“I’m worried about today. I’ll deal with tomorrow later.”

“If I cut out vacations and saving for retirement, I can make it work.”

Have you ever heard money excuses like this before?

I recently had a couple of great talks that got me thinking about comments like this. These talks led me to think about common money mindsets we sometimes have when we’re worried about paying for things today.

For many of us, the natural inclination when money is tight is to ignore the future and focus on today.

The pattern goes something like this:

Go to work, pay the bills, keep food on the table.

Wake up and do it all over again tomorrow.

Dream about life-enriching experiences and retirement later.

The problem with this money mindset: how are you ever going to break the cycle?

How are you ever going to progress towards financial independence so your life is not stuck on auto-pilot?

My challenge to you?

When money is tight, think long and hard about the future. Think about what comes next.

Use a challenging period in your life as motivation to do things differently.

It helps to picture yourself 10 years from now. Imagine you don’t do anything differently.

Same Job. Same bills. The cycle continues.

Do you like what you see?

If you do, no need to read any further. Keep doing what you’re doing.

If you don’t like what you see, let me share another perspective with you.

Let’s use the future as motivation to make the hard decisions today.

That way, you can spend your money (and time) on the things and experiences that bring you happiness in life.

Some dollars will be used to pay your ordinary life expenses, some dollars will be used for all the things in life you love, and some dollars will go to your financial goals.

That’s all there is to it.

When it comes to budgeting, I divide my money into three primary categories:

Now Money

Life Money

Later Money

Now Money

Now Money is what you need to pay for basic life expenses.

These are expenses that you can’t avoid and should be relatively fixed each month. If you have expenses for kids, pets, and other fixed life expenses, be sure to include them in your Now Money category.

Life Money is what you are going to spend every month on things and experiences in life that you love.

This bucket includes dining out, concerts, vacations, subscriptions, gifts, and anything else that brings you joy.

We can’t be afraid to spend this money. This bucket is usually what makes life fun and exciting. The key is to think and talk so you are spending this money consistently on things that matter to you.

Later Money

Later Money is what you are saving, investing, or using to pay off debt.

This bucket includes long term goals, such as retirement plan contributions (like a 401k or Roth IRA), college savings for your kids (like a 529 plan), emergency savings and paying off student loan or credit card debt.

This bucket also includes any shorter term goals, like saving for a wedding or a downpayment for a house.

Most fun of all, this bucket includes any investments you make to more quickly grow your wealth, like investing in real estate or the stock market.

Later Money is the key category that fuels your ultimate life goals, like financial independence. The more you fuel this category, the faster you can reach your goals.

Your budget is really just about finding fuel for the best things in life.

This is where we circle back to the importance of having a clear understanding of what we want out of our money.

“Is your current spending aligned with how you want to use your money to fuel your goals and ambitions?”

If not, you can make incremental adjustments as you progress towards your ideal spending alignment.

The idea is to continuously add more fuel to our Life Money and Later Money. Why?

These are the buckets that represent the things we love the most (Life Money) and our most important life goals (Later Money).

When money is tight, resist the urge to cut these expenses from your budget. These are the expenditures that oftentimes give meaning to life and allow us to build a future on our terms.

Instead, focus on the Now Money bucket as much as possible.

You can make small adjustments, which are usually easier and faster to put in place. These adjustments might include dining out a bit less, cutting out a concert, or cancelling a gym membership or subscription you don’t use.

You can also make big adjustments, like moving to a cheaper part of town or getting rid of you car.

Small or big, the key is that when you make these adjustments, you repurpose that money in a thoughtful and intentional way. You’re now starting to align your budget with your money motivations.

These adjustments will give you options in the future.

With each thoughtful decision, you’re progressing towards your best money life. Most importantly, you’re learning about yourself and developing lasting habits. You won’t get discouraged and give up on budgeting.

Creating a Budget After Thinking is really all about one question:

What do you really want out of life?

When you prioritize Life Money (experiences) and Later Money (financial freedom), each dollar you spend or invest brings you one step closer to that ideal life.

If you are totally consumed with Now Money, you’ll struggle to build the life that you really want.

By that point in my life, I had paid off my student loan debt and was about to get married.

My soon-to-be wife and I had good money coming in, but I never truly thought about what I wanted in life. Sure, I had thought about things like having a family and being able to take vacations.

But, I never carved out time to purposefully think hard about what I actually wanted. I had never asked myself what truly motivates me.

I never allowed myself to dream about financial freedom.

The truth is, I don’t think I had ever visualized a life that wasn’t dominated by a full-time job.

Up to that point, my whole life had revolved around getting an education and then getting a job. I never pictured a world where I might not need a full-time job to provide for myself and eventually my family.

I had read about the concept of being financially free, but it always seemed like a possibility for other people, not me.

Writing this years later, I feel sad for that version of myself for having such limiting beliefs.

Whenever someone tells me she doesn’t make enough money to dream about the future, I think about those same limiting beliefs I used to have.

That’s the cycle I’m hoping to help people break.

When money is tight, think about the future.

When it comes to spending choices, resist the urge to cut the things from your budget that make life what it is. That might mean money spent today on memorable experiences, like vacations.

Or, it might mean money saved and invested to provide yourself more options down the road.

The key is to break the thoughtless spending cycle that can make your life feel like it’s stuck in place.

Create a Budget After Thinking that prioritizes what you truly value.

Money might still be tight, but you’ll know you’re spending on things that matter.

You’ll know that you’ll have options in the future.

Having taught personal finance to law students and young lawyers since 2021, I’ve picked up on a common theme.

At the conclusion of class, my students tend to be motivated and excited to get good with money.

This makes sense because we spend a lot of time thinking and talking about what our ideal lives look like. Then, we learn how to use money as a tool to build those lives.

In the weeks following class, I usually hear from several students who want to follow-up about topics we cover in class, like side hustles or investing in real estate.

I’ll meet each student for coffee downtown and give them some feedback on their ideas. I love these money talks over coffee.

My students’ excitement to take control of their money and their lives is contagious.

Their excitement rubs off on me. I leave these conversations motivated to check in on my own money strategies and goals.

When our chat is wrapping up, I always encourage my students to keep me posted on their journeys. I invite them to check-in every few months so I can help keep them accountable and to adjust any plans we’ve put in place.

Unfortunately, less than 10% of my students ever follow-up after these initial meetings.

After a while, I figured out what was going on.

See, every now and then, I’ll run into one of these former students at a lawyer event or hanging around the courthouse. I’ll ask them about work and life and eventually about the money plan we talked about.

That’s when I usually hear something like, “I’m still thinking about that side hustle. I just put it on the back burner for now. I’m going to do it someday.”

Do you see the problem?

As a wise man once taught me, “someday” means “no day.”

Financial freedom is about consistent, intentional choices.

Ask anyone who has reached true financial freedom how they did it, and you’ll pick up on something right away.

You’ll quickly realize that people who reach financial freedom got there by making consistent, intentional choices with their money.

They came up with a plan and they stuck with it.

They didn’t say “some day.”

Achieving financial freedom is not about being the highest earner or the best investor.

It’s about consistency.

There are endless ways to make money. The same goes for investing that money.

You can reach financial freedom as a lawyer who invests in index funds.

Just the same, you can be a consultant who owns rental properties.

Or, an engineer who buys laundromats.

The point is the avenue you choose to build wealth is less important than the consistency of your choices.

For example, if you commit yourself to investing 20% of your salary in index funds, you will be well on your way to financial freedom.

But, if you can’t follow through on your plan for more than a few months, you’re never going to get there.

Of course, we’ve all experienced this tendency in various areas of life. The easiest examples to think of relate to fitness and healthy eating.

