In a recent paper called “Giving Up”, authors Seung Hyeong Lee and Younggeun Yoom examined a troubling trend in younger generations.

The authors found that because home ownership has become so expensive, many younger generations have given up on the idea altogether.

Whether you want to own a home is not the main takeaway. We can debate the merits of home ownership all day long.

The main takeaway of the article is something far worse than that.

The authors hypothesize that the high cost of home ownership has impacted young people’s overall outlook on work, spending and life.

Because people don’t think they can afford to own a home, they shift their entire behavior when it comes to money. The authors project that:

[Those] born in the 1990s will reach retirement with a homeownership rate roughly 9.6 percentage points lower than that of their parents’ generation. The model also shows that as households’ perceived probability of attaining homeownership falls, they systematically shift their behavior: they consume more relative to their wealth, reduce work effort, and take on riskier investments.”

More consumption?

Less work effort?

Riskier investments?

Do these projections raise any red flags for anyone else?

The authors go on to explain their thesis. Goals like purchasing a home, paying for college, or saving for retirement require sustained effort over the long-term. However, these goals are getting harder to attain due to rising costs for homes and childcare, not to mention inflation.

The problem with these goals being so hard to reach?

As the authors explain:

[W]hen such goals become exceedingly difficult and are perceived as beyond realistic reach, households may cross a threshold at which they begin to give up on them entirely. Unfortunately, this abandonment of major life goals is becoming increasingly common world-wide, particularly among younger generations.

According to the Harris Poll’s 2024 State of Real Estate Survey,1 42% of Americans and 46% of Gen Z respondents agreed with the statement, “No matter how hard I work, I will never be able to afford a home I really love.

No matter how hard I work, I will never be able to afford a home I really love.

If the authors are correct in their theory, this is a troubling article.

Should we give up on personal finance education?

When I first read this article, I immediately thought about a law student in my personal finance class a few years ago.

After the course, she wrote to me that the material we covered will never apply to her. She explained that she already had too much debt and will never earn enough to think about saving and investing.

She had already resigned herself to living paycheck to paycheck in a perpetual struggle to get by. In the end, she wrote, personal finance education would never matter for her.

At first, I was shocked by her perspective. She was about to graduate law school and had endless potential in front of her. Why was she so pessimistic about the future? Sure, it would take some time and effort to pay off her loans, but there was a path forward.

After a few more years of teaching, I realized that she was not alone in her concerns. The only thing different about her was that she was vocal and honest about her money fears. I’ve come to learn that a number of my students have the same worries:

High education debt.

Rising costs of housing and other consumer goods.

Incomes that have not kept up.

I can understand why some people give up when the odds seem so stacked against them.

Of course, I know that some people are beyond convincing that personal finance education is crucial to their overall well-being. I get trolled on socials all the time by people with this type of mentality.

So, while I understand the anxious money mindset, I’m not even close to giving up on young people having a solid financial future. This is especially true when it comes to young lawyers.

Now, when I read articles like this, I am more motivated than ever to teach personal finance to lawyers.

Being a lawyer is a hard job.

It’s no secret that our profession is a challenging one.

I know plenty of lawyers who make a lot of money. That doesn’t mean they’re good with money. Far from it.

This is a problem because our profession can be very taxing. We tend to work long hours under stressful conditions.

This means time away from our families. It means less time available to exercise, cook healthy meals, and sleep. You already know how important these things are to a healthy life.

Sadly, the nature of our profession means that lawyers have high rates of alcohol abuse and depression.

In a prominent study, the American Bar Association and the Hazelden Betty Ford Foundation found rates of alcohol abuse and depression among lawyers are among the highest of any career field in the U.S.

Studying nearly 13,000 attorneys, the authors concluded:

Substantial rates of behavioral health problems were found, with 20.6% screening positive for hazardous, harmful, and potentially alcohol-dependent drinking. Men had a higher proportion of positive screens, and also younger participants and those working in the field for a shorter duration…

Levels of depression, anxiety, and stress among attorneys were significant, with 28%, 19%, and 23% experiencing symptoms of depression, anxiety, and stress, respectively.

The authors further concluded:

Attorneys experience problematic drinking that is hazardous, harmful, or otherwise consistent with alcohol use disorders at a higher rate than other professional populations. Mental health distress is also significant.

As a lawyer, and someone who comes from a big family of lawyers, these conclusions terrify me.

Which is a major reason why personal finance education is so important for lawyers.

Some of the personal finance challenges have changed, but the fundamentals remain the same.

For lawyers, high student debt loads and other financial pressures are certainly among the reasons for our personal challenges.

The thing that gets me the most is when people give up at the very beginning of the journey, sometimes before the journey has even started.

Whether we like it or not, money touches all aspects of our lives. Why give up on learning about money instead of learning how to use it for the tool that it is?

If learning personal finance sounds appealing to you in light of the challenges we face, here are three steps to help you get started.

Step 1: Foster a positive money mindset.

The first step is to foster a positive money mindset. Without establishing why you want to be good with money, none of the specific skills and recommendations will matter.

This first step is essential and will help any young lawyer who is thinking about giving up on the future.

In my blog, I write regularly about money mindset. You can learn all about developing a strong money mindset by reading my posts here.

Additionally, if you are interested in checking out one of my favorite money mindset books, you can find my top recommendations here.

Step 2: Find out where all your money is going.

