Debt

-

How the Jay Leno Rule Turbocharged my Net Worth

The Jay Leno Rule might be the best money strategy that I’ve used to increase my net worth on my way to financial independence.

-

Failing to Reach a Money Goal Does Not Make You a Failure

When evaluating your goals, don’t focus on just the result. I “failed” to reach 2 of my 3 money goals this year. And, this year was an unequivocal success.

-

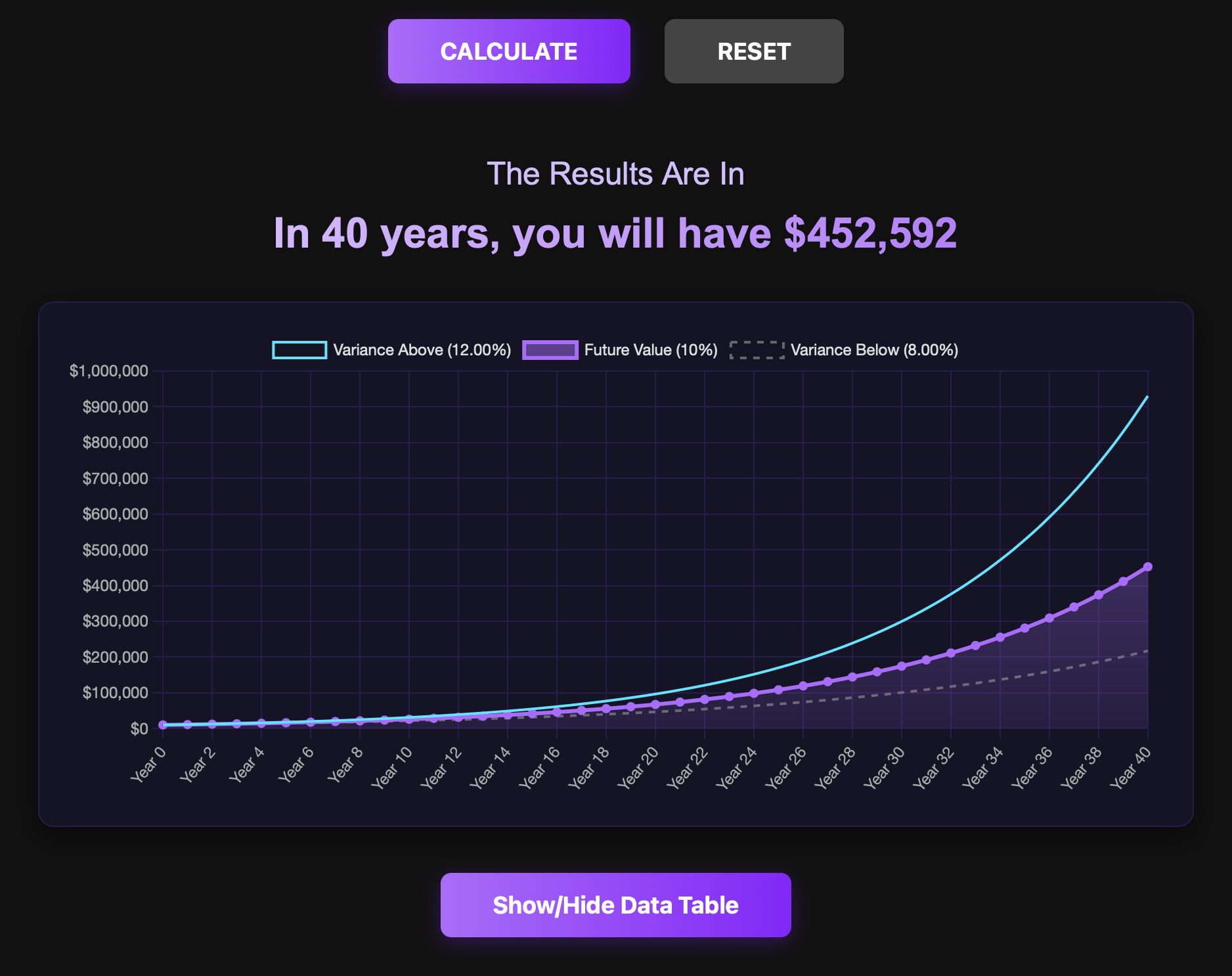

Use a Calculator to Help Make Big Money Decisions

Financial calculators are powerful motivational tools. Use the Think and Talk Money calculators to make decisions, like what to do with a $10,000 bonus.