How many of us have said we’re going to commit to working out five days a week or eating vegetables every meal, only to give up after a couple months?

It’s not that we want to give up, just that the rest of life gets in the way. We tell ourselves that we’ll return to healthy living someday, which actually means no day.

When it comes to your money choices, don’t let the rest of life get in the way. Money is such a powerful tool when wielded properly and consistently.

Don’t waste this powerful tool.

To help make consistent choices, think about why money matters.

To help you make consistent money choices, the first step is to think about a simple and powerful question: why does money matter?

For me and many others, money is about financial independence, which translates to the power to choose.

When we have the power to choose, we have the power to live a life that conforms to our personal values. That means we can live on purpose, not on auto-pilot.

What does it mean to live on purpose?

It means that we can choose to spend our working hours doing what is meaningful to us. It means we can choose to spend more time with the people who are meaningful to us.

My favorite part during my personal finance for lawyers class is when my students share their motivations with each other. We all learn so much from these honest conversations.

It’s why I believe talking about money is so important. We all benefit from knowing that we’re not alone in our money worries. We can be inspired by hearing what our friends want from their money and their lives.

The more you think and talk about why you want to be good with money, the clearer your motivations will become.

To help you get started, here are three powerful reasons why I want to be good with money:

1. Money can give you choices.

This may seem obvious, but when you have money, you have choices.

You can choose where to live. You can choose who you work for or can work for yourself. On a daily level, you can choose how you eat, exercise, relax, and travel.

This holds true whether you make $50,000 or $250,000. Of course, your options may be different. The point is that when you’ve made good money choices, you’ll at least have options.

2. Money can give you personal power.

This is another way to say that money gives you control of your life situation.

If you are in a bad relationship, a bad job, or just need a change, money gives you the personal power to do something about it. When you don’t have money, you may be stuck.

3. Money can give you time.

When you have enough money to be truly financially independent, you have earned the freedom to do whatever you want with your time.

As I mentioned earlier, you can spend your working hours at a job that is meaningful to you. And, you can spend more time with people who are meaningful to you.

It’s been said many times, “time is our most precious resource.”

Years ago, I asked myself this important question. I wrote down my answer and called it my Tiara Goals.

If you haven’t ever actively thought about what you would do with financial freedom, now’s the time to do so. It is extremely motivating.

Even when you feel like financial freedom is only a distant dream for you, it’s important to actively think about what you want out of life.

I’d even suggest that the further away you feel from financial freedom, the more important it is to think about what it would mean for you.

When you’re at your lowest point, visualizing what you would do with financial freedom is a helpful escape.

Don’t forget to write down whatever you come up with.

Here are my 7 Tiara Goals for Financial Freedom:

Be with my wife and kids as much as I want. Dad never missed a game. Mom never missed a game. Nana never missed a game.

Not be forced to commute to work on Friday or Tuesday or whatever day, if I need that day for myself.

Choose how to spend my working hours (representing clients, teaching, volunteering, building a business, etc.).

Continue to study and learn constantly.

Take at least one big trip every year.

Never turn down an exciting or smart opportunity because I can’t afford it.

Work alongside people that value my contributions.

Keep in mind that I wrote these goals before I had kids and before I was even married. This was also years before the pandemic when working from home was a foreign concept to most of us.

I think it says a lot that I was thinking about these things way back then.

Being consistent means thinking just a little bit about money every week.

My goal is to help you think even a little bit about your money choices every week. That way, your money life remains in balance with the rest of your life, and you can continually evolve and adapt your choices as your life changes.

I want to encourage you to think, and to talk, and to choose. If all I do is help you and your loved ones think more purposefully about your money, Think and Talk Money will be a success.

Maybe your goal is also financial independence, or the power to choose and to live on purpose.

Maybe it’s something else entirely. Whatever it is, discovering your motivation is the crucial first step.

It’s so important that I’ll encourage you to think about that motivation every week.

I’ve learned that money is something that we all need to think about as a regular part of our lives. Not that we should only think about money. Or that we need to obsess over money. Simply that we can’t ignore money.

How sad is it when we realize our hard earned money has just vanished? That at the end of each month, we have less money?

You don’t have to struggle with making continuous money choices alone.

Most of us could use someone to talk to or something to read to help us learn about personal finance.

I hope Think and Talk Money can be that place for you.

I can’t, and won’t, tell you what to do with your money. It’s your life, after all. But, I will strive to help you think and talk with purpose about your money.

The basic money concepts are easy enough to understand. Consistently making good choices is hard.

Most of us could ace a quiz that asked, “Is it a good idea to spend more money than you earn every month and plummet deeper and deeper into debt?”

Knowing what to do is not the same as actually doing it. Remember, someday is no day.

That’s why it helps to not be afraid to talk about money. For some reason, most of us choose to deal with money on our own. I’d like to change that.

There’s a stigma that we shouldn’t talk about money. I’d like to change that, too.

That way, we all have a better chance of making intentional, consistent choices with our money.

Have you been excited about money in the past only to lose that excitement not long after?

Have you tried talking about money with your friends and family to help you stay motivated? If not, what is holding you back?

I thought of this question the other day as I sat in the yard. It’s such a simple but important question.

You should be able to easily feel money well spent. If nothing comes to mind, that might be an indication that the money you are spending has not been well spent.

This one purchase gave me an extended, triple happiness boost.

Buying this tree for my backyard gave me a triple happiness boost.

First, I enjoyed the process of learning about and choosing the right tree.

I liked talking trees with the experts at the nursery and my family members. My kids and I would walk around the neighborhood and take pictures of any trees that we liked. It was infectious how excited they were to hunt for beautiful trees.

Even though my daughter’s first choice was this Easter egg tree, she eventually relented and agreed the Baby Blue was the way to go .

My second happiness boost came from buying and then planting the tree.

The day I bought the tree, I walked around the nursery in the rain with my father-in-law and picked the actual tree we wanted. I’ve never picked out a tree before, but it was fun. I learned from the experts and enjoyed pretending I knew what I was doing.

The next day, the landscaping crew came over to plant the tree. It was fun to strategize exactly where to put it and then watch the experts execute the plan.

My third happiness boost came the next day with the tree in the ground and my kids running around the back yard.

My son played with his toys at the base of the tree. He and his sister played hide-and-seek and took advantage of the new hiding spot.

The whole time I watched them, I sat with a smile on my face. I expect that feeling will continue every time I look at Baby Blue in my yard.

So, yeah, Baby Blue was money well spent.

And yeah, I know. I’m old.

Baby Blue brought me joy before, during, and after the purchase.

Baby Blue is an example of the trifecta of happiness. It brought me joy before, during and after.

The same happiness effect has been well-documented when it comes to traveling. People get a happiness boost in planning the trip, then taking the trip, and finally remembering all the fun things they did on the trip.

That’s why so many people “love to travel.” It brings them happiness before, during, and after.

Baby Blue taught me that I can spend money to get that same triple happiness boost even when not traveling.

I recently met up with an old friend for a great talk about money.

I experienced the same trifecta recently when I met up with an old friend for a great talk about money.

Funny enough, we reconnected after he learned from a mutual friend that I had launched Think and Talk Money. I had no idea that he’s as fascinated about personal finance as I am.

I had been looking forward to our “date” since we planned it a couple weeks ago.

The conversation was great. We talked about money, careers, kids, and shared friends. We hadn’t seen each other for years, but you would never know it. That’s the sign of a good friendship.

When the check came, I was delighted to spend my money. That conversation brought me a lot of happiness.

Since we met up, I’ve been revisiting in my mind so many of the topics we covered. I’m already looking forward to the next time we get together.

That’s money well spent.

