Money goals are all about having a plan ahead of time so your dollars don’t disappear.

If I could synthesize all of personal finance into one message, that would be it.

Make a plan. No disappearing dollars.

This is essentially all that budgeting is.

Put a little effort into learning where your money is going. Then, evaluate whether you need to make any adjustments. I call this a Budget After Thinking (BAT) .

Having a BAT in place ahead of time means you know where every dollar is going before you earn it. At the end of each month, all you need to do is make your transfers to each account.

That’s how you stay on budget with only two simple numbers.

Focusing on just two numbers, you can rest easy knowing that you’re making progress towards your personal finance goals.

This takes the anxiety out of trying to figure it out after the money has already hit your checking account.

And, it eliminates the risk that the money sits in your checking account and slowly disappears because of mindless spending choices.

The bottom line is that if you don’t have a plan in place, it’s going to be very difficult to accomplish your goals.

As 2025 winds to a close, I wanted to share how I did with my money goals this year.

Here are the three money goals my wife and I came up with in early 2025:

- Pay off the HELOC debt. Our first goal was to continuing paying down HELOC debt that we used to help acquire some of our rental properties. Now that we’re not actively looking for more rentals, we’re focused on paying back these loans.

- Build up our emergency savings. Our second goal was to build up our emergency savings. We mostly ignored our emergency savings between 2017 and 2024 as we focused on buying investment properties. It was risky and led to some touch-and-go moments that we’d like to avoid moving forward.

- Fully fund college for our second kid. Our third goal was to boost our contributions to our kids’ 529 college savings accounts. We have three kids. We previously hit our savings goal for our first kid. This year, we were focused on our second kid.

In the end, I did not accomplish two of my three money goals.

Does that make 2025 a failure?

No way!

This year was far from a failure. It might have been our best year ever. I’ll explain below.

What’s interesting is the goal we did achieve was the lowest priority of the three at the beginning of the year. I’ll talk about that, too.

Before we get to that, I want to first talk about failure.

Failing to complete a goal does not make you a failure.

I realized years ago that failing to complete a goal does not mean that I am a failure. Goals are about making progress, not just the end result.

If you put in the effort and make progress toward a desired result, any progress should be viewed as a success.

In theory, we all know this.

Here’s an example:

Think about a woman who sets a goal to finish a 10k in less than an hour. She’s never run that far or that fast before.

She trains for months in pursuit of her goal. It’s not easy. There are training runs she wants to skip. Her legs ache and her body is sore. But, she sticks with it.

On the big day, she gives it her all and finishes the race in one hour and 2 minutes.

Two minutes too slow.

Is she a failure because she didn’t finish in less than an hour?

Of course not.

This woman ran further than she’s ever run before. She’s stronger and more fit than she was before training.

On top of that, she now has a new baseline to start from. She can evaluate her process and learn from what she accomplished.

If she wants to, she can sign up for another 10k with all the knowledge and improved fitness she gained this time around.

By just about every measure, she’s a success. Goals are about the process and not just the result.

Keep this little example in mind when you review your own goals.

We are harder on ourselves than we are with other people.

Throughout life, we tend to be harder on ourselves than we are on other people. This is especially true when we fall short of accomplishing all of our goals.

I want to encourage you to reframe how you evaluate your goals. Instead of focusing just on the result, think about how far you progressed from where you started.

This part can be difficult.

Years ago, I would get down on myself for not hitting all of my targets. It took some time to realize that even when I didn’t hit my target, I still had a successful year.

Here’s a personal example, sticking with the running theme.

A few years ago I made a goal to run 500 miles for the year. In the end, I ran something like 460 miles.

At first, I was very hard on myself. I concluded that I failed because I did not reach 500 miles.

Then, I evaluated why I fell short.

I realized that I was making great progress before I was sidelined with an injury for a couple of months. I did my best to make up for the lost time but couldn’t quite recover.

Looking back, the fact that I got close and didn’t give up entirely was a good thing, not a failure.

I was proud that I continued to make progress, even after a setback.

By the end of the year, running 460 miles was an accomplishment despite falling short of the ultimate goal.

Nowadays, this is exactly how I evaluate all of my goals, whether they’re fitness goals, money goals or any other type of goal.

I set ambitious targets knowing that I might not hit them.

If I don’t complete all my goals, I don’t let myself think that I’m a failure.

Instead, I evaluate my progress and the actions I took to reach my target. If I fall short, I try to understand what happened so I can learn for next time.

Sometimes, I fall short because I made an unrealistic goal. Other times, it might just be that I got close but not all the way across the finish line.

There have also been times when my goal was simply a bad goal, meaning something I didn’t actually care about.

Regardless, I review my motivation and my effort so I can recalibrate for the following year.

With this process in mind, let’s take a look at how I did with my 2025 money goals.

How did I do with my 2025 money goals?

I failed to achieve my three money goals for 2025.

But, this year was not a failure.

Not even close.

As I look back on my 2025 money goals, I’m thrilled with my progress.

1. Pay off the HELOC debt.

For years, my wife and I used HELOCs to help acquire rental properties. Now that we’re not actively looking to acquire more properties, our goal is to eliminate this HELOC debt.