The next step is to evaluate where your money is actually going each month. Once you know where your money is going, you can come up with a realistic plan that moves you closer to reaching your financial goals.

I call this process a Budget After Thinking.

Having a Budget After Thinking is crucial for not giving up on your future financial goals. You would be amazed at the confidence you can build if you can stick to a simple plan for your money.

For a step-by-step guide on how to create a Budget After Thinking, read my post here and follow-up posts here and here.

You might be wondering what makes my budget process different from any other budget.

My budgeting philosophy is premised upon your actual spending habits and realistic adjustments.

In other words, forget about aiming for predetermined, generic goals like saving 20% of your income.

I’ve taught enough law students and lawyers to know that these rigid, predetermined targets don’t work.

With massive student loan debt and soaring costs of living, generic savings targets just don’t work.

If you aim for some predetermined amount, you’ll end up cutting out everything you like spending money on to the point where you will resent your budget. Then, you’ll give up on your budget and fall back to your old habits.

The beauty of creating a Budget After Thinking is that it is based upon a baseline budget of your actual, current spending habits.

In evaluating your current habits, you can then make thoughtful and realistic adjustments to that budget that will actually last. Through this process, you can accomplish the main goal of generating more fuel for your ultimate financial goals.

And that leads us to the third and final step to begin establishing strong personal finance skills to prevent you from giving up before you get started.

Step 3: Use financial calculators for concrete motivation.

Online Calculators are some of the most powerful motivational tools for developing financial wellness.

Check out our Think and Talk Money calculators for concrete motivation to allocate more of your monthly income to your financial goals.

When you play around with these calculators, you will quickly see how even seemingly small adjustments to your Budget After Thinking will pay massive dividends in the long run.

Remember, the goal of your Budget After Thinking is to generate more fuel for your future goals. What exactly does that mean?

This is where using a good financial calculator pays off.

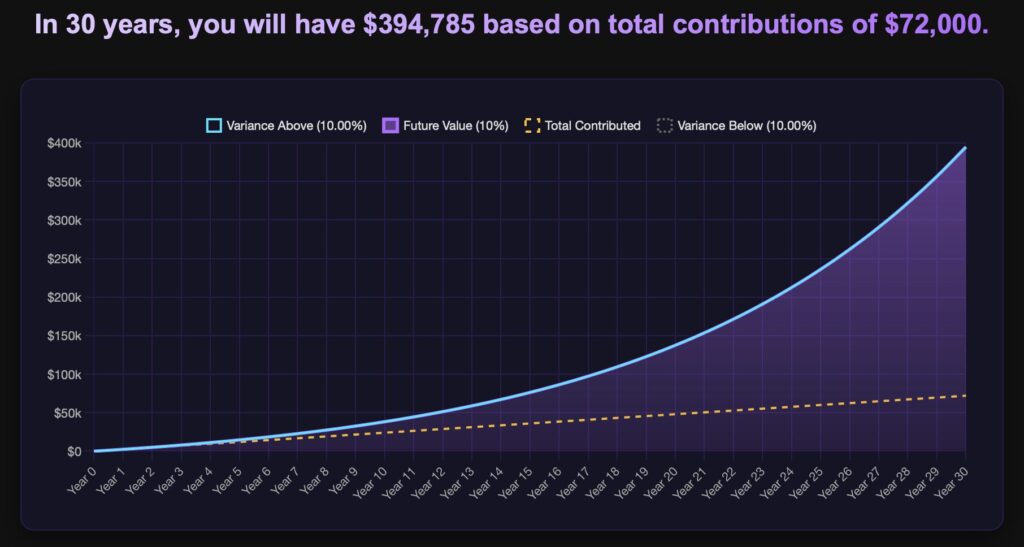

For example, let’s say you cut $200 of spending per month and invested that money in an S&P 500 index fund with average historical returns of 10%.

Look at the results using the Think and Talk Money Compound Interest Calculator:

If you invested just that $200 each month for the next 30 years, you would have $394,785!

And, that’s based on contributing only $72,000 of your own money. The rest is interest you earned for doing nothing.

Take a second to let that sink in: You’d have nearly $400,000 in your investment account all because you created a Budget After Thinking.

If that doesn’t motivate you to make some thoughtful adjustments to your spending, I don’t know what will.

Now is the perfect time to invest in your financial education.

If you’re thinking about giving up on your future goals, there’s no better time than now to invest in your financial education.

Whether we like it or not, money touches every facet of our lives.

When you take control of your money, you’ll see that your productivity at work improves.

Your relationships outside of work will improve.

I’d even go so far as to say that you’ll start to believe in yourself more. You may even find the courage to follow a different path in life you hadn’t previously explored.

By the way, if most of your peers are giving up, think of the opportunities out there for anyone willing to learn personal finance.

If less people are motivated to work hard, imagine what a strong work ethic can do for you.

If less people are looking to buy a home, think about the homes that might be available if you make it a goal to buy one.

When other people spend and spend in the present day, think of the foundation you can build by investing in the future.

Yes, there are some of us who will give up and never try to build for the future because of these present day challenges.

You could be one of those people.

Or, you can make it more of a priority to build your financial foundation.

After all the years you’ve spent in school to earn the right to practice law, my gut tells me you’re the type of person willing to put in the work.

Don’t give up on your financial future.

Invest in your personal finance education and thrive when others quit.