Personal finance is not just about the numbers.

In the personal finance world, we spend a lot of time talking about numbers. That’s not a bad thing. Numbers help us turn our ultimate life goals into quantifiable action steps.

However, saying you want to “buy a house” is nice, but it’s not that helpful for planning purposes.

Saying you want to “save $100,000 for a down payment on a house in the next 3 years” is an improvement.

Running the numbers and committing to saving $2,800/month to achieve that goal is even better.

So, while numbers are certainly important in personal finance, it’s equally important to continuously recognize the emotions behind those numbers.

Those emotions turn into our motivation to stay on track and hit our numbers.

Personal finance is tied to our emotions.

I spent money on Baby Blue. In exchange, I received a triple happiness boost. The same is true about catching up with an old friend. These experiences reminded me of why I care about money.

Money is nothing but a tool. I care about money because I want to wield that tool to bring me and my family happiness.

Happiness is hard to define. Spending money in exchange for happiness can be hard to accomplish. What has helped me in that regard is thinking about how I can use money to get what I want.

Sometimes, that means taking a deep look at my Money Why. Or, it could mean sitting on a beach with a notepad (and maybe a beer or two) and writing down my Tiara Goals for Financial Freedom.

But, thinking about money is not just about long term goals.

It also means how we spend our money in the present.

Humans are emotional creatures. We can rationally look at examples and charts and won’t dispute the long term magic of compound interest.

At the same time, we have emotions and feelings that need to be tended to now.

It’s not realistic to expect people to put off all happiness until some unknown time in the future.

It is realistic to make reasonable sacrifices now to ensure a better future.

That’s the essence of investing. We invest money that we could spend today and hope it turns into more money later on.

What might be a reasonable sacrifice for one person may be totally unreasonable for someone else. That’s perfectly fine. Still, it’s one thing to make sacrifices. It’s another thing to deprive ourselves entirely.

I don’t think it’s reasonable to expect people to entirely deprive themselves of the things that make them happy. The key is understanding what those things are, and then spending our money in the pursuit of those things.

This is one of the things my friend and I talked about the other day. It’s not that hard to understand the numbers on the spreadsheet. It’s much more difficult to stay motivated to keep making good money choices.

This intersection of money and life is what makes personal finance so fascinating.

Personal finance is fascinating, not because of the numbers, but because of the emotional impact of money.

It’s why I encourage people to talk about money with their loved ones. Talking money is not about talking numbers and spreadsheets. It’s about motivating each other to intentionally use money in a way that aligns with our values. And, to do so both in the present and in the future.

When we create a Budget After Thinking, this is exactly what we’re doing. Not only are we generating fuel for our Later Money bucket, we are giving ourselves permission to spend our Life Money on things we truly care about.

So, what’s the best money you’ve spent recently?

I bought a tree.

I had a beer with a friend.

Sure, I could have saved that money and invested it. But, I’m glad I didn’t.

I had the happiest occasion to think about that question this past week.

My wife and I welcomed our third child, a little baby girl.

We were very fortunate and had a smooth delivery process.

Even so, when you’re in the delivery room, your mind runs wild. You just want everything to go well. It’s completely out of your hands by that point.

Things get really interesting when you’ve been at the hospital for a while and haven’t slept. There’s no telling where your mind will go.

No matter how much you tell yourself not to do it, you can’t help but think of all that can go wrong.

During these moments, I can assure you that one thing you’re not thinking about is money. If anything, you’re thinking that you would trade all the money you have for a healthy baby and a healthy mom.

When you finally hold your new baby, nothing else in the world matters. Everything around you goes quiet. The sense of relief is overwhelming and you cry.

It’s a beautiful thing.

In those first few moments, I told my baby girl that I love her. I promised that I will always protect her. Whatever she needs, I will be there.

If I want to keep that promise, I need to be good with money.

To be good with money, I need a powerful Money Why.

I wrote down that goal before I was even married or had kids.

Years later, my Money Why hasn’t changed. The only thing that’s changed is my Money Why has gotten stronger and stronger since then.

In 2017, my Money Why got stronger when I got married.

Then in 2020, my Money Why got stronger when my daughter was born.

Again in 2022, my Money Why got stronger when my son was born.

This week, my Money Why got stronger when my baby girl was born.

My Money Why has never been more clear. It doesn’t even matter if my brain is functioning at half speed right now on limited sleep.

My Money Why is my baby girl, my son, and my daughter. My Money Why is my wife.

Of course, I want to provide for my family financially.

But my Money Why is more than that.

I don’t want to just provide money, I want to provide time. And, I want to be present and share experiences.

Most of all, I want to be with them.

My overall goal in life is to spend as much time as possible with the people who are meaningful to me. To accomplish that goal, I need to be good with money.

If I’m good with my money, I can achieve financial freedom.

With financial freedom, I can choose how to spend my time. That means I can choose who to spend my time with.

My Money Why is not about being rich.

Saying that I want to be good with money is not the same thing as saying that I want to be rich. Funny enough, people that are good with money oftentimes feel rich regardless of what their net worth is.

But I’ve noticed on my path to financial freedom there were several times when I felt incredibly rich and money wasn’t the dominant reason.

I couldn’t agree more with Dogen. There’s no richer feeling than having just come home from the hospital with a healthy baby girl. That feeling has nothing to do with money.

Check out more from Dogen at his website financialsamurai.com. There’s a reason why he is one of the leading voices in the personal finance space.

Simply making a lot of money will not make you feel rich.

On the flip side, people that make a lot of money but are not good with money often feel like they’re struggling to get by. As CNBC explained after talking with financial psychologists:

Whether you’re aiming to save more cash or boost your overall earnings, it’s important to ask yourself what you hope to achieve by obtaining more money, Chaffin says. Otherwise, if you don’t change your internal money beliefs, you may still feel anxious about money even if you hit millionaire status.

The takeaway is that it is pointless to make money without stopping to think why you want that money and what you’re going to do with it.

Money is nothing but a tool that you can manipulate to get what you truly want out of life. The thing is, you have to actually think about what you want if you are going to use that tool effectively.

Don’t wait for a major life event to start thinking about money.

You don’t have to wait until you have a baby to start thinking about what money can do for you. In fact, if you wait for a major life event like that, it’s going to be a lot harder than if you start thinking now.

Ask yourself:

“What is my Money Why?”

Whatever comes to mind, write it down.

Maybe you want to retire early. Maybe you’re just looking for a life pivot, as Scott Trench, CEO and President of BiggerPockets wrote about recently and has regularly discussed on the BiggerPockets Money podcast.

I personally agree with Trench, and I like almost everything about FIRE, which stands for Financially Independent Retire Early. It’s just that I know that retiring early is not for me.

I prefer to think of it as FIPE:

Financially Independent Pivot Early

With FIPE, the goal is not to retire. The goal is to give yourself the freedom to choose what to do next.

Whether you want to retire early or just pivot to a new chapter in your life, being good with money is key.

Besides, I’ve never seen the point in working endless hours to make money, while spending hardly any time seriously thinking about how to keep that money.

What’s your Money Why?

My Money Why gets clearer by the day. It has never been more clear than it is right now after bringing home a little baby girl.

What is your Money Why?

Has your Money Why changed over time?

How does your Money Why impact your relationship with money?

Each year, they analyze data from 140 countries and publish their findings in an effort to give everyone the knowledge to create more happiness for themselves and others.

Please imagine a ladder with steps numbered from 0 at the bottom to 10 at the top. The top of the ladder represents the best possible life for you and the bottom of the ladder represents the worst possible life for you. On which step of the ladder would you say you personally feel you stand at this time?

WHR explains that this “life evaluation” question empowers people to make their own judgments about what matters most.

