The stock market has been sliding so far in 2026.

As of this writing, the S&P 500 is down 3.3% in 2026 and the Dow is down 3.8%.

The market can change suddenly, for better or worse. Nobody knows what’s going to happen. Don’t believe anyone who tells you otherwise.

During times like this, it’s important for all of us, and especially young lawyers, to remember the fundamentals of investing.

I was asked recently, “What am I doing with my portfolio while markets are falling in early 2026?”

Despite how chaotic it may seem in the world today, this is not a difficult question for me to answer.

I’m not doing anything.

I invest in the stock market to help achieve my long-term goals. My two main long-term goals are to save for college and to save for retirement.

Each objective is so far away that time is on my side.

Our oldest child is six-years-old, so I have 12-13 years until she even begins college. Over the past two years, we super-funded a 529 college savings plan for my oldest daughter and my son. We plan to do the same for our baby girl.

I fully anticipate that the market is going to go up and down over the next two decades while my kids are in school. That’s part of the process.

As for retirement, I have even more time in front of me. Same as what we just talked about with saving for college, I fully expect the market is going to go up and down many times before I retire.

Time is on my side. That’s why I’m doing nothing.

Like you, I don’t enjoy seeing my portfolio drop so suddenly.

It’s not fun to read the headlines right now. My brain seems to jump to the worst case scenario. Maybe you do the same thing. As lawyers, we’re trained to think of the worst case scenario, right?

This is one of the reasons why I only look at my portfolio once per month when I track my net worth.

To remind myself to hold steady during the down times, I think of a study that examined what would happen if an investor missed the 10 best days for the market in each decade since 1930.

As summed up by CNBC:

Looking at data going back to 1930, the firm found that if an investor missed the S&P 500′s 10 best days each decade, the total return would stand at 28%. If, on the other hand, the investor held steady through the ups and downs, the return would have been 17,715%.

These results illustrate how risky it would be for me to try to time the market. The last thing I want to do is miss the upswing. I have no idea when it’s coming.

But, time is on my side.

I’m going to be in the market when that upswing eventually comes. It may not be until years from now. That works for me and my investment horizon.

Think of it this way: the market is on sale right now.

One other mental hack that’s helping me right now:

I’m telling myself that the market is on sale. How so? I can buy the exact same stocks today for less money than they would have cost even a few days ago. I do love a good sale.

In the end, no matter how bad things seem right now, I plan to continue making regular contributions to each of my investment accounts.

Since I’m investing for the long run, I’ll let the market do its thing while I’m off doing my own things.

Disclaimer: Your situation may be different. I am not an investment advisor. Do your homework and make the best decisions for your personal situation.

What is my personal investing strategy?

When it comes to investing in the markets, I’m about as boring as can be.

My wife and I invest primarily in index funds. We are not active traders. We don’t seek out the newest, hottest stocks.

All we do is make regular contributions to our various investment accounts and let the markets take care of the rest.

As an example, for my daughter’s 529 plan, we chose a passive investment option that’s a mix of stock index funds and bond index funds.

Our portfolio automatically rebalances over time based on my daughter’s projected first year of college. Essentially, the closer we get to her first year in school, the more conservative our portfolio becomes.

We chose a similar option for our other kids’ 529 plans. It’s boring but it works.

Why index funds?

I wrote a post detailing the 7 reasons why I love index funds. Here’s a preview:

- Anybody can do it

- No wasted mental energy

- Low fees

- Automatic diversification

- The closest thing to predictability

- I don’t have stock FOMO

- Good enough for Buffett, good enough for me

Like so many others in the financial independence community, I fell in love with index funds after reading J.L. Collins’ book The Simple Path to Wealth. You can read my full review of The Simple Path to Wealth in my post here.

Even if you work with a financial advisor, it’s crucial to educate yourself so you can make informed decisions, especially in times of economic uncertainty like we’re in right now. As Collins explains, benign neglect of your finances is never the solution.

By the way, it’s not just Collins urging us to invest in broad based index funds. So does the single greatest investor of our lifetimes, if not ever: Warren Buffett.

In 2013, Buffett famously instructed that after he dies, his wife’s cash should be split 10% in short-term government bonds and “90% in a very low-cost S&P 500 index fund.”

Good enough for Buffett, good enough for me.

For more on index fund investing, check out our full series on investing.

How much money should you put towards each of your financial goals?

Between saving for emergencies, saving for college, and saving for retirement, there are a lot of options. In addition, you may have other short term goals, like paying for a wedding or a house. Or, you may want to invest in real estate.

So, how do you determine how much to allocate to each goal?

There’s no perfect answer here.

The first thing you should do is to spend some quality time formulating your version of Tiara Goals for Financial Freedom.

Then, let those goals inspire conversations with your people to help you make the best decisions. This is exactly how my wife and I came up with our financial goals for this year.

It also helps to attach specific targets to your financial goals, like we did when we estimated how much you should be saving to pay for college.

Once you know what you’re striving for, it’s time to commit to a Budget After Thinking. The primary focus of a Budget After Thinking is to generate fuel for the most important goals in your life.

Are you saving too much for retirement?

Spend enough time on the internet, and you’ll get many different answers about how much to save for retirement. There are just too many variables in play to generally answer this question, like what kind of retirement you want and when you want to retire.

My perspective on retirement savings evolved after reading Die with Zero by Bill Perkins.

In Die with Zero, Perkins suggests that many of us are saving too much for retirement at the expense of using that money to live our best lives now.

Perkins’ book is one of the most compelling personal finance books I’ve read in a long time, and I highly recommend it.