Admittedly, this was a very ambitious goal to accomplish in one year. Especially considering the other two goals on this list.

In the end, we paid off 71% of our HELOC balance.

While not the end result we targeted, I’m happy with this outcome. Any year that you eliminate 71% of a debt burden is a tremendous year.

Because we made major progress on this goal in 2025, I anticipate that at our current saving rate, we’ll have the HELOC debt fully paid off by the end of 2026.

It will be an incredible feeling to have this debt load off of our shoulders. We’ve been carrying it for too long now.

Once this debt is eliminated for good, I can focus on more fun goals. I can watch my accounts grow, instead of just seeing debt shrink.

That excites me.

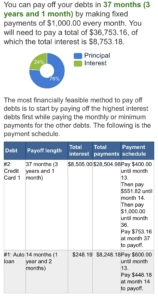

How to pay off debt on a budget.

By the way, I don’t regret using HELOC debt to help purchase investment properties and build our portfolio.

That said, at this stage in my life, I’m ready for that debt to be gone.

If you are similarly working towards paying off debt, check out my top 10 strategies for paying off debt on a budget:

My top 10 strategies for how to pay off debt on a budget.

- Write down your Tiara Goals.

- Create a Budget After Thinking so the debt stops growing.

- Prioritize Later Money funds for debt.

- Apply our Top 10 strategies for staying on budget.

- Talk to your people about paying down debt.

- Track your net worth and saving rate for small wins.

- Pick a strategy and stick with it: Debt Snowball v. Debt Avalanche.

- Think about loan consolidation.

- Get a side hustle.

- Don’t let yourself fall backwards.

Throughout the year, I was focused on prioritizing funds for debt, using the debt snowball approach, and not letting myself fall backwards.

For a deep dive on each of the 10 strategies, check out my full post on paying off debt on a budget:

2. Build up our emergency savings.

Your emergency savings account is the most important savings account in personal finance. I like to refer to emergency savings as Parachute Money.

My goal is to have four months of living expenses saved up in my Parachute Money account.

Why four months?

Most personal finance experts recommend three to six months. Much of it depends on your current income situation and overall comfort level.

I have income from my primary job, rental properties, and part-time teaching. Taking all that into account, four months of emergency savings feels like the sweet spot to me.

So, how did I do with this goal?

Well, it was another “failure” that I don’t view as a failure at all.

When it comes to emergency savings, my challenge has been that I’ve been so focused on eliminating HELOC debt that this goal has typically been pushed aside.

This year, I set out to make emergency savings more of a priority.

I’m happy to share that for the first time in a few years, we now have an emergency savings account with 1.5 months of living expenses.

It’s not the four months we targeted, but once again, we made good progress.

By the end of 2026, this is another goal that we should be able to check off because of what we accomplished this year.

3. Fully fund college for our second kid.

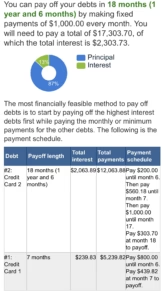

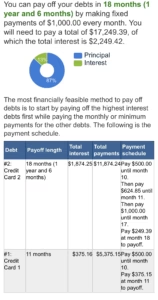

Using the Think and Talk Money 529 College Savings Calculator, I figured out how much money we would need to invest this year in our son’s 529 savings account to fully fund his college.

The 529 Savings Calculator showed us that with investments of $37,972 this year, we could fully fund his in-state tuition at the University of Illinois (our premier in-state university).

Here’s what the results look like from the calculator:

When my wife and I saw these results, we realized that we could make it happen, if we made it a priority.

So that’s what we did.

We made it a priority to fully fund our son’s college account.

And, I’m happy to report that we completed this goal.

The tradeoff was that we did not make as much progress on our HELOC debt or our emergency savings.

The funny thing is this was the lowest priority goal of ours when the year started.

In the end, it’s the only one we accomplished. How did that happen?

Well, our emotions took over.

This is an example of why I always say that money is emotional.

When my wife and I chose to fund our son’s college savings account, we knew that would mean we’d fall short on our other goals.

We were more than OK with that tradeoff.

My wife and I received a powerful emotional boost by prioritizing our son’s college. We can now cross this item off the “to-do” list once and for all.

See, most “financial experts” would have advised us to eliminate our debt and build an emergency savings before targeting college savings for our kids.

Well, most experts ignore that money is emotional.

We don’t live in a spreadsheet.

When my wife and I talked about doing this for our little boy, the decision was easy.

There’s nothing we wouldn’t do for him. I smile every time I think about what the future may have in store for him.

How did you do with your 2025 money goals?

As you look back on your 2025 goals, don’t beat yourself up if you didn’t reach your ultimate target.

We all need to give ourselves some grace. Any and all progress is an accomplishment and something to build upon.

As you look ahead to 2026, evaluate what you learned about yourself in 2025.

Soon, I’ll share my 2026 money goals. You can already guess my first two goals: eliminating the HELOC debt once and for all and hitting that 4-month emergency savings target.

If you’ve never set money goals before, my process might help you get started.

How did you do with your 2025 money goals?

What did you learn about yourself?

Let us know in the comments below.