As part of its analysis, WHR uses economic modeling to explain countries’ average life evaluation scores. They look at six variables, and one of them jump out at me:

“Freedom to make life choices.”

What countries would you guess scored the highest on the 2025 rankings?

The top five countries in the happiness rankings are:

Finland

Denmark

Iceland

Sweden

Netherlands

Each of these nations has ranked near the top for a long time.

Where is the United States on the happiness chart?

The United States fell to number 24, its lowest happiness ranking ever.

The United States’ highest ranking was 11th place way back in 2011.

I’m not totally surprised that the United States’ ranking is as low as it’s ever been.

We’ve discussed some theories that may help explain this drop:

8 out of 10 of us are worried we may lose our jobs this year.

Nearly half of us don’t use our hard-earned paid time off (PTO) and choose to work more days than we are asked to.

I wasn’t surprised to see the United States rank 24th in the global happiness rankings, but I was shocked by the sub-ranking for this specific question:

Are you satisfied or dissatisfied with your freedom to choose what you do with your life?

The United States ranked 115th out of 147 countries in response to the freedom question!

When we are financially free, we can choose to live life on our own terms. To me, that sounds a lot like what the WHR freedom question is trying to answer.

When you have financial freedom, you can make important decisions based on what truly matters. When you don’t have financial freedom, you risk making unsatisfactory decisions for money reasons.

We can choose to spend more time with the people who are meaningful to us.

We can choose to use our skills for work that is meaningful to us.

Most of us grow up thinking that life only revolves around getting an education and then getting a job. We don’t allow ourselves to believe that financial freedom is possible for us.

This was exactly how I felt before I wrote down my Tiara Goals one day on the beach in 2017.

My goal with Think and Talk Money is to help us all realize that financial independence is within our reach. If we can think and talk about our money choices even a little bit every week, we can make sure our money life remains in balance with the rest of our life.

By practicing strong personal finance habits, each of us can feel more satisfied with our freedom to choose what to do with our lives.

How would you rank yourself on the freedom question?

Are you satisfied with your freedom to choose what you do with your life?

What are your core values?

Have you ever written down your core values?

Do you know what you’re striving for?

Successful businesses look at these questions regularly. I find it helpful to learn how successful businesses operate so I can apply similar principles to my own life.

For example, there’s a great business book called Traction by Gino Wickman. In the book, Wickman encourages businesses to focus on vision, mission, and values.

It seems like a pretty good idea for all of us to think about vision, mission, and values as they apply to our own lives.

For example, if you’re one of the nearly half of Americans not taking your PTO, are you making that choice based on your core values?

It’s possible that you are. Perhaps you’re being strategic and have formulated a plan to benefit from all those extra hours at the office.

Or, it’s possible that you’ve never really stopped to think about why you’re working so much. You’ve never paused to articulate to yourself what you want out of life.

In Traction, Wickman makes a compelling argument why businesses should not skip this crucial step.

We all should take the same step in our personal lives. In 2017, I wrote down my core values, what I call my Tiara Goals.

Looking at the big picture, my Tiara Goals have helped me visualize what I truly want out of life.

In the short term, my Tiara Goals help guide me through difficult decisions. As long as I’m clear with myself about what I want in the long run, I can make daily decisions to get my closer to those goals.

Millennials want more kids but can’t afford them.

According to a recent report from Business Insider, Millennials want more kids but can’t afford them.

This makes me sad.

The study points to rising costs, as well as the reality that Millennials are saddled with large amounts of student loan debt.

Combined, it makes sense that Millennials are worried about money.

If you want to start a family, or grow your family, what better motivation could there be to spend a little bit of time each week thinking and talking about money.

If this is your reality, or you know someone in this position, establishing strong personal finance habits is crucial.

Each week at Think and Talk Money, we focus on developing these strong personal finance habits.

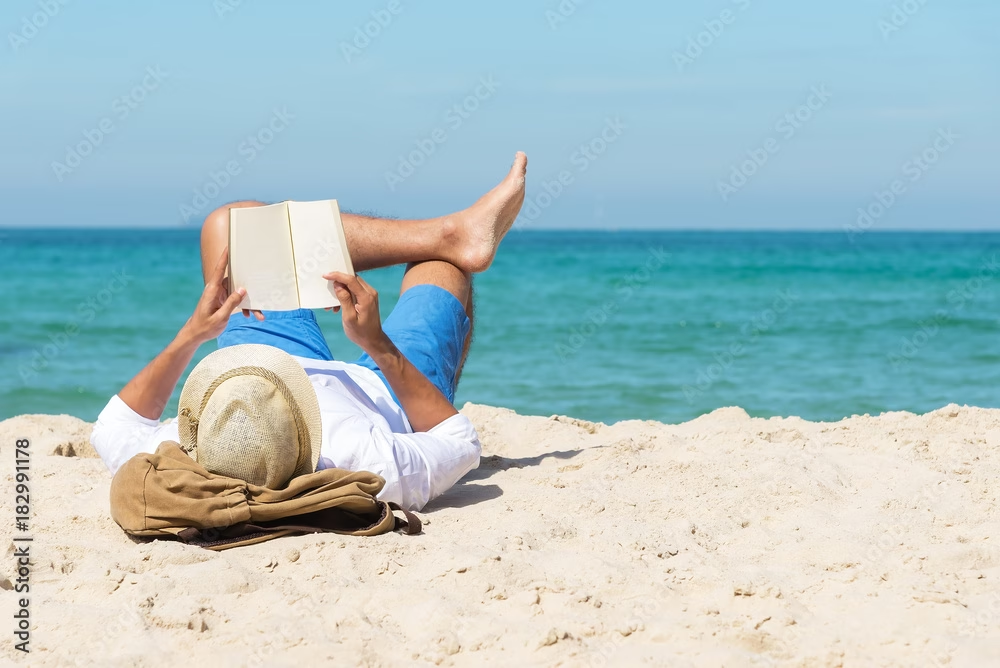

A few months before we got married, my wife and I took a trip down to Florida. One afternoon, I headed out to the beach with a book, a notebook, and a few ice cold beverages.

The weather was perfect. It was sunny but not too hot. Blue skies and just a slight breeze. The beach was quiet that afternoon. I set up my chair to face the ocean and started reading. This little break was exactly what I needed in the middle of “wedding planning.”

I don’t recall the book I was reading that day. I’ve been meaning to look back at my journals to see if I can figure it out. Anyways, I’ll never forget what I learned about myself that afternoon.

The author wrote about the power of financial freedom. We’ve discussed financial freedom in previous posts. The basic idea is that when you are financially free, you can choose how to live your life on your own terms. You can make important decisions based on what truly matters to you, as opposed to being forced down a certain path for money reasons.

On the beach that day, the concept of financial freedom was not new to me. I had read about it for years. The concept really hit home that afternoon when the author asked a simple but powerful question:

What would you do with financial freedom?

Maybe the question really resonated with me because I was about to get married. It’s only natural to daydream about what life would be like after the wedding, even though my wife and I had been a couple for six years by that point.

Over the years, we had talked a lot about what we wanted our lives together to look like. We knew long before the wedding how we each felt about major topics like starting a family and where we wanted to live.

We were also on the same page when it came to money decisions. My wife and I met early on during my personal finance journey, not long after I had determined to get my money life sorted out. My wife still jokes that she was my first personal finance student.

By the time we got married, I had been on my personal finance journey for about seven years. I was out of debt and was starting to think about the options that were now available to me. It was around this time that I learned one of the most powerful words in personal finance:

DINK

Back then, my wife and I were both working as lawyers in Chicago. We didn’t have any kids. I didn’t realize it until later on, but we were DINKs.

