What I love most about studying and teaching personal finance is the interconnection between money and life.

We talk about it all the time in the blog.

Money is just a tool to be wielded to get what you really want in life. Money is not the destination, it’s the vehicle to help get you there.

With that in mind, here are my money and life goals for 2026.

By the way, this is the first year I’m sharing more than just my financial goals. My aim is to help you think about how money and life connect in your own situation.

2026 Money and Life Goals

- Pay off remaining HELOC debt.

- Save 6 Months in my Parachute Money.

- Run the NYC Marathon in 4 hours.

- Expand the TATM Resource Library.

- Create the first TATM online course.

- Refocus my best energy on my family.

1. Pay off remaining HELOC debt.

For years, my wife and I used HELOCs to help acquire rental properties. Now that we’re not actively looking to acquire more properties, our goal is to eliminate this HELOC debt.

This is a carryover goal from 2025. Last year, we set out to eliminate the debt entirely. In the end, we managed to pay off 71% of the remaining balance.

While not the end result we targeted, I’m happy with this outcome. Any year that you eliminate 71% of a debt burden is a tremendous year.

Because we made so much progress on this goal in 2025, I anticipate that at our current saving rate, we’ll have the HELOC debt fully paid off by the end of 2026.

It will be an incredible feeling to have this debt load off of our shoulders. We’ve been carrying it for too long now.

Once this debt is eliminated for good, I can focus on more fun goals.

I look forward to updating my net worth in the TATM Net Worth Tracker™️. It excites me to think about my assets growing, instead of just seeing debt shrink.

2. Save 6 Months of Parachute Money.

Your emergency savings account is the most important savings account in personal finance.

I like to refer to emergency savings as Parachute Money.

Last year, my goal was to have four months of living expenses saved up in my Parachute Money account. This year, I’m upping the goal to six months.

Why six months?

Most personal finance experts recommend three to six months. Much of it depends on your current income situation and overall comfort level.

I have income from my primary job, rental properties, and part-time teaching. I could probably get away with only a few months in emergency savings.

However, I now have three young kids. That raises the stakes. I need to make sure they are protected should financial disaster strike.

Taking all that into account, six months of emergency savings feels like the right target for me.

In 2025, for the first time in a few years, we saved 1.5 months of Parachute Money.

This was another “failure” that I don’t view as a failure at all.

When it comes to emergency savings, my challenge has been that I’ve been so focused on eliminating HELOC debt that this goal has typically been pushed aside.

This year, with the HELOC debt dwindling, we’ve set out to make emergency savings more of a priority.

By the end of 2026, this is another goal that we should be able to complete because of what we accomplished this year.

3. Run the NYC Marathon in 4 hours.

I’m 41-years-old. It occurred to me a few months back that the last time I really challenged myself physically was when I played club basketball in college. That was 20 years ago.

Oof.

While I’ve done a decent job of regularly exercising over the years, I’ve never really challenged myself. I’ve kind of just gone through the motions without a specific target in mind.

This year, I’m changing that.

So, why the NYC Marathon?

I listened to a podcast recently where the host encouraged people to think back to what they enjoyed doing as kids and make that a part of their adult lives. Doing so can help improve our overall happiness in life.

I love this advice.

As a kid, I liked to play sports. I liked to compete. Running endurance was always one of my strengths. I was never a fast sprinter, but I could run for days without getting winded.

As an adult, I like running. My normal exercise routine includes going for 2-3 jogs per week. Plus, I’ve always thought about running a marathon, but never made it an actual goal.

Until now.

For my first marathon, I had always planned on running in Chicago. It’s one of the seven world majors and a terrific event. Of course, I love Chicago.

As it happens, my brother-in-law is getting married the weekend of the Chicago marathon, so I pivoted to New York.

Choosing the NYC Marathon led to a great example of using money as a tool.

What’s interesting is that my decision to run the NYC Marathon led to a great example of what I mean about using money as a tool to get what you want out of life.

