Money Mindset

-

How the Jay Leno Rule Turbocharged my Net Worth

The Jay Leno Rule might be the best money strategy that I’ve used to increase my net worth on my way to financial independence.

-

Ignore Courthouse Stock Tips: Start with the Fundamentals

Don’t make the mistake of thinking that “personal finance” means “investing.” Yes, investing is important. But, it’s not where personal finance begins.

-

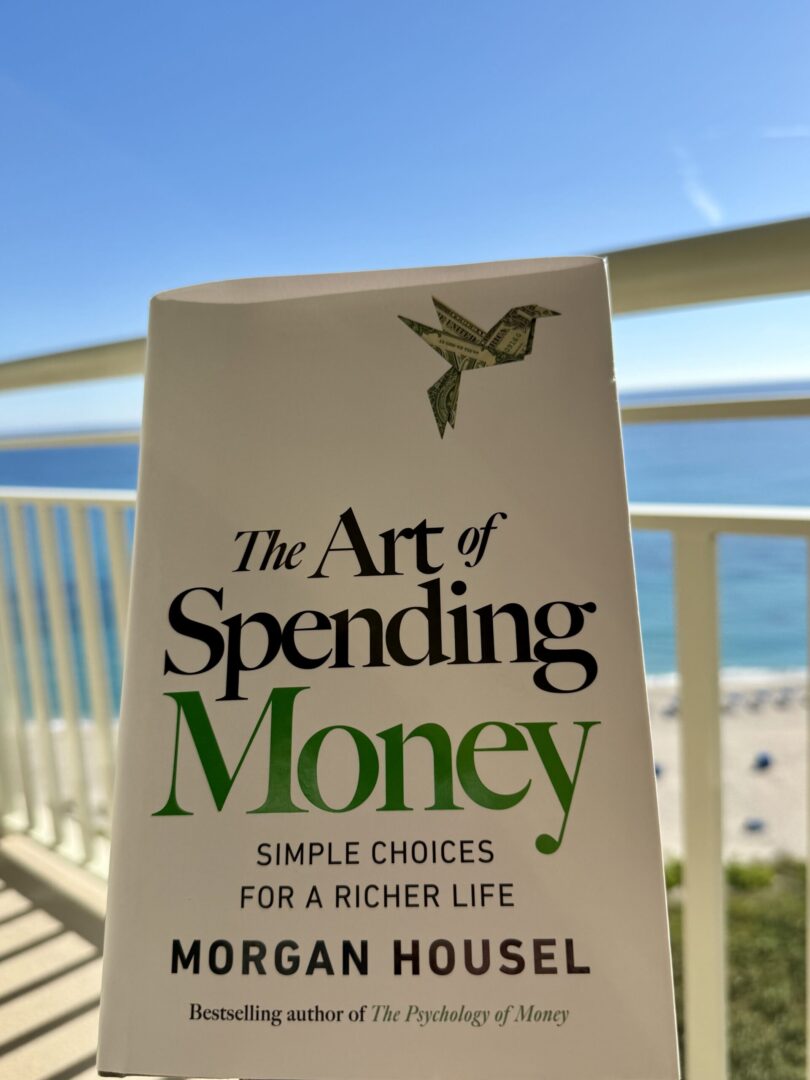

Read The Art of Spending Money by Morgan Housel

The Art of Spending Money encourages us to think individually and spend money on what matters the most to us, not what matters to other people.

-

Money is Just a Tool: My 2026 Money and Life Goals

What I love most about teaching personal finance is the interconnection between money and life. With that in mind, here are my money and life goals for 2026.

-

You Use GPS But You Don’t Track Your Net Worth?

Tracking your net worth is easy using the new TATM Net Worth Tracker™️. You wouldn’t drive without GPS. Don’t go through life without knowing your net worth.

-

Failing to Reach a Money Goal Does Not Make You a Failure

When evaluating your goals, don’t focus on just the result. I “failed” to reach 2 of my 3 money goals this year. And, this year was an unequivocal success.

-

Why Wouldn’t You Want to be Good With Money?

A lot of lawyers make good money but are not good with money. That’s a problem. Financial wellness touches all parts of life, which makes it an essential skill.

-

Why it’s Important to Invest in Your Financial Wellness

We get so caught up in how to invest that we ignore the obvious choice: investing in ourselves. When you invest in yourself, the potential returns are infinite.