DINK means “Dual Income No Kids.”

When you’re in a relationship where you have two incomes coming in and are sharing financial responsibilities, you have the opportunity to supercharge your Later Money goals.

If you are currently a DINK, or will soon be a DINK, please pay extra attention here.

Don’t waste this powerful opportunity to supercharge your Later Money goals.

This is what my wife and I were able to do, even if we didn’t know what a DINK was. We each had good incomes coming in and our monthly expenses were low. The two of us could comfortably share an apartment, instead of each paying for an apartment separately. That’s major savings each month.

We didn’t have to worry about childcare. We were young so the odds of unexpected medical care were lower. All things considered, it was pretty easy to keep our Now Money to a minimum with plenty to spare for Life Money.

This allowed us to fuel our Later Money goals, like having a nice wedding and saving up for a home or rental property. We had money in the bank and seemingly endless choices.

And, I didn’t want to screw it up.

Which brings us back to me sitting on the beach, thinking about what I would do with financial freedom, with maybe 1 or 2 less beverages in the cooler.

What did I really want out of life?

I put my book down and looked off into the ocean, thinking about what I wanted out of life. I started thinking about what my ideal life would look like. By this point, I was engaged in the type of deep thought where you don’t even realize what’s happening around you.

It quickly occurred to me that I had never truly thought about what I wanted in life. Sure, I had thought about things like having a family and being able to take vacations.

But, I never carved out time to purposefully think hard about what I actually wanted. I had never asked myself what truly motivates me.

Without a doubt, I had never written down the answer to that powerful question: what would I do with financial freedom?

I hadn’t ever allowed myself to dream about financial freedom.

The truth is, I don’t think I had ever visualized a life that wasn’t dominated by a full-time job. Up to that point, my whole life had revolved around getting an education and then getting a job. I never pictured a world where I might not need a full-time job to provide for myself and eventually my family.

I had read about the concept of being financially free, but it always seemed like a possibility for other people, not me. Writing this years later, I feel sad for that version of myself for having such limiting beliefs.

That said, I completely understand why I felt that financial freedom was unattainable for someone like me. This was in the phase of my life where I had been preoccupied with eliminating debt. Because of that debt, I didn’t allow myself to dream about what life could look like if money wasn’t holding me back.

This was also before my wife and I had rental properties. It was before we recognized the impact of side hustles and multiple streams of income. I had read about and understood these concepts in theory, but I hadn’t put what I learned into practice.

That day on the beach, it was like a light went on in my head.

After years of patience and discipline, I had climbed out of debt. I was now a DINK with Later Money in the bank waiting to be deployed. That meant I had created opportunities.

I wasn’t financially free, but for the first time in my life, I allowed myself to accept that financial freedom was possible for me.

This was one of the most powerful moments in my life.

With that realization in my mind, I walked into the ocean to cool off and think some more.

What would I do with financial freedom?

There in the ocean, I wasn’t thinking about dollars or career goals. This was more important than that. I was thinking about what I wanted my life to look like if money was not an issue. I was thinking about what I would do with my time if I was in complete control.

Floating there in the water, it was like I had an epiphany. Everything suddenly became clear to me. I ran out of the ocean to get back to my chair before I forgot what just popped into my head.

I whipped out my top bound spiral notebook and started writing with a blue pen. Minutes later, I had written down seven answers to the question: what would I do with financial freedom?

My “Tiara Goals” were born.

Nearly eight years later, I still have that sheet of notebook paper. I keep it safe in a leather binder protected by a laminated page holder. It has those familiar tear marks on the top of the page where the paper connected to the spiral binding.

Even though I have these seven goals memorized by now, I still look at this sheet of paper every month. Looking at this sheet is an incredible reminder of that day on the beach when everything became clear to me.

A quick aside, I call my goals “Tiara Goals” because it’s a silly, but meaningful, description to me. Have some fun with what you name your goals. If you do it right, you’ll be thinking and talking about these goals a lot.

What are my Tiara Goals?

So, here are my original Tiara Goals from 2017, as scribbled on that sheet of paper and edited for clarity:

Be with my wife and kids as much as I want. Dad never missed a game. Mom never missed a game. Nana never missed a game.

Not be forced to commute to work on Friday or Tuesday or whatever day, if I need that day for myself.

Choose how to spend my working hours (representing clients, teaching, volunteering, building a business, etc.).

Continue to study and learn constantly.

Take at least one big trip every year.

Never turn down an exciting or smart opportunity because I can’t afford it.

Work alongside people that value my contributions.

Keep in mind that I wrote these goals before I had kids and before I was even married. This was also years before the pandemic when working from home was a foreign concept to most of us.

I think it says a lot that I was thinking about these things way back then.

In a future post, we’ll unpack each of these goals.

While I haven’t reached financial freedom yet, I think I’m doing a pretty good job already living by these fundamental values.

We can obtain Parachute Money. We can choose to do meaningful work and choose to spend more time with people who are meaningful to us.

No, it’s not easy to achieve financial freedom. But, it is a whole lot easier when you know what you are striving for in the first place.

That’s why at the beginning of my financial wellness class, I ask my students to write down their own versions of Tiara Goals. I want to help them avoid the limiting beliefs that I had before that day on the beach.

My favorite part of class is when my students share their Tiara Goals.

Without a doubt, this is always my favorite part of class. When I say I’m on a mission to convince you that talking money is not taboo, I think of my students sharing their goals. I get so energized by hearing their goals. My students report the same sentiment after learning what drives their friends and peers.

Over the years, my students have shared countless impactful stories. As unique as these goals can be, it’s remarkable how most of us want the same things in life. Year after year, I hear the same motivating forces:

Spend more time with my family.

Travel and enjoy experiences around the world.

Stay healthy and fit.

Provide for my children and my aging parents.

Work for a cause I believe in.

Have time to volunteer.

I also regularly hear one thing that my students, and the rest of us, don’t want:

Be specific, but not too specific, when you think about financial freedom.

When we talk about what we do with financial freedom in class, I encourage my students to get specific without being so precise that the goal becomes restrictive. When we’re thinking about goals related to financial freedom, the idea is to focus more on big-picture, core values.

There will be a time and a place to strategize how to get there. The point here is to help define what you’re even trying to get in the first place.

For example, instead of “spending more time with family,” I would suggest something like, “never miss my child’s soccer game or dance recital because of work.”

Instead of “travel around the world,” I would suggest “at least one overseas trip of at least 2 weeks per year.”

Adding that little bit of specificity will help you visualize what you’re striving for with your money decisions.

Don’t get discouraged if you think you are not close to financial freedom.

Even when you feel like financial freedom is only a distant dream for you, it’s important to actively think about what you want out of life. I’d even suggest that the further away you feel from financial freedom, the more important it is to think about what it would mean for you.

When you’re at your lowest point, visualizing what you would do with financial freedom is a helpful escape.

If you haven’t ever actively thought about what you would do with financial freedom, hopefully this post will encourage you to do so.

Don’t forget to write down whatever you come up with.

I suggest you share your version of Tiara Goals with your friends and loved ones. It’s OK to keep some of your goals private. By sharing, you will get the benefit of them cheering you on. You’ll also hopefully encourage them to share their goals with you, which can be very inspiring.

Have you thought about what you would do with financial freedom?

Have you ever written it down or shared your answers with others?

8 out of 10 people! Is it just me, or is that mind-boggling?

On the flip side, only 4% of workers report no concerns about losing their jobs.

These numbers are shocking to me, but maybe I shouldn’t be that surprised. As Yahoo Finance explains,

Many large corporations have already announced or kicked off a round of layoffs, including Chevron, CNN, Estee Lauder, Meta, and Southwest Airlines. And that, of course, doesn’t count the thousands of workers terminated under Elon Musk’s campaign to reduce the federal workforce.

