Let’s take a deeper dive into the two most common strategies for paying back debt when you have multiple loans: Debt Snowball v. Debt Avalanche.

In our post on how to confidently tackle debt, we discussed that it’s a smart idea to apply one of these strategies. Here, we’ll see why.

You’ll notice we have lots of charts and numbers in this post. Don’t worry, you don’t need to do any math. I’ll show you how to use a simple online calculator to help you decide with strategy is best for you.

Before we look at the strategies, always keep in mind the number one rule:

Always pay the minimum required amount on every loan no matter what.

Whatever strategy you end up using, always pay the minimum payment on every loan. If you fail to do so, you will be charged penalties and your credit history and score will be negatively impacted. You will also accrue interest on those penalties, compounding your mistake.

Don’t worry if this sounds confusing right now. We’ll discuss credit cards and the responsible use of credit in detail in upcoming posts.

The below strategies apply to any excess funds you have left after paying at least the minimum on every loan balance. No matter what, you need to make the minimum payment on each loan every single month.

What is the Debt Snowball method?

The first strategy is known as “Debt Snowball.” When you apply the Debt Snowball strategy, the idea is to focus on the loan with the smallest balance first, regardless of interest rate.

Remember, these strategies are for helping you pay back multiple loan balances.

Once you have paid off the first loan in full, you move to the loan with the next smallest balance, again regardless of interest rate. The money you had been paying to the first loan can now be rolled into the second loan.

What is the Debt Avalanche method?

The second strategy is referred to as Debt Avalanche. With this method, you will prioritize the loan with the highest interest rate, regardless of the balance.

Once you’ve paid off the loan with the highest interest rate, you move to the loan with the next highest interest rate. Just as before, the money you had been paying to the first loan can now be applied to the second loan.

You can apply either of these strategies in the same way no matter how many loans you have.

The first step in choosing a debt payoff strategy is to gather some basic information on each loan that you have.

For each loan, you’ll need to find the outstanding balance, the interest rate, and the minimum required monthly payment. You can pull this information from your most recent monthly statement.

Once you have this information, you can plug the numbers into a simple online calculator. By doing so, you’ll get an idea of how much it will cost you (in terms of time and money) to pay off these debts.

I like using calculator.net.

They have calculators for all sorts of different purposes, including a Debt Payoff Calculator. Using the Debt Payoff Calculator, you can decide the best payoff strategy for your personal situation.

You may prefer the quicker emotional wins that come with the Debt Snowball method. Or, you may prefer the savings that come from the Debt Avalanche method.

There’s no wrong answer. The choice is yours.

Let’s see how Debt Snowball and Debt Avalanche work in practice.

Note, for simple illustration purposes, the minimum payments in these examples remain the same throughout the life of each loan.

Example 1: Two Different Credit Card Balances

Imagine you have two credit cards with balances owed.

Credit Card 1: $5,000 balance with a 15% interest rate and a minimum required payment of $150 per month.

Credit Card 2: $10,000 balance with a 20% interest rate and a minimum required balance of $200 per month.

| Balance | Rate | Min. Pay. | |

| Credit Card 1 | $5,000 | 15% | $150 |

| Credit Card 2 | $10,000 | 20% | $200 |

After creating a Budget After Thinking, you’ve determined that you have $1,000 per month to put towards these two loans. Because you have to pay a minimum of $150 to Credit Card 1 and $200 to Credit Card 2, you have $650 left to deploy.

How should you do it?

Debt Snowball

If you apply the Debt Snowball approach, you prioritize paying off the loan with the smallest balance. That means paying $800 to Credit Card 1 ($150 minimum payment plus $650 remaining funds) until that loan is paid off completely. The remaining $200 needs to be applied to cover the minimum payment on Credit Card 2.