-

Year End Checklist: Make Your Charitable Contributions Now

If you are a W-2 employee, consider making additional charitable donations in 2025 if you want to reduce your taxable income.

-

Make Money by Playing The Game of Big Expenses

Play The Game of Big Expenses to turn negative money experiences into positives by negotiating the cost and then investing the difference.

-

Why It’s So Important to Learn Personal Finance

Personal finance education, whether through a blog, a course, or coaching, should be a constant in your life so your money choices align with your true values.

-

Practice Strong Money Fundamentals Before Investment Dreams

In my personal finance course, I teach my students that before they dream about huge investment returns, they need to build a strong money foundation.

-

That’s a Wrap: Another Successful Personal Finance Seminar

After completing another personal finance seminar with a great group of law students, I feel energized to use my money as a tool to build a life I’m proud of.

-

Spend Money Based on Your Wealth Not Your Income

Instead of spending money based on your income, spend money in line with your wealth. Income is temporary, even for high earners. Wealth is your foundation.

-

A Reminder About the Intersection of Money and Life

Money is only a tool that we should all use to build memories and create stories. I recently had a good reminder of this intersection between life and money.

-

How Much Money Did You Actually Keep This Week?

When was the last time you really appreciated how much effort you put into making money? Shouldn’t you actually keep a lot of that money?

-

Are You Making Progress on Your 2025 Money Goals?

Don’t wait until the end of the year to revisit your money goals. Now is the perfect time to check your progress to ensure you hit your mark.

-

Should You Invest in Chicago Real Estate Right Now?

You should base your decision on where to buy real estate on the available data, common sense, and your personal experiences. That’s why I invest in Chicago.

-

Did You Win the $1.787 Billion Powerball Jackpot!?

Didn’t win the jackpot? You should still take this chance to think about what you would do with a major windfall so you’re prepared when the time comes.

-

Financial Independence is Not About a Life of Deprivation

There is way more to financial independence than cutting costs and living frugally. I view FI as creating options to get more of what I want in life, not less.

-

When Money is Tight, Think Even More About The Future

When money is tight, that’s the best time to think about your future self. Use those challenging periods as motivation to make hard spending decisions today.

-

Coast FIRE Will Help You Realize When Enough is Enough

Coast FIRE can help you know when enough is enough. Instead of chasing money for retirement, you can pivot to a life now that better matches your interests.

-

How to Gain Confidence by Calculating Your Coast FIRE Number

Gain confidence in your progress towards retirement by calculating your Coast FIRE number. You may be pleasantly surprised by this powerful money mindset hack.

-

Why Coast FIRE is a Powerful Money Mindset Hack

When you achieve Coast FIRE, retirement planning is no longer an issue. That means you have options to pivot to a job that better fits your life goals.

-

Capital One Settlement: A Reminder to Evaluate Your Bank

The recent Capital One class action settlement is a reminder to always evaluate your banking relationships to ensure your bank is still a good fit for you.

-

The Best Ways to Come Up with a Rental Property Down Payment

Here are my best tips for coming up with the down payment for a rental property, which is the biggest impediment to investing for lawyers and professionals.

-

Dreaming About Rental Properties but Ignoring Money Mindset?

To come up with the money to buy rental properties, start with revisiting your money mindset and the key personal finance fundamentals.

-

Does Being Good with Money Make You a Greedy Dragon?

Being good with money does not make you a greedy dragon. When you’re good with money, you can build a meaningful life of experiences with your family.

-

Being Good with Money is About Consistent Choices

Being good with money takes consistent choices. Too many of us give up on our money goals just as we’re getting started. That’s why talking about money helps.

-

Money Questions: How to Handle the New Student Loan Changes?

Whether it’s changes to federal student loans or any other recent developments, I encourage you to plan accordingly and take ownership of your money decisions.

-

Money on My Mind: Read The Simple Path to Wealth

The Simple Path to Wealth by JL Collins is the best book I’ve read on investing. Collins teaches us the simplest and most effective way to earn massive wealth.

-

Money Question: What Would I do with $10 Million?

Readers recently shared what they would do with $10 million. One reader asked what I would do. So, here’s what I would do, and wouldn’t do, with $10 million.

-

What if You Woke up Tomorrow with $10 Million?

I love asking people what they would do if they woke up with $10 million in the bank. It’s another way to think about what you would do with financial freedom.

-

Money on My Mind: Bears, Net Worth and Exercise

On my journey to financial freedom, I’m consistently striving to learn as much as I can from other bloggers and writers who have done it before me.

-

What is the Best Money Mindset Book?

A great money mindset book will motivate you to use money to build a life you’re proud of. These are my favorites from my journey to financial freedom.

-

Money on My Mind: Read Millionaire Milestones

Millionaire Milestones by Sam Dogen is the Goldilocks of personal finance books. He’s not only done it all in personal finance, he’s still doing it.

-

Great Talk: Money, Baby Blue, and Friends

The best money I’ve spent lately was on a tree and a friend. I felt a triple happiness boost each time, which reminded me of the tie between money and emotions.

-

Money on My Mind: Financial Literacy Month

April is National Financial Literacy Month. Think and Talk Money readers don’t need a recognized money month. We think and talk about money throughout the year.

-

Happy that I Delayed Financial Independence

I’m happy that I delayed financial independence to build the life that I truly want. By house hacking for seven years, I can now clearly see the finish line.

-

FIPE not FIRE: Financial Independence, Pivot Early

Instead of FIRE, I believe in FIPE: Financial Independence Pivot Early. With FIPE, the goal is not to withdraw, but to pivot to more meaningful work.

-

My Journey to Financial Freedom

My journey to financial freedom began 15 years ago. I’ve learned that the journey to financial freedom for lawyers and professionals does not happen over night.

-

The Biggest Money Question: What is Your Money Why?

Have you thought about what it could mean for you and your family if you are good with money? I was recently reminded of why I want to be good with money.

-

Money on My Mind: Global Happiness

Happiness is tied to the freedom to choose what you do with your life. This is why financial freedom is so important when striving for a happy life.

-

Great Talk: Money and Fences

Talking to your people is a great way to help make financial decisions, whether you’re replacing a fence or starting a budget.

-

Powerful Money Lessons from Alone

We can learn about personal finance by watching Alone. Not all dollars are created equal, attitude is everything, and family is so important.

-

My Path to Financial Freedom with Tiara Goals

Have you ever asked yourself what you would do with financial freedom? Thinking about that question on a beach in 2017 opened my eyes to what truly mattered.

-

Money on My Mind: Always Working?

Do you work too much? It’s a simple question that most of us don’t want to answer. Let’s discuss the potential consequences of always working.

-

Buy a Home Now or Wait for Mortgage Rates to Drop?

Why you shouldn’t wait on interest rates to buy a home and why I personally wouldn’t hesitate to buy the most expensive home in a neighborhood.

-

Big Decisions are Easier with Parachute Money

Parachute Money is a powerful personal finance concept. When you have Parachute Money, you are financially free to control your life, not the other way around.

-

Great Talk: Money, Friends and Cheeseburgers

Talking about money is not taboo. Learn from the personal finance conversations I’m currently having. Including, one empowering chat over cheeseburgers.

-

Money Truth: It’s Not Taboo to Talk About Money

I’m flipping the script with personal finance. Talking about money is not taboo. The only thing that’s taboo is avoiding your personal finances.

-

Q&A: Look for a Valuable Side Hustle

In this week’s Q&A, we discuss how the timing was right to launch Think and Talk Money, why you should consider a side hustle, and what comes next.

-

Money on My Mind: Capital One Edition

Here, we discuss Capital One’s alleged deceptive practices, rising credit card balances, and how life experiences may impact the amount we save for retirement.

-

Strong Motivation to Talk Money with Friends

Talking about money with your friends is no different than talking about exercise, travel, books, or food. No need to talk numbers, focus on strategy.

-

Better at Making or Keeping Money?

To invest, you need available money. To have available money, you need a budget that actually works combined with honest life motivations.

-

Help a Professor Out: Ask Your Money Questions Here

Think and Talk Money’s motto is “Money Wellness Together.” The more we all talk, the more we all benefit. Ask questions so we can keep the conversation going!

-

You will Easily Know and Feel Money Well Spent

Talking money is really just talking life. I would not trade my Cubs memories for anything. Learn to keep the experiences without the worries.

-

You Should Want to be Good with Money

You should want to be good with money. Money can give you choices. Money can give you personal power. Money can give you time.

-

How to Think About Money and Italian Beef

Instead of convincing ourselves that we’re not worried about money, let’s get energized thinking about what money can do for us.

-

I’m Matt Adair. This is my Financial Freedom Blog for Lawyers

I started a financial freedom blog because I want us to go to our people to talk about money, just as we would talk about anything else.