My mind immediately jumps to a follow-up question:

Surveys like this one motivate me to continue bringing attention to core personal finance issues, like having adequate emergency savings. This is why I so strongly believe that talking about money is not taboo.

Life is too short and too precious to be in a constant state of worry. Is there any sense worrying about something, like getting laid off, when you have practically no control over whether it happens or not?

Nearly half of US workers choose to work more days than they are required to!

And, it gets worse if you’re a high earner or highly educated.

According to the same study, the more money you earn, the less likely you are to take your full paid time-off.

The more educated you are, the less likely you are to take your full paid time-off.

The more senior you are, like being a manager vs. non-manager, the less likely you are to take your full paid time-off.

If the first survey mentioned above surprised me, this one just makes me angry.

Do you recognize a difference between working hard and always working?

Don’t misunderstand why these results make me angry. It’s not about working hard vs. slacking off. It’s not about being a good employee vs. a bad employee. I am 100% in favor of people working hard and working with integrity to get the job done.

My frustration is that somewhere along the way, “working hard” turned into “always working.”

By the way, before you accuse me of being a slacker, I am no stranger to working hard.

I work full-time as a lawyer, manage 11 rental properties, teach law school courses on Wednesdays and Sundays, and publish three blog posts per week. Still, none of these things are more important to me than spending quality time with my family.

Years ago, I first read Tim Ferris’ game-changing book, The 4-Hour Workweek. Ferris described how his small business took off as soon as he started doing less, not more. He empowered his staff and stopped himself from getting in the way. Not only did his company thrive, he had more time available to pursue what really mattered in his life.

If you’re one of these people choosing to work more hours instead of taking your earned vacation time, have you ever asked yourself why?

Keep in mind, these are days off that your company has already agreed to give you. You earned them. Why are you not taking them?

Are you worried about getting fired? Passed up for a promotion? Is your self-worth tied to how many hours per week you work?

Years from now, when your grandkids are huddled up for story time, do you plan on telling them how much you worked and how many life experiences you skipped out on?

These are hard questions to truthfully answer. If you’re being honest with yourself, you may start thinking about another set of questions:

Is this job the right job for me? Do I want to spend my life stressed from working too much? What would be a better use of my working hours so I can spend more time doing the things that I love with the people that I love?

I’ve spent a lot of time thinking about these questions. I’ve realized that I’ll never understand what the point is of working so much at the cost of spending time with the things and people you love.

Maybe I’m the weird one. But, I don’t think I am. Unfortunately, the data backs me up and confirms that working too much can have series consequences.

Fortunately, we can learn from strategies geared towards retirees. Let me explain.

The tips include finding a purpose, strengthening your body, and rebuilding your brain.

When I came across this story, I immediately thought that we shouldn’t wait for retirement to do these things. This is solid advice for all of us, at any stage in our lives.

Do you know what sounds pretty great to me?

A life filled with purpose sounds pretty great. The same goes for being fit and smart.

The challenge is that work often gets in the way.

When we let this happen, the consequences can be catastrophic.

As just one example, lawyers as a profession have long struggled with mental health issues. I first learned about these challenges during law school orientation. Today, I see it in practice. Being a lawyer is a hard way to make a living. When you work as a lawyer, the hours are intense and stress levels are consistently high.

In 2023, the Washington Post analyzed data from the U.S. Bureau of Labor to determine what the most stressful jobs are. The study confirmed that lawyers are the most stressed.

Of course, lawyers are not alone in struggling in this regard due to long, stressful hours. The same study showed that people working in the finance and insurance industries were right up there with lawyers as being highly stressed.

Anecdotally, I’ve personally talked to people recently in a wide variety of other fields, like consultants and small business owners, who are frustrated for the same reasons.

The point is, regardless of industry, many of us struggle with work stress.

What can we do about it?

That’s a complicated question with many possible answers. For starters, I firmly believe that by building strong personal finance habits, we can create more opportunities to find purpose and practice good health.

I recommend you think back to our conversations about Parachute Money and why you should want to be good with money. When you’ve made thoughtful money choices, you can choose to live a life right now on your terms rather than waiting until retirement.

I agree with what you’re probably thinking. These are not easy or fun topics to think about. However, in my opinion, it’s much worse to let life go by while failing to take responsibility.

Am I wrong about people working too much?

Maybe I’m wrong about people working too much?

I don’t think I am.

The data paints a very sad picture for lawyers, and I have to believe anyone else working long and hard hours. If you have similar data about your profession, please share it with us. I hope I’m wrong about what that data will show, but I fear I’m right.

As always, let us know what you think in the comments below.

And, thank you for continuing to share stories you’ve come across that would be good to discuss here.

We’ve all heard these common money phrases. If you were to ask someone older than you for one piece of personal finance advice, I’m betting you’ll hear one of these lessons. Let me know if I’m right about that in the comments below.

There’s a reason these phrases are so common. They’re simple and easily reflect some of our core personal finance principles. In fact, we’ve covered these concepts in detail in earlier posts:

It’s not that we want to have high debt and low savings. So why is this the reality for so many of us?

I have 3 main theories why we fall into debt.

There are countless theories on why people end up in debt. I have three primary theories. Looking at each of these explanations can help us understand and avoid common pitfalls that lead us into debt.

1. We fall into debt because we are simply careless.

Like many people, I failed to create a budget and assumed that my W-2 income was plenty. I ignored emergency savings and never even thought about creating Parachute Money.

The saddest part is that I didn’t even realize that I was slipping backwards. I had no idea because I didn’t track my net worth or savings rate. I worked hard all year long and just hoped things would work out.

By the way, if this sounds familiar, you should know by now I’m not judging anyone. I’ve been very open about my money mistakes. We all deserve a chance to learn about and talk about strong personal finance habits.

So, being careless with money is one common reason people fall into debt. Another common reason is that bad things happen in life.

This might include medical emergencies, home repairs or car troubles. It’s not our fault that these things happen. But, it is our fault if we’re not prepared in advance.

While these events are unfortunate, and maybe even tragic, they are not unexpected. We all need to expect that bad things will happen.

Preparing for the unexpected is part of every solid organization’s planning. In government, planning ahead means having a “rainy day fund.”

When managing properties, planning ahead for big repairs means having a “Capital Expenditures” or “Cap Ex” fund. For our personal finances, planning ahead means having an emergency fund.

Whether it’s government, business, or personal finance, the goal is to have options other than taking on debt to get through challenging circumstances.

3. Blame the Kardashians.

Besides carelessness and emergencies, there’s another powerful force that contributes to rising debt levels across the world. This force is nearly impossible to ignore. It’s become a part of our daily lives, whether we want to admit it or not.

What is this powerful force that contributes to our rising debt levels?

The era of social media and on-demand entertainment has made it harder than ever to avoid temptation. It’s everywhere we look.

Blaming the Kardashians realtes to another timeless, common money phrase: “Keeping up with the Joneses.”

The Kardashians are the modern day Joneses.

Once upon a time, “the Joneses” represented your neighbors, people you could observe from a distance on a regular basis. The idea behind the phrase is that you can see what your neighbors are spending money on and are either consciously or subconsciously tempted to do the same.

If your neighbors buy a new car, you buy a new car to keep pace. If your neighbors vacation in Australia, you research diving tours at The Great Barrier Reef. When you notice your neighbors hosting a backyard BBQ party with lots of happy looking people, you decide to host a party the next weekend.

As humans, it can be difficult to ignore the temptation to keep up with our neighbors. Whether we like it or not, we are concerned with our social status. Part of our self-worth gets tied to comparing ourselves to others.