Once Credit Card 1 is paid off completely, you will add that $800 payment to Credit Card 2 for a total payment of $1,000.

| Balance | Rate. | Min. Pay. | Snowball | |

| Credit Card 1 | $5,000 | 15% | $150 | $800 |

| Credit Card 2 | $10,000 | 20% | $200 | $200 |

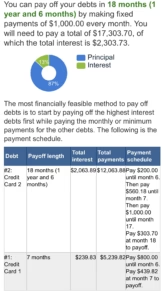

Using calculator.net, you’ll see that it will take you 18 months to eliminate both loans with the Debt Snowball approach. It will cost you a total of $17,303.70, of which the total interest is $2,303.73.

Importantly, Credit Card 1 will be completed paid off in 7 months.

Debt Avalanche

Now, let’s see what happens when we apply the Debt Avalanche approach. Under this approach, you would prioritize Credit Card 2 because it has the higher interest rate. That means you would pay $850 to Credit Card 2 and only the $150 minimum payment to Credit Card 1. Once Credit Card 2 is paid off, you would pay the full $1,000 to Credit Card 1.

| Balance | Rate | Min. Pay. | Avalanche | |

| Credit Card 1 | $5,000 | 15% | $150 | $150 |

| Credit Card 2 | $10,000 | 20% | $200 | $850 |

Using calculator.net, you’ll see that it will take you 18 months to eliminate both loans with the Debt Avalanche approach. You’ll end up paying a total of $17,071.84, of which the total interest is $2,071.87.

It will take you 14 months to eliminate the first loan, Credit Card 2.

Now, we can compare the results of using Debt Snowball or Debt Avalanche.

Under the Debt Snowball approach, you’ll pay $231.86 more in interest. It will take you 18 months to eliminate both debts under each approach.

However, under the Debt Snowball approach, it will only take you 7 months to completely erase one loan. Under Debt Avalanche, you will not erase the first loan until 14 months have gone by.

Now that you have this data, you can decide whether you prefer Debt Snowball or Debt Avalanche. Some people may prefer the emotional win of eliminating one loan completely after 7 months using the Debt Snowball method.

Other people will prefer the Debt Avalanche approach, which results in more savings. The tradeoff is that they won’t eliminate any loans completely until month 27.

As we said before, there is no right or wrong answer. It is entirely a matter of personal preference.

Why not just pay the same amount to each credit card?

If you pay $500 to each credit card from the beginning, let’s see what happens:

| Balance | Rate | Min. Pay. | Equal | |

| Credit Card 1 | $5,000 | 15% | $150 | $500 |

| Credit Card 2 | $10,000 | 20% | $200 | $500 |

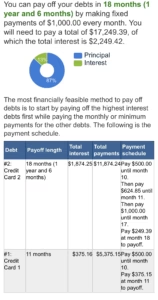

You will end up paying off both loans in 18 months and paying a total of $17,249.39, of which the total interest is $2,249.42. You won’t eliminate any loans completely for 11 months when Credit Card 1 is paid off.

Compared to the Debt Snowball approach, splitting the payments evenly means four more months to pay off the first loan completely. That means you’re waiting longer for your first emotional win.

Compared to the Debt Avalanche approach, you’ll end up paying $177.55 more in total interest. If you’re looking to maximize your savings, splitting payments is not the way to go.

As you can see, whatever your preference is, it makes sense to pick either Debt Snowball (fastest emotional win) or Debt Avalanche (most money saved).

Personally, I prefer the Debt Snowball approach.

I prefer the Debt Snowball approach because of the emotional win that comes with eliminating a debt in less time, sometimes even twice as fast.

That victory is more important to me than saving $231.86 spread out over 18 months (the length of time it takes to eliminate both debts).

If you prefer paying the least amount in interest, I won’t argue with you. There’s nothing wrong with saving money. It’s a personal choice.

That said, there is one instance where I prefer Debt Avalanche to Debt Snowball.

If you have Bad Debt, like credit card, always pay that debt first.

Bad Debt typically has significantly higher interest rates than other forms of debt, like student loans, auto loans, or mortgages.

