It’s important to embrace the reasons why you’re investing and why you’re opening yourself up to risk.

It never hurts to remind yourself what you are hoping to achieve in the future.

When you know what that thing is, it’s much easier to pay the cost of risk.

When you look at Sally and Terry’s future outlook, who would you rather be?

It’s not really a hard question, right?

It’s not that Sally has a bigger bank account. What matters is that she has created options for herself.

Sally should be in position to do whatever she wants.

Terry probably can’t.

- Are you naturally more inclined to act like Terry or Sally?

- If you’re more like Terry, have you thought about what outcome in life would be worth taking on some reasonable risk?

Let us know in the comments below.

Leave a Reply