Who better to measure up against than the people in our neighborhood who we probably have a lot in common with?

This same idea is oftentimes compounded in the professional setting. It is not uncommon to compare ourselves in the same way to our colleagues at the office.

Some professions heighten the pressure to keep up. Have you ever noticed that real estate agents seem to always drive nice cars? Or, big city lawyers wear fancy suits? It’s easy to get caught up in expensive tastes when you’re expected to fit in.

One of my favorite personal finance books, The Millionaire Next Door, discusses this concept in detail. I highly recommend you read this book if you are struggling with comparing yourself to others.

What does this all have to do with the Kardashians?

In today’s world dominated by social media and the internet, we’re no longer influenced just by our neighbors or colleagues. We’re now influenced by people throughout the world. That could mean friends or complete strangers.

Instead of just learning your neighbors went on vacation, now you know when anyone in your circle is on a trip. At any moment, you may be on the train in 12 degree weather heading to work. One look at your phone and you’ll see plenty of wonderful pictures of people doing cool things. It’s hard to not want that for yourself.

The byproduct of social media and the internet is the never ending temptation to spend money. Even if that means spending money we don’t have. That’s a powerful force pushing us deeper into debt.

I am fighting this temptation in my life right now. Having moved to a new home not long ago, there are so many things we want to buy and projects we want to do. I need to constantly remind myself to slow down so I don’t again fall victim to consumer debt.

Instead, the first part of the solution is to recognize when you’re making careless money decisions based on what you think other people are doing.

Making money decisions based off of your neighbors, let alone the Kardashians, is the fast road to debt. You have no idea why or how another person is spending money. For all you know, it’s all for show and that person is barely getting by.

Do you really want to blindly follow this person’s choices? Wouldn’t it be better to confer with people you trust to help you think through money decisions?

The second part of the solution is to recognize that everywhere you look, companies are clamoring for your dollars.

If you let that reality sink in, you’ll hopefully pause the next time you’re about to spend money on something you don’t actually care about.

This is where we circle back to money mindset.

To counteract social media and mass marketing, you need to have a competing force in your life that’s strong enough to overcome all the noise.

I’m referring to your ultimate goals in life. I mean the reasons you wake up every morning to go to a job or stay up late to finish a project.

Why are you working so hard?

When you can answer that question, you’ll know what your ultimate goals are in life. With those goals in the forefront of your mind, it’s much easier to make consistent, intentional money decisions.

Most importantly, you’ll stay on budget and avoid sinking into debt.

You’ll also be much happier when you stop worrying about what random strangers are spending money on.

The only thing that’s taboo is avoiding your personal finances.

To help flip the script and convince you that talking money is not taboo, I plan to regularly post about the current money conversations that I’m having. Through my examples, I hope to encourage you to have similar conversations.

In our first “Great Talk” post, we’ll discuss what my wife and I decided to do with our Later Money throughout 2025. We’ll also talk about how really smart people I know have started budgeting. We’ll conclude with an empowering conversation I had with a friend about what you can do with your time if money wasn’t an obstacle.

What I’m doing with my Later Money in 2025.

Later Money is what you are saving, investing, or using to pay off debt. This bucket includes long term goals and investments, like retirement and college savings. It also includes emergency savings, paying off debt, or any other shorter term goals, like saving for a wedding or a downpayment for a house.

So, what are my wife and I doing with our Later Money in 2025?

We recently had a great talk about our options and came up with a plan that will guide us throughout the year. Before we talk about our 2025 goals, it’s important to keep in mind that your Later Money goals will change over time. That’s perfectly fine.

We purchased our first rental property in 2018, a four-flat in an up-and-coming Chicago neighborhood. Less than a year later, we bought a three-flat in the same neighborhood.

In 2021, we invested in a Colorado rental ski condo. In 2022, we purchased our fourth rental property, a three-flat, in the same (now booming) neighborhood in Chicago.

After living in our rental properties since 2018, we purchased a single-family home just outside Chicago in 2024.

During this timeframe, any spare dollar we earned went towards acquiring more real estate. We contributed towards other financial goals, like retirement and college, but our priority was investing in real estate.

Reading Small and Mighty Real Estate Investor helped my wife and I conclude that at this point in our lives, we have enough. If anything, we’re closer to having too much on our plate. We self-manage our 10 units in Chicago and work closely with a property manager in Colorado. With our full-time jobs and kids at home, we’ve bitten off as much as we can chew.

Our portfolio generates enough income to help fuel our current goals. If we were to continue expanding, the headaches could end up outweighing the financial benefits.

We want to build a life full of experiences and memories. That means we need more time, not more money. Acquiring and managing more properties right now would take up a lot of time. That tradeoff is not currently worth it to us.

So, if we’re not pursuing additional properties in 2025, what are our goals?

After talking it through together and weighing all our options, my wife and I came up with these three goals for 2025:

Our third goal is to boost our contributions to our kids’ college savings accounts. We use what’s called a “529 college savings plan.” 529 plans are state-sponsored, tax-advantaged investment accounts. We use Illinois’ 529 plan because we receive a tax break as Illinois residents. Just about every state offers a 529 plan. They are a great way to save for college.

With our plan in place ahead of time, we now know where every dollar is going before we earn it. This takes the anxiety out of trying to figure it out after the money has already hit our bank account.

At the end of each month, all we need to do is make our Later Money transfers to each account. We can rest easy knowing that we’re making progress towards our personal finance goals.

How Budgeting is Helping Very Smart People.

One of my favorite moments since launching Think and Talk Money occurred just last week. Walking down the hall in my office, one of my colleagues called me over.

She was very excited to share that she started tracking her spending so she can create a Budget After Thinking.

We chatted for ten minutes. She’s been reading the blog on her commute to work every Monday, Wednesday, and Friday. She used Think and Talk Money vocabulary, like “Now Money” and “Life Money.”

She showed me the app she’s been using to track her spending, one I wasn’t familiar with and am now looking into. The best part was that she’s been telling her friends about Think and Talk Money because she’s already learned so much.

This is exactly why talking about money is not taboo. She taught me something new and helped me think about my own budgeting process. She gave me new ideas to think about.

How could this type of conversation be bad?

We didn’t need to talk numbers. We talked strategy and habits. That’s what talking money is all about.

What would you do with your time if money was not an obstacle?

I had lunch with an old friend last week at a downtown Chicago lunch spot that’s been serving up epic burgers since the 1970’s. My friend and I are both balancing careers as lawyers in Chicago with young families at home.

In between bites of a massive BBQ-bacon-cheeseburger, I asked him a question I like asking smart people:

“What would you do with your time if money wasn’t an obstacle?”

Without hesitation, he answered that he would work with his hands. He likes working on projects around the house. He gets immediate satisfaction from completing a repair or making an improvement.

His answer was great and very relatable. My years as a landlord has taught me the same feeling of satisfaction in completing a project.

What stood out to me the most was how quickly he answered the question. He knew exactly what he would do if money was not an obstacle.

This simple question helps illustrate what I mean when we talk about financial independence. It’s not an easy goal to accomplish, but I can’t think of a better goal to strive for.

You are financially independent when money is not an obstacle.

In this week’s Q&A, we talk about how the timing was right to launch Think and Talk Money, why you should consider a side hustle, and what comes next for the website.

As always, please email your questions or leave a comment below or on socials.

You have a lot on your plate. Lawyer, teacher, landlord, young kids… why launch Think and Talk Money now?

I had been thinking about writing a book or starting a website for a couple years. Over the holidays, my dad gave me the final push I needed.