Here’s the story:

Over the holidays, I mentioned to an experienced runner that I was going to run New York for my first marathon.

He told me it was a bad idea. It would be too expensive. I’d have to buy flights and pay for a hotel. I’d also have to register through an expensive charity because so many people enter the race lottery.

For a few minutes, he told me all the reasons I couldn’t do the NYC Marathon.

I politely listened… and then booked my hotel in New York as soon as I got home.

Money is a tool.

This year, I’m using that tool to run a marathon, something I’ve wanted to do for a while now. Something that will be a personal challenge. Something that allows me to compete like I did as a kid.

The sound of all of that makes me happy.

If I’m not going to use money to improve my health and accomplish something I’ve always wanted to do, what would I ever use it for?

This is exactly what I mean when I encourage you to use money to get what you really want in life.

Any marathon runners out there, please reach out! I’d love to hear your stories.

4. Expand the TATM Resource Library.

In creating Think and Talk Money, my aim is to share the content of the personal finance course I’ve been teaching law students and lawyers for years.

I dedicated 2025 to that aim by blogging 2-3 times per week.

In 2026, the plan is to continue blogging, while also sharing the personal finance tools and resources that have helped me and so many others.

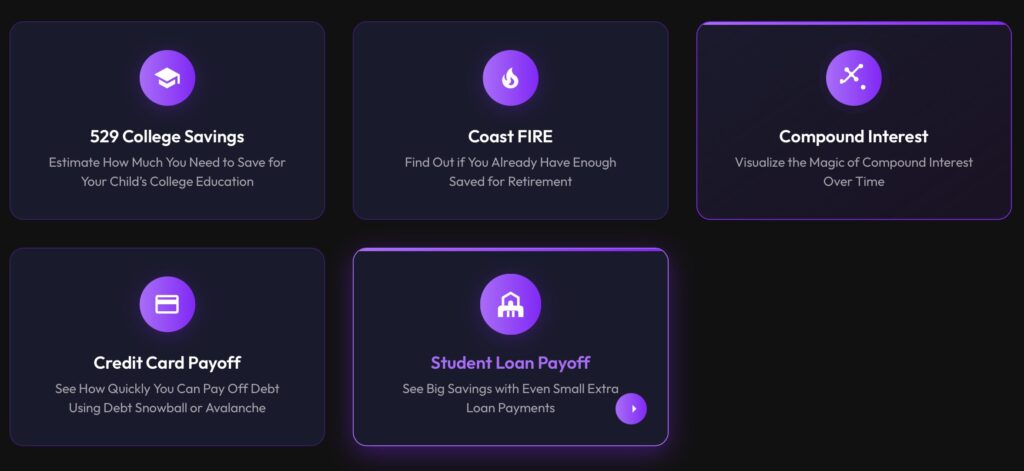

To that end, we now have a TATM Resource Library designed to help you chart out and achieve all of your money goals.

The TATM Resource Library includes five online calculators.

These five calculators are 100% free to use.

I specifically chose to create these five calculators because I find them to be extremely motivating on my own journey to financial independence.

I’ve heard the same from the students and lawyers I have shared them with in the past.

I encourage you to use these calculators to help formulate your own plan to financial independence:

- Compound Interest Calculator to visualize the magic of compound interest over time.

- Student Loan Payoff Calculator where you can see big savings with even small extra loan payments.

- Credit Card Payoff Calculator where you can see how quickly you can pay off debt using debt snowball or debt avalanche.

- Coast Fire Calculator where you can find out if you already have enough saved for retirement.

- 529 College Savings Calculator where you can estimate how much you need to save for your child’s college education.

The TATM Resource Library includes the only two spreadsheets you’ll ever need.

In addition to the five calculators, you can also download the only two spreadsheets you’ll ever need to stay on top of your finances:

If you don’t track your net worth or don’t know where your money is going each month, I recommend you check out these templates.