Compare these current (February 2025) average interest rates for various types of loans:

It’s not hard to see that credit card debt comes with a significantly higher interest rate than any other form of common debt.

This is why I recommend you always pay your credit card debt first.

Let’s look at a second example to illustrate this point.

Example 2: Auto Loan and Credit Card Balance

Auto Loan: $8,000 balance with an interest rate of 5% and a minimum required payment of $50 per month.

Credit Card: $20,000 balance with an interest rate of 20% and a minimum required payment of $400 per month.

| Balance | Rate | Min. Pay. | |

| Auto Loan | $8,000 | 5% | $50 |

| Credit Card | $20,000 | 20% | $400 |

Just as before, you’ve determined that you have $1,000 per month to put towards these two loans. Because you have to pay a minimum of $400 to your credit card and $50 to your auto loan, you have $550 left to deploy.

How should you do it?

Debt Snowball

If you apply the Debt Snowball approach, you would prioritize paying off the loan with the smallest balance. That means paying $600 to your Auto Loan until that loan is paid off completely. The remaining $400 needs to be applied to cover the minimum payment on your credit card debt.

Once the auto loan is paid off completely, you will add that $600 to the credit card debt for a total of $1,000.

| Balance | Rate | Min. Pay. | Snowball | |

| Auto Loan | $8,000 | 5% | $50 | $600 |

| Credit Card | $20,000 | 20% | $400 | $400 |

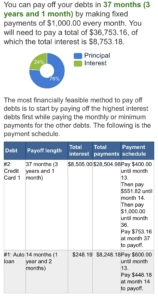

Using calculator.net, you’ll see that it will take you 37 months to eliminate both loans with the Debt Snowball approach. It will cost you a total of $36,753.16, of which the total interest is $8,753.18.

Importantly, the auto loan will be completed paid off in 14 months.

Debt Avalanche

Now, let’s see what happens when we apply the Debt Avalanche approach.

Under this approach, you would prioritize the credit card loan because it has the higher interest rate. That means you would pay $950 to the credit card and only the $50 minimum payment to the auto loan. Once the credit card is paid off, you would pay the full $1,000 to your auto loan.

| Balance | Rate | Min. Pay. | Avalanche | |

| Auto Loan | $8,000 | 5% | $50 | $50 |

| Credit Card | $20,000 | 20% | $400 | $950 |

Using calculator.net, you’ll see that it will take you 34 months to eliminate both loans with the Debt Avalanche approach. You’ll end up paying a total of $33,822.14, of which the total interest is $5,822.17.

It will take you 27 months to eliminate the credit card debt.

We can again compare the results of using Debt Snowball and Debt Avalanche.

Under the Debt Snowball approach, you’ll pay $2,931.01 more in interest. It will also take you three months longer to eliminate both debts.

On the plus side, your auto loan will be completely paid off in 14 months, which is nearly twice as fast as with Debt Avalanche.

Some people may still prefer the emotional win of eliminating one loan completely after 14 months using the Debt Snowball method.

For me, the price of that emotional win has gotten too expensive. I would prefer to save the $2,931.01 and have both loans paid off in less time, even if that means waiting longer to pay off a single loan.

If you do this exercise with any normal credit card compared to another form of loan, you’re likely going to find that the credit card interest rates are so high that you should target those loans first.

Do you prefer Debt Snowball or Debt Avalanche?

As we said before, there’s no right or wrong answer. Money decisions are emotional. Paying off debt is the perfect example.

Using a simple online calculator can help you make the best decision for your situation. All you need to do is find the balance, interest rate, and minimum payment for each of your loans and the calculator will do the rest.

Whichever method you choose, stick with it. Save yourself the stress of doing mental gymnastics each month.

The most important thing is that you are making your payments every month.

Have you used Debt Snowball or Debt Avalanche?

Which method do you prefer?

Let us know in the comments below.