We were casually chatting while the kids played in the other room. Out of nowhere, he said, “Matt, you should do it.”

Do what?

“You should write a book.”

Oh, no biggie.

I didn’t expect him to say that. He went on to explain how you get to a certain age and you look back on life and wonder where it all went. You think about all the things that you wanted to do but never got around to doing.

No regrets, blogging then book.

He knew I had been thinking about writing a book for a while and didn’t want me to regret not doing it.

I thought about it and realized he was right. I would never forgive myself if I didn’t take this chance.

Now that I’ve thrown this out there, I have to do it, right?

There’s never a perfect time in life. If I didn’t start Think and Talk Money now, I might never have gotten around to it. Something always comes up. It’s too easy to make excuses.

It’s true we have a lot going on. Fortunately, I had a system already in place that gives me time to write thanks to Hal Elrod’s The Morning Miracle.

I hesitate to say a certain book “changed my life.” This might be one of them.

For almost 10 years now, I’ve been waking up at 5:30 a.m. to read, journal, and relax. It’s so beneficial to have that time for myself, especially now with kids, before the day gets away from me.

Since launching Think and Talk Money, I use my mornings to blog instead of reading. I like teaching and writing about personal finance, so my mornings are still enjoyable.

We’ll spend some time in a future post talking about all the advantages of having a side hustle.

The obvious advantage is you can make more money. The important thing is what you do with that money to make the side hustle worth it. A side hustle is another time commitment, after all. If you’re going to take on the responsibility, make sure it counts.

Before you consider a side hustle, have a plan in place for why you want additional money. Are you looking to pay down debt faster? Save for a wedding? Invest in your first rental property?

One of my favorite experiences teaching personal finance to law students involved a side hustle. A couple of years ago, a student approached me during a break and told me about his credit card debt. It had been weighing heavily on him.

After our discussion about side hustles, he committed himself to driving for DoorDash and using the income to pay off his credit card balance.

Six months later he sought me out to share that the plan worked. His side hustle allowed him to pay off his credit card in less than six months. All while working a full-time job and attending law school par-time. I couldn’t have been happier.

To help you think through why you might want a side hustle, check out these three posts:

BTW, you’re not too busy or important for a side hustle.

Some people reading this will automatically think, “I’m way too busy to even think about another job.”

In my personal finance class for law students, we spend a lot of time challenging that notion. Very few people- and I mean very few- are too important or too busy to take on a side hustle.

You may think you’re one of those “too important” people. I would challenge you to assess whether you’re confusing “too important” with “too stressed.”

Setting that conundrum aside, the ideal side hustle is something you enjoy doing that can earn you extra money at the same time. Some examples my students have come up with in class include:

Bartending. Entice your friends to come to your bar by offering cheap drinks. You get to hang out with them and get paid at the same time.

Fitness instructor. Instead of paying $48 for the spin class you love, become the instructor and get paid to lead the class.

Dog Walker. If you love dogs and don’t currently have one of your own, what better way to fill that void in your life while making money. The same applies to babysitting.

Home Baker. Make homemade treats with your kids and sell them to parents who don’t have the time.

I’m reminded of another conversation my dad and I had when I was in high school.

Growing up, my siblings and I were busy kids. Sports, clubs, performances, classes, you name it. I made a remark to my dad about it at one point.

He responded that being busy wasn’t a bad thing because you don’t have time to fool around. When you have no choice other than to stay focused, you actually perform better in all facets of life.

You’re not thrown off by distractions because you’re locked in on accomplishing your goals.

After launching Think and Talk Money, I feel a heightened sense of focus. It’s benefitting me in all of my pursuits. I take care of business as best I can, while prioritizing my family and my health.

I can see your eye rolls through your screen.

This guys is nuts. He’s a workaholic.He has no life.

Have you ever used a HELOC to invest in real estate?

Yes, I’ve used HELOCs, which stands for Home Equity Lines of Credit, to scale my real estate portfolio.

This question leads to so many concepts we need to discuss, from debt and credit to investing. We’ll come back to HELOCs more fully in a separate post.

The bottom line is using HELOCs to scale your investment portfolio is a more advanced strategy that I would not recommend for everyone. I probably wouldn’t recommend it for most people, even experienced real estate investors.

I say that for good reason. When you hear HELOC, think debt. For many of us, debt is problematic and leads to negative emotions.

If you satisfy all of the above, a HELOC may be useful to scale your real estate portfolio. If you’re thinking about using a HELOC in the near future and want to talk it out, please feel free to reach out.

What’s it like being a blogger?

It’s only been five weeks, but I’m happy I took the chance to launch Think and Talk Money.

It’s been fun.

And, it’s been hard.

First, the fun stuff. I’ve enjoyed writing and talking about personal finance concepts that are important to me. I’ve especially enjoyed all the interactions with our readers.

One unexpected element I’ve appreciated is the sense of accomplishment that comes with publishing every post. This is very different from my experience as a lawyer where we typically work on a case for years before its conclusion.

I’ve also had fun writing in a new style. I haven’t ever blogged before. I haven’t done any writing other than legal writing since college. If you’ve ever had the pleasure of reading a legal brief or court opinion, first off, I’m sorry. Second, you understand how different legal writing is from blog writing.

Even though the writing styles are different, there is certainly some overlap in the fundamentals. My aim in both styles of writing is to be clear, concise, and informative. I hope to be somewhat interesting, as well.

As a blogger, I’m still finding my voice, as they say.

It can be challenging to make core personal finance concepts- like budgeting and saving money- educational, simple, and entertaining. If I’m doing my job, then my personal finance content should also be relatable and understandable.

Please let me know you have any feedback on what’s working (or not working for you)!

So, what’s hard about blogging?

Now, for the hard stuff.

My wife and I launched Think and Talk Money with zero knowledge, skills, or experience in starting a website.

Can you tell? Be nice.

We have no tech background whatsoever. Two months ago, I had no idea what SEO, caching, or plugins were.

If you’ve ever started a website, you know exactly what I mean. Creating the content is only the first step. So much more goes into it behind the scenes. We’re still only scratching the surface.

To sum it up, the tech stuff has been challenging and time consuming. We’ve learned so much already but have so much more to learn.

Thank you to everyone who has reached out with tips and suggestions!

What’s the end game for Think and Talk Money?

I completely understand why this is an important question to think about. The truth is we’re just getting started and haven’t thought about Think and Talk Money in terms of an end game.

I’ve always liked to teach and write, and this lets me do more of both. For now, our mission is to introduce the most important concepts of personal finance through the blog.

We post three times per week on Mondays, Wednesdays, and Fridays.

Some of the posts cover core personal finance topics in depth. Other posts are more targeted and address specific strategies or lessons.

There’s an intentional order to the way we’ve been introducing concepts. The order is important and mirrors the curriculum in my personal finance class for new lawyers.

Let’s start with recent news that impacted me personally.

A reminder to consistently evaluate your banking relationships.

For a long time, I used Capital One for all my savings accounts. When I started law school in 2006, there was a Capital One cafe right next to my school. You could get a cup of coffee for $.75 and talk to a banker at the same time. It was a cool concept and convinced me to bank with Capital One.

I told everyone about how great Capital One was. I had Capital One savings accounts and a Capital One credit card. You could say I was a huge Capital One fan.

One day that November, for whatever reason, I logged into my Capital One account to see what rate I was earning. I was sure it would be in the 4% range, and probably closer to 5%, since Capital One was a leader in online banking.

When my statement loaded, I was shocked.

0.30%!

Shocked probably isn’t the right word. I was disgusted.

0.30% in 2023 might as well have been 0.0%… from a bank that had been a leader in online savings accounts that I had banked with for 17 years.

What the heck happened?