Perkins is not suggesting that saving for retirement isn’t important. He’s saying that the hard data shows that most of us are over-saving.

Believe it or not, you may be closer than you think to achieving your retirement goals.

That’s a very powerful realization.

Think about the options you can create for yourself if you no longer need to save a hefty chunk of your paycheck for retirement.

Personally, after reading Die with Zero, I used the Think and Talk Money Coast FIRE calculator to estimate my projected retirement savings. As Perkins would have expected, at our then-savings rate, my wife and I risked over-saving for retirement. In other words, we have reached Coast FIRE.

With that realization, I made some adjustments and am now targeting my other financial goals at a faster rate. I’m also not skipping out on any experiences that appeal to me because of fears about retirement.

What is Coast FIRE?

Coast FIRE relates to Perkins’ thesis that many of us are over-saving for retirement.

The central idea behind Coast FIRE is to aggressively fund your retirement accounts early in your career so you won’t have to save for retirement as you get older.

For lawyers more established in their careers, Coast FIRE represents the idea that all those earlier years of saving means you no longer need to worry about retirement. You can sit back and let compound interest do its thing. Your retirement years are covered.

This is the essence of Coast FIRE: knock out retirement planning early on to create more career and life flexibility later. Coast FIRE does not mean you can stop working altogether. It means that you no longer need to save for retirement.

Why is achieving Coast FIRE so beneficial?

Because once you hit your projected magic retirement number, you no longer need to fund your retirement accounts. With retirement covered, you can reallocate those funds to other financial or life goals. That means you have more optionality in life.

For example, you won’t need to earn as much money if you’re not allocating a big chunk of your income to retirement. That opens up the possibility of switching jobs or working fewer hours. It also means that you can focus more dollars on your present-day self.

Achieving Coast FIRE also means that you can focus on adding present day liquidity to your portfolio. Liquidity means having cash and investments immediately available in case you need it. Increasing liquidity is an important step for maximizing optionality in your life.

On top of that, when markets are dropping, knowing that you have cash-on-hand can give you a lot of confidence to ride out the dip.

How do you figure out if you have achieved Coast FIRE?

The easiest way to determine if you’ve reached Coast FIRE is to use an online calculator, like the Think and Talk Money Coast FIRE Calculator.

Here’s an example.

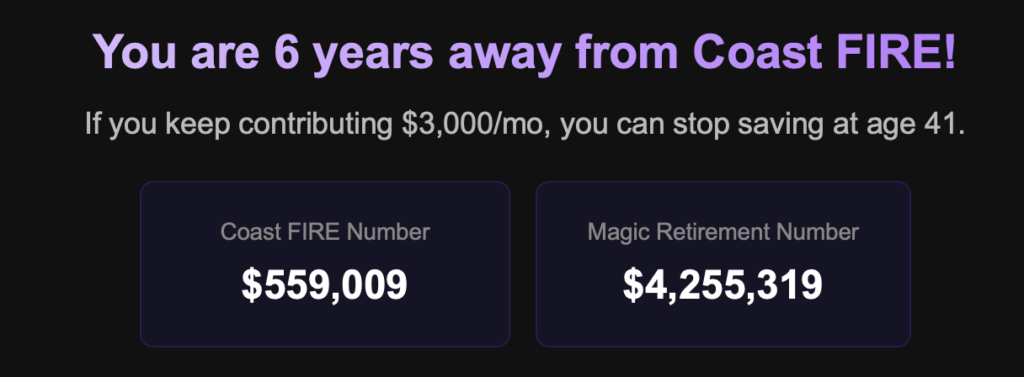

Let’s say you are 35-years-old and plan to retire at age 65. After 9 years of working at a law firm, you have $400,000 saved up in your various retirement accounts. You also currently contribute $3,000 per month to your retirement accounts.

Your goal is to have $200,000 annually to spend in retirement.

We’ll assume an average annual return of 10% (on par with the historical results of the S&P 500). We’ll also factor in a 3% inflation rate (the historical average in the United States). Finally, we’ll assume a safe withdrawal rate of 4.7% in light of the updated “4% Rule.”

Now, we’ll plug these numbers in the Think and Talk Money Coast FIRE Calculator.

Based on the above variables, your Coast FIRE number is $559,009.

What does this mean?

At your current saving rate, you will have $559,009 saved up and will reach Coast FIRE in six years. That means that at the age of 41, you will no longer need to fund your retirement.

The big win is that the $3,000 you had been saving for retirement can be repurposed for other life goals or experiences.

Yes, you need to keep earning money to sustain your present lifestyle. However, you have the option to pursue a lower paying, lower stress job because your retirement years are already covered.

Note: Your FI number (magic retirement number) is significantly higher: $4,255,319. That’s how much money you’ll need saved up by the time you turn 65 in our example to spend $200,000 annually in retirement and not run out of money. Because of compound interest, your balance should grow to that amount without any additional contributions after age 41.

When markets are falling, stick to investing fundamentals.

If you are a young lawyer with a long investment horizon, you shouldn’t be concerned when markets are falling like they recently have been.

Time is on your side. Stick to the fundamentals.

I prefer to invest in broad based index funds, like Collins and Buffett recommend. Regardless of markets rising or falling, I make regular contributions and let compound interest work its magic.

Because I have already achieved Coast FIRE, I am now focused on building more liquidity, which translates into more optionality.

It’s not as much fun to track my net worth these days, but the cyclical nature of the markets is part of the process we need to accept.

Young lawyers: what do you tell yourself when markets are falling, knowing you have a long horizon?

Does it help stay the course if you talk to your people?

Let us know in the comments below.