TATM Net Worth Tracker™️

This is the template I’ve personally used for years. It’s easy to use and customizable for your individual situation.

There’s no better way to measure your progress towards financial freedom.

TATM Budget After Thinking Template™️

This custom template utilizes my Budget After Thinking framework to simplify the budgeting process.

I’ve learned through years of teaching personal finance that people quit on budgeting when it’s unnecessarily complicated.

There’s no reason to make budgeting a process you hate. I designed my system to make budgeting easy, and most importantly, only a temporary commitment.

How is that possible?

Using the TATM Budget After Thinking Template™️, you’ll learn enough about your spending habits in six months that you can create a lasting budget that actually works for you.

At that point, you’ll only need to track two simple numbers to stay on course and achieve your financial goals.

5. Create the first TATM online course.

I’ve taught personal finance to law students and lawyers for years, and I’m energized about sharing my course material online.

So, in addition to building out the TATM Resource Library, I plan to release the first TATM online course in 2026.

Admittedly, I wouldn’t be taking this step if it weren’t for the positive feedback I’ve received from students over the years.

Here’s a sampling of what I mean:

“Really worthwhile course! Prof Adair made a lot of sensitive money-related subjects very accessible and comfortable to talk about, and seems super passionate about the content and helping his students.”

“Should be taught twice a semester probably, so everyone can have a chance to take it.”

“Prof. Adair is very welcoming and relatable. He cares a lot about his students and what he is teaching. He is clearly very knowledgeable in this area and was able to answer everyone’s questions. I am so grateful for his passion to spend the weekend with us!”

“Killed it! Honestly, this may be the most important class I have taken in law school.”

I’m humbled by these sorts of comments and can’t wait to share my course with the TATM community.

6. Refocus my best energy on my family.

I saved my most important goal for last.

This one is a hard goal to measure. I’m sure the “goal police” will take issue with such a vague idea.

Well, it’s my blog. And, it’s my goal.

The truth is my other goals don’t matter without this one.

Similar to my Tiara Goals for Financial Freedom, I view this goal as more of an overarching, continuous force in my life, rather than striving for a particular finish line.

This is the type of goal that I will remind myself of every day.

For starters, it will help me be a better husband. I want to refocus my best energy for more quality time with my wife.

As just one example, that means more date nights.

As any parent with young kids knows, date nights can be hard to come by. In 2026, I want to change that. No more (or at least not as much) ships passing in the night.

I also want to refocus my best energy on my kids.

My kids turn 6, 4, and 1 this year. These years are flying by way too fast.

My oldest daughter is the best chatter I know. She can happily chat for hours, just ask her aunts and grandmas.

There isn’t a person alive who asks me harder questions. “Does space ever end? Is an elephant bigger than my room? Can you drive to South America?”

My son is the sweetest boy in the world. My wife and I ask ourselves just about every day, “How did we get so lucky?”

He’s also a total jokester. Nobody makes me laugh harder. In the car the other day, I quizzed him:

“You and your sister are two of my four favorite things in the whole world. Can you name my two other favorite things?”

Without missing a beat, he responded “Costco and Chick-fil-A.”

Then, there’s my baby girl. She smiles ear-to-ear whenever I walk in the room.

If I don’t smile back at her right away, she’ll say “Hey Dada, Hey Dada, Hey Dada” until I do. Then, she’ll erupt in the biggest smile you’ve ever seen. There is no better feeling.

All in all, I know how lucky I am. I just want to be better at remembering it every single day.

These are the good old days.

Good luck to everyone on achieving your own 2026 money and life goals.

Those are my goals for 2026. I’ll keep you all posted throughout the year on my progress.

I love hearing from TATM readers.

Your goals will surely be different than my goals. By talking about them, maybe we can help each other.

Keep me posted on your progress along the way.

If I can be of any help, don’t hesitate to reach out.

The best way to reach me is to sign up for my weekly newsletter and then reply to any email.

Or, you can leave a comment below.