-

Make Money by Playing The Game of Big Expenses

Play The Game of Big Expenses to turn negative money experiences into positives by negotiating the cost and then investing the difference.

-

That’s a Wrap: Another Successful Personal Finance Seminar

After completing another personal finance seminar with a great group of law students, I feel energized to use my money as a tool to build a life I’m proud of.

-

Top 10 Tips to Pay Off Debt for Lawyers and Professionals

If you make six figures and have bad debt, your income is not the issue. You need a plan. Here are 10 tips to pay off debt for lawyers and professionals.

-

How to Make a Budget to Pay Off Debt in 3 Steps

If you have credit card debt, your number one money goal should be to get rid of it. To help you out, here’s exactly how to make a budget to pay off debt.

-

Don’t Blame Your Income if You Are a Lawyer in Debt

If you’re a lawyer in debt, the problem is not your income. You make plenty of money. Here are three theories why lawyers are in debt and what to do about it.

-

Furloughs Show Why You Need Savings and Parachute Money

Furloughs remind us to focus on emergency savings and parachute money for multiple layers of protection in case our primary source of income dries up.

-

Are You Making Progress on Your 2025 Money Goals?

Don’t wait until the end of the year to revisit your money goals. Now is the perfect time to check your progress to ensure you hit your mark.

-

Debt is Really Annoying When you Want to Buy Fun Things

Debt can be really annoying when you want to buy fun things. But, it’s important to stay disciplined while on your journey to financial freedom.

-

Money Questions: How to Handle the New Student Loan Changes?

Whether it’s changes to federal student loans or any other recent developments, I encourage you to plan accordingly and take ownership of your money decisions.

-

Invest in Real Estate and Other People Pay Your Debt

Besides cash flow and appreciation, the next main reason I invest in real estate is because other people pay off my debt through monthly rent payments.

-

Money on My Mind: Read The Simple Path to Wealth

The Simple Path to Wealth by JL Collins is the best book I’ve read on investing. Collins teaches us the simplest and most effective way to earn massive wealth.

-

How to Prioritize Investment Account Types While in Debt

How to prioritize investment account types, especially if you’re paying off debt, is another tricky money question. Here’s exactly what I would do.

-

How to Think About Investing While in Debt

Whether to invest while in debt is a tricky question. I like to do both for these reasons, using 75% of my available funds for debt and 25% for investments.

-

Top 10 Student Loan Tips for Lawyers and Professionals

Student loans are just heavy. To help get rid of that weight as efficiently as possible, here are my 10 student loan tips for lawyers and professionals.

-

The Time is Now: Student Loan Basics

With student loans, don’t let outside factors stop your progress towards financial freedom. Learn the basics about student loans so you can make a plan.

-

Student Loans and Financial Freedom

Debt from student loans and financial freedom go hand-in-hand. My wife and I talked about paying off my student loans before marriage. I’m so glad we did.

-

Is Debt Snowball or Debt Avalanche Better?

Debt Snowball and Debt Avalanche are the two most best strategies to efficiently pay down multiple debts. I prefer Debt Snowball for the faster emotional wins.

-

How to Realistically Pay Off Debt on a Budget

Paying off debt takes patience and a plan. Here are my Top 10 strategies for how to pay off debt on a budget as efficiently and painlessly as possible.

-

How to Responsibly Use Good Debt

There may not be a more polarizing debate in personal finance than the concept of Good Debt vs. Bad Debt. Learn why I believe in the power of Good Debt.

-

Three Big Reasons Why You’re in Debt

Too many of us are in debt. Looking at my three main theories why people get into debt can help us understand and avoid these common pitfalls.

-

Scary Stats to Know About Debt to Help You Get Out of It

8 out of 10 of us have some form of debt. That’s why learning to effectively deal with debt is a